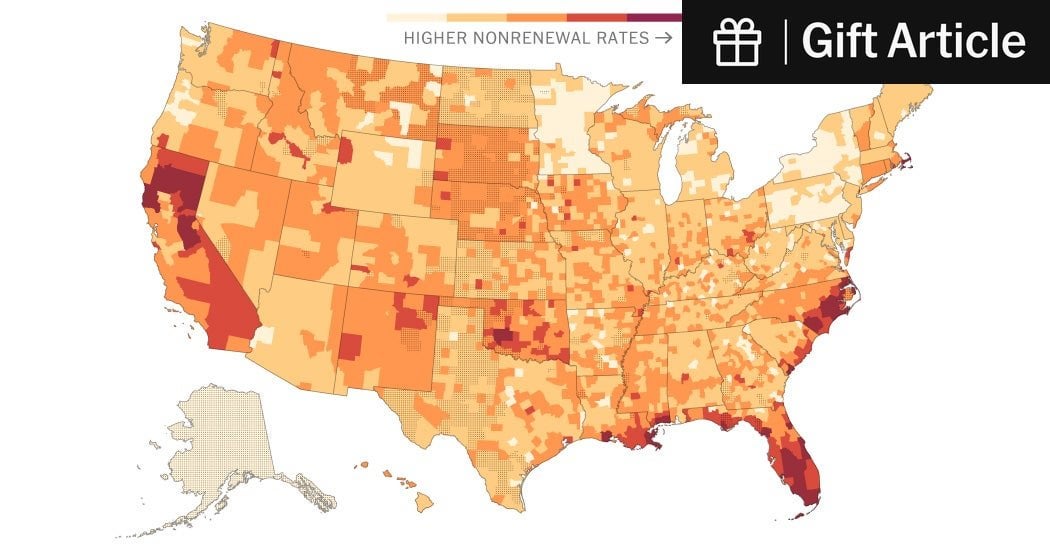

Florida insurance rates are insane. This is going to drive property values way down. No insurance means no mortgage. No mortgage means no house.

Why does Minnesota tend to be so good at things like this? I would normally just guess they are super white, but their neighbors are whiter.

I am a believer that culture does matter, but what would be unique about them vs say Wisconsin or South Dakota?

And wouldn’t the heavy snow or hail pose the same or more risks?

I can spot the hurricane and wildfire problem areas; what’s happening in OK that’s causing so many more non-renewals there than in adjacent areas?

I remain stumped as to why real estate prices have not adjusted in these areas along with lending — it seems inevitable that mass re-valuation is going to happen, with catastrophic economic consequences.

An under-appreciated aspect of non-renewal is that being unable to get homeowner’s insurance can also mean being unable to get liability or umbrella coverage. So, even if don’t need a mortgage and you’re willing to self-insure against the primary risk you may still be unable to stay due to liability exposure. I think California at least offers policies that wrap-around the FAIR or state fire insurance, but I don’t believe this is the case in NM which is a focus of the article.

Fire risk may be more addressable for owners than hurricane/flood in that there are more viable mitigation strategies available, but a LOT has to change and it’s happening slowly. Property values in these areas almost certainly have to come down significantly, which nobody is going to volunteer to do (and will have major impacts all by itself). Coverage probably has to become focused on ‘compensation to relocate’ in the event of a loss rather than ‘replacement’. Community response capability (water storage, sprinklers) probably has to increase and property maintenance and creation of firebreaks and defense lines has to become mandatory rather than advisory. All of this takes time and money and effort.

The problem is twofold. Increased regularity/severity of storms and extreme inflation on building supplies the last few years with no reductions predicted, on either side.

Property insurance companies across the nation have not been profitable in years and this is pretty well publicly documented.

Seems to be me houses should built stronger. And why is insurance for homes along the coast even available? That’s crazy to me, there is obvious inherent risk.

Just in time for a cabinet full of billionaires to sink any headway made in getting investment firms out of the residential housing market. Then, like magic, insurable again. Mark my words.

8 comments

Florida insurance rates are insane. This is going to drive property values way down. No insurance means no mortgage. No mortgage means no house.

Why does Minnesota tend to be so good at things like this? I would normally just guess they are super white, but their neighbors are whiter.

I am a believer that culture does matter, but what would be unique about them vs say Wisconsin or South Dakota?

And wouldn’t the heavy snow or hail pose the same or more risks?

I can spot the hurricane and wildfire problem areas; what’s happening in OK that’s causing so many more non-renewals there than in adjacent areas?

I remain stumped as to why real estate prices have not adjusted in these areas along with lending — it seems inevitable that mass re-valuation is going to happen, with catastrophic economic consequences.

* [McNamara et al 2024, Policy and market forces delay real estate price declines on the US coast]( https://www.nature.com/articles/s41467-024-46548-6)

* [Gourevitch et al 2023, Unpriced climate risk and the potential consequences of overvaluation in US housing markets](https://www.nature.com/articles/s41558-023-01594-8)

An [Atlantic article](https://www.theatlantic.com/science/archive/2024/08/climate-change-risk-homeowners-housing-bubble/679559/) with an overview.

What’s going on in northern California?

An under-appreciated aspect of non-renewal is that being unable to get homeowner’s insurance can also mean being unable to get liability or umbrella coverage. So, even if don’t need a mortgage and you’re willing to self-insure against the primary risk you may still be unable to stay due to liability exposure. I think California at least offers policies that wrap-around the FAIR or state fire insurance, but I don’t believe this is the case in NM which is a focus of the article.

Fire risk may be more addressable for owners than hurricane/flood in that there are more viable mitigation strategies available, but a LOT has to change and it’s happening slowly. Property values in these areas almost certainly have to come down significantly, which nobody is going to volunteer to do (and will have major impacts all by itself). Coverage probably has to become focused on ‘compensation to relocate’ in the event of a loss rather than ‘replacement’. Community response capability (water storage, sprinklers) probably has to increase and property maintenance and creation of firebreaks and defense lines has to become mandatory rather than advisory. All of this takes time and money and effort.

The problem is twofold. Increased regularity/severity of storms and extreme inflation on building supplies the last few years with no reductions predicted, on either side.

Property insurance companies across the nation have not been profitable in years and this is pretty well publicly documented.

Seems to be me houses should built stronger. And why is insurance for homes along the coast even available? That’s crazy to me, there is obvious inherent risk.

Just in time for a cabinet full of billionaires to sink any headway made in getting investment firms out of the residential housing market. Then, like magic, insurable again. Mark my words.

Comments are closed.