Global oil prices faced significant headwinds in the first quarter that could continue as 2025 unfolds. We were surprised that the Organization of the Petroleum Exporting Countries and allies (OPEC+) adhered to its timeline of gradual production increases on April 1. American trade policy uncertainties have rippled through the market, including possible inflationary impacts that could weaken demand, and a Russia-Ukraine peace deal could further weigh on crude prices. Still, new sanctions on Venezuela and the willingness by OPEC+ to reevaluate its decisions means we’re likely approaching a floor on crude, as some market indicators hint at upward pressure.

Source: Morningstar. Data as of March 24, 2025.

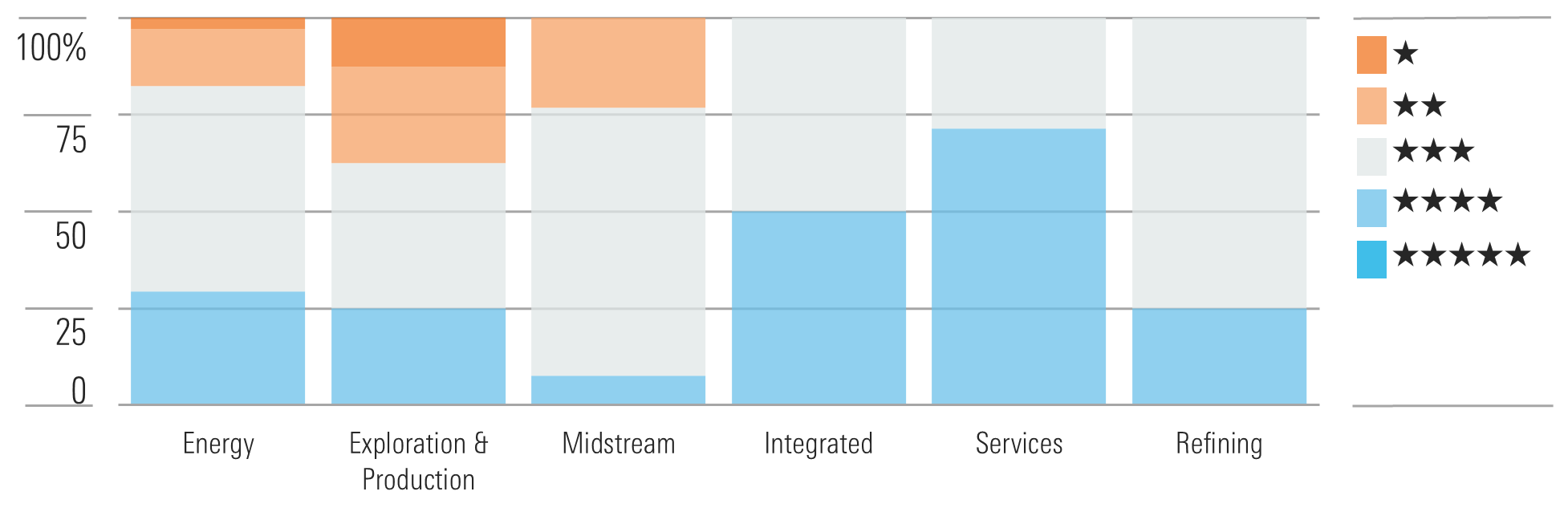

Source: Morningstar. Data as of March 24, 2025.

Uncertainty surrounding global oil supply and demand has weighed on stock performance for oil producers. Oil names like Devon and Hess look undervalued, as the market has poured and parked capital in gas-leveraged names. Idiosyncratic trends in gas demand, driven by artificial intelligence, data centers, and new LNG production coming online, supports elevated North American natural gas prices to the end of 2025. Though many gas E&P names have these trends largely priced in, we still see value in names along the gas value chain in services such as SLB and Halliburton.

Source: Rystad, Morningstar, Data as of March 7, 2025.

US rig count has held roughly flat sequentially, suggesting the market is stuck in a wait-and-see holding pattern amid broader macroeconomic uncertainty. It initially appeared that OPEC+ production cuts would keep crude oil near year-end pricing levels through the first quarter of 2025. That proved somewhat true through most of the first quarter, but oil prices have slid further in March. On the gas side, we expect Henry Hub prices above $4 per MMBtu means US producers will likely tap into their inventories of drilled wells.

Source: Rystad, Morningstar, Data as of March 7, 2025. Top Energy Sector PicksHF Sinclair

HF Sinclair DINO is the lone refiner trading below our fair value estimate. After HollyFrontier’s acquisition of Sinclair Oil, HF Sinclair is a fully integrated independent company composed of refining, marketing, renewables, specialty lubricants, and midstream businesses. Following weak fourth-quarter results, the company remains a turnaround story, but management is showing progress in improving reliability and efficiency and cutting costs across its portfolio to improve competitiveness. Along with a focus on shareholder returns, we think this is the right playbook to improve valuations.

Schlumberger

Schlumberger SLB is among the cheapest stocks in our global energy coverage with a moat. Its multiple trades in line with peer services firms, but it deserves a premium given its scale, suite of solutions, competitive position in some of the more attractive services markets, and technological advantage. These factors position SLB to outperform peers. Its offshore segment outside North America boasts a growing project opportunity set that could exceed $100 billion annually over the medium term. SLB’s digital-related revenue is also highly accretive and more resilient to cyclical headwinds. We expect digital revenue can more than double by the end of the decade.

ExxonMobil

ExxonMobil’s XOM strategy diverges from industry trends as it plans to increase its spending through 2030, aiming to raise production to 5.4 mboe/d and boost earnings by over $20 billion. While this higher spending has raised concerns among investors, given the industry’s track record of prioritizing growth over returns, Exxon’s high-quality hydrocarbon portfolio should ensure attractive returns while maintaining capital discipline. Continued capital efficiency gains and structural cost reductions support the company’s ambition of generating $165 billion in surplus cash by 2030, with $20 billion in share repurchases projected for 2025 and 2026.