CHARLOTTE, North Carolina (ICIS)–There is

uncertainty about the extent that stated US

policy goals on tariffs will be achieved and

their impact on the economy this year and

beyond. Yet for now, the US economy remains on

solid ground.

An extension of the 2017 tax cuts would be

positive, as would deregulation and higher

defense spending. On the other hand,

immigration restrictions and tariff increases

would take away from growth and could foster

inflationary pressures. It is possible that new

tariffs will be measured.

Higher inflationary pressures of late have

raised interest rates, which could subtract

from US growth.

It is clear from looking at year-earlier

comparisons that the US economy is slowing. The

US remains in the late stage of the business

cycle, but there is likely more room for the

economy to run.

December featured a solid employment report.

There are 1.1 job openings per unemployed

person, a level back to pre-pandemic levels.

With a balanced labor market, incomes are

holding up for consumers and providing support

for the US economy.

The headline December Consumer Price Index

(CPI) was up 2.9% year on year, a

third month of higher comparisons. Economists

expect inflation to average 2.5% this year,

down from 2.9% in 2024, 4.1% in 2023 and 8.0%

in 2022. This is still above the Fed’s target.

CPI inflation is expected to stabilize at 2.5%

in 2026 and soften to 2.3% in 2027. That said,

expectations of stronger growth and higher

inflation have pushed up interest rates, as

measured by the 10-year Treasury yield.

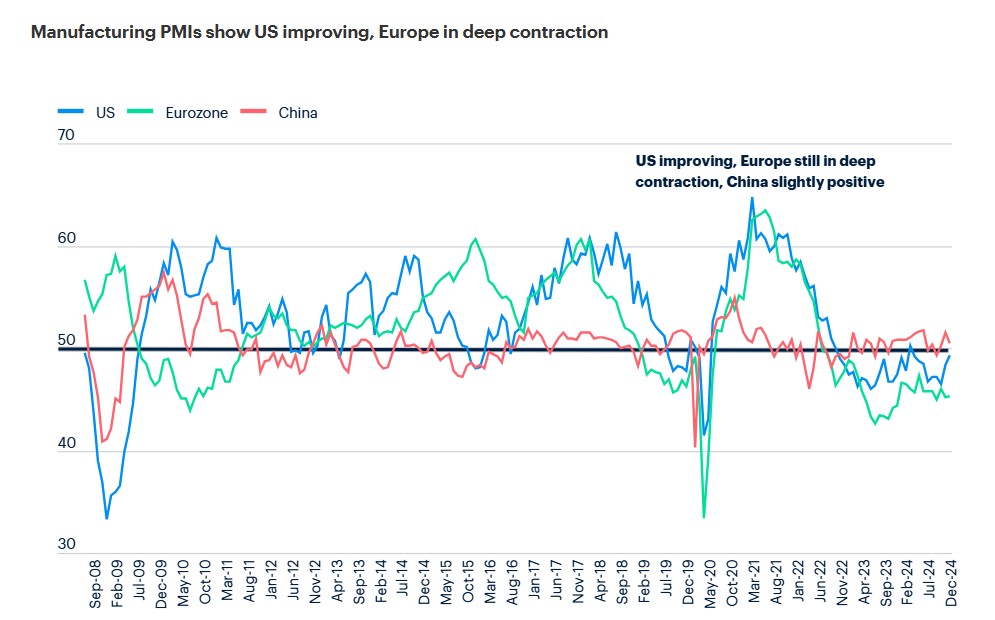

US MANUFACTURING PMI

IMPROVES

Turning to the

production side of the economy, the December

ISM US Manufacturing PMI registered 49.3, an

improvement from November’s reading.

Overall manufacturing production contraction

moved into positive territory, and new orders

strengthened further. Order backlogs and

inventories moved closer to breakeven,

suggesting the start of a restocking cycle.

Seven of the 18 industries surveyed expanded.

The ISM US Services PMI rose 2.0 points to

54.1, a good expansionary reading.

The Manufacturing PMI for Canada was in

positive territory for a fourth month while

that for Mexico contracted again slightly.

Brazil’s manufacturing PMI expanded for a

twelfth month, but at a slower pace.

Euro area manufacturing has been in contraction

for 30 months. The UK PMI remains in

contraction. China’s manufacturing PMI was

slightly positive for a third month, indicative

of a stalling recovery.

AUTO AND HOUSING

OUTLOOK

Turning to the demand

side of the economy, light vehicle sales

improved again in December, and although

inventories have moved up this past year, they

remain low. Affordability continues to be the

issue and is providing headwinds, although the

year ended on a solid note.

We expect light vehicle sales of 16.31 million

in 2025, before improving to 16.53 million in

2026 and 16.95 million in 2027. This would

bring activity back to the last peak in 2018.

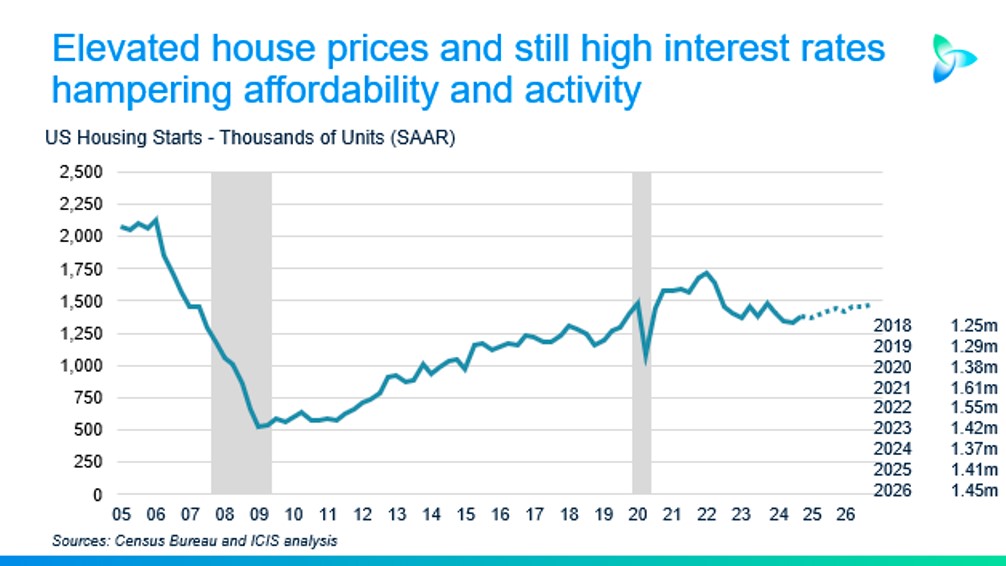

Housing activity continues to be muted amid

affordability issues as 30-year mortgage rates

returned to over 7%, along with low builder

confidence.

We expect housing starts will average 1.41

million in 2025 and improve to 1.45 million in

2026 and to 1.59 million in 2027. Demographic

factors will support activity through the end

of the decade. There is significant pent-up

demand for housing and a shortage of inventory.

RETAIL SALES PICK

UP

Retail sales were lackluster

for much of this year, but Q4 results were

robust. Sales at food services and drinking

places also remained positive. Overall consumer

spending continues to improve but may be

slowing.

Business fixed investment has been languid of

late, but led by a need to boost productivity

and by reshoring initiatives, this will take

over from consumer spending as a driver of the

US economy. This is typical in the late-stage

of the business cycle.

US GDP FORECAST

US GDP

rebounded 6.1% in 2021 and then slowed to a

2.5% gain in 2022. The much-anticipated

recession failed to emerge for a variety of

reasons, and in 2023, the economy expanded 2.9%

followed by an estimated 2.7% in 2024. This

pace is well above long-term growth potential.

Q4 2024 economic growth will be strong, but a

slowdown in quarterly economic gains towards

long-term growth potential suggests that in

2025 the economy could rise 2.2%, followed by

another 2.2% gain in 2026 and 2.0% growth in

2027.

Deregulation, energy and tax reform as well as

other initiatives could aid economic growth.

The US continues to outpace other advanced

nations. Recent results suggest that Europe’s

economic prospects appear stagnant amid many

structural and competitiveness headwinds.

China appears to be attempting to export its

way out of a soft economy. The stimulus

provided will likely have only a modest effect

on improving growth prospects and rising trade

tensions may hinder growth.