following Israeli strikes on Iran but impact on

fundamentals limited

Retaliation from Iran highly likely, strong

response expected given Israeli attack severity

But energy market participants cautious on

longer-term escalation risks, citing regional

examples of geopolitical tension with limited

lasting price impact

Brent crude would need to near $100/bbl for

oil-linked LNG contracts to match current LNG

spot market prices

Unfolding situation further supports

already bullish picture for coming months

across energy markets

In the early hours of 13 June, Israel

launched a wave of attacks targeting Iran’s

nuclear programme, with strikes on nuclear

infrastructure as well as the killing of

scientists and military figures. Iran’s foreign

minister called the attacks a “declaration of

war” and vowed to retaliate.

ICIS experts share views on the potential

next steps and the future impact across the

energy complex.

Did the strike

take energy markets by surprise?

(Matthew Jones, Head of Power

Analytics) An Israeli strike on Iran’s

nuclear capabilities has been a significant

market risk for many months. Back in January,

we predicted this occurrence

in 2025. While there had not been much sign

of an impending attack in the first few months

of the year, there were reports in late May

that Israel was preparing a move, while the US

began to pull staff out of the Middle East on

Tuesday 10 June, after news emerged that

strikes could be

imminent. The exact timing was not clear,

but markets were aware of rapidly increasing

risk.

What price impact have we seen so far

across the commodity complex?

(Gemma Blundell-Doyle, Crude Market

Reporter) Oil prices spiked by almost 10%

on Friday morning, to their highest since

January this year. Brent crude reached

$78.48/barrel at 03:41 London time. At 14:30 it

remained elevated at $74.33/barrel.

(Rob Dalton, Senior Gas Market

Reporter) European gas prices rose on

Friday morning with the ICIS TTF front-month up

6% to €38.50 ($44.30)/MWh, a three-month high.

(Anna Coulson, Senior Power Market

Reporter) Bullish European gas supported

power prices, with the German front month

rising 2.2% from Thursday’s close to €82.75/MWh

by 13:50 on Friday.

(Ed Cox, Global LNG Editor) East Asian

LNG (ICIS EAX) spot prices rose 8% on Friday to

$13.43/MMBtu, the highest since March. Asian

spot prices have been increasing since early

June, in line with a firmer ICIS TTF.

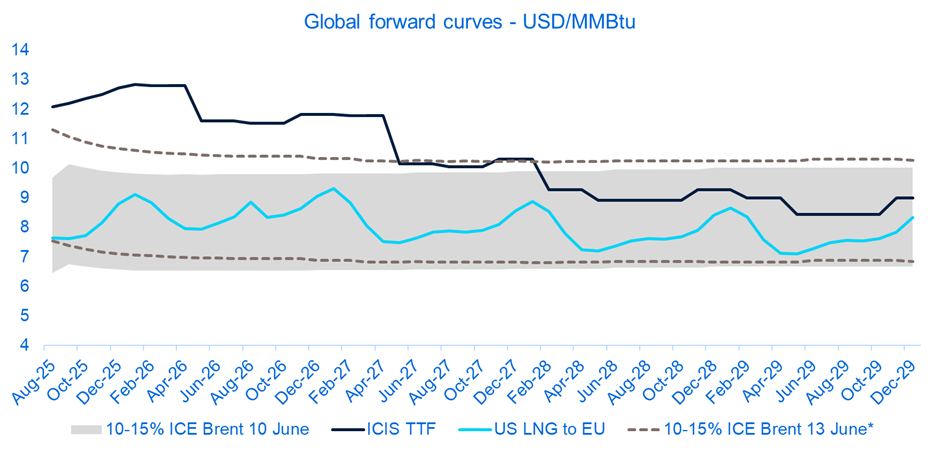

forward curves 13 June 2025, Source: ICIS,

CME

Is the price impact risk-based, or have

we seen a direct impact on fundamentals so

far?

(Gemma Blundell-Doyle) Oil

fundamentals were on Friday afternoon

unchanged. The National Iranian Oil Refining

and Distribution Company said refining and

storage facilities had not been damaged and

continued to operate.

(Rob Dalton) The immediate,

price-driven response across the TTF was

fuelled by rising risk premiums and speculative

positioning, with particular concern

surrounding the shutdown of Israel’s offshore

gas fields. Market participants remain cautious

about the longer-term risks of escalation, with

many pointing to the 2024 Israel-Iran conflict

as an example of geopolitical tension with

limited lasting impact on pricing.

(Ed Cox) No immediate fundamental LNG

impact with outright spot LNG demand limited

from key Asian buyers, partly due to market

prices sitting well above oil-linked LNG

contracts.

LNG buyers closely monitor oil prices, which

are still used to price most Asian LNG

procurement. Most oil-linked contracts take a

historic oil price of at least three months

previous, so higher Brent today would impact

LNG contracts later in the year. Brent would

need to go closer to $100/bbl for oil-linked

LNG contracts to match current LNG spot prices

and to encourage buyers to switch to more spot

offtake.

ICIS understands that Egyptian fertilizer

producers have already shut down at least three

urea plants because of measures taken by Israel

to temporarily halt gas production. Israel

supplies over 30 million cubic metres/day of

gas to Egypt, which already faces major supply

shortages. Any extended reduction in Israeli

gas supply could mean Egypt has to buy

additional LNG cargoes to cover the shortage.

Egypt has recently committed to buy what could

be close to 10 million tonnes of LNG in 2025

and 2026 from a variety of sellers through

large tenders. It may call on the market for

additional cargoes which in turn could further

support global spot prices.

What next?

(Matthew Jones) You could see

different levels of response from Iran. The

least consequential would be similar to the

events of April 2024 playing out again, in

which Iran fires missiles and drones at Israel,

which shoots most of them down. Given Iran’s

weak position this cannot be ruled out.

But it seems more likely that Iran will attempt

a stronger response given the severity of the

Israeli attack. That could include attacks on

targets in the Persian Gulf, including on

tankers or oil refineries.

Iran could conclude that creating energy market

turbulence is the best way to get the US to

restrain Israeli action.

The most consequential response would be the

closing of the Straits of Hormuz through which

massive volumes of global oil and LNG travel.

Such an event would have major bullish

consequences for global energy markets but

should be seen as low probability as Iran will

be very reluctant to alienate key allies like

China. It would also be physically very

difficult for Iran to close the Strait even if

it wanted to.

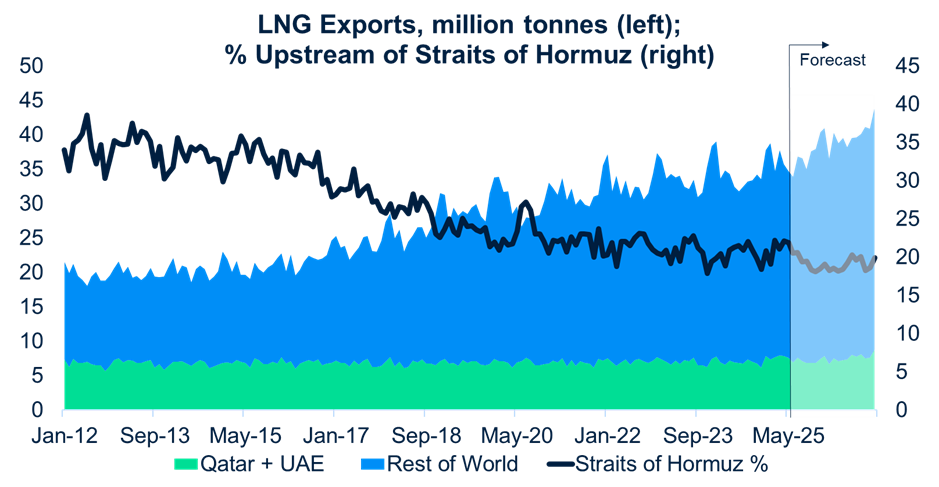

(Ed Cox) For LNG, the narrative around

a potential Straits of Hormuz closure will

return, even if this would represent a major

further escalation from Iran with little

clarity on practical implementation.

Almost 20% of global LNG production will pass

through Hormuz from Qatar and the UAE in 2025

so the global LNG market will naturally focus

closely on events. LNG and wider shipping flows

via the nearby Suez Canal remain constrained

due to the risk of attack and there is limited

scope for a major impact on LNG shipping given

the large number of new vessels coming to the

market which is suppressing charter rates.

But we should expect major LNG buyers to

analyse current stocks and review emergency

supply security plans in response to these

events.

Global LNG exports and share of

trade using the Strait of Hormuz. Source:

ICIS

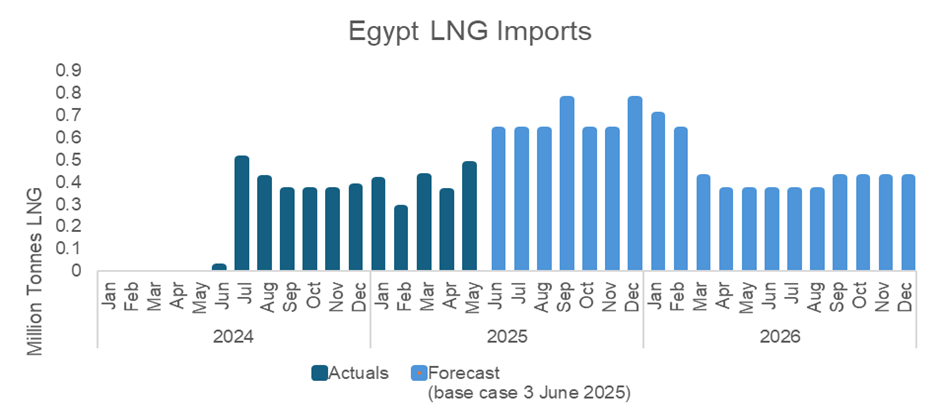

(Andreas Schroeder, Head of Gas

Analytics) A wider Middle East conflict

could have serious implications for Egyptian

gas markets. The country has switched to

becoming an importer of LNG since 2024 and is

set to increase imports going forward.

A major buy tender was issued recently. There

is now talk of around 100-110 cargos needed

overall in 2025 instead of the previously

expected 60-70. We forecast 6.3 million tonnes

of LNG imports, nearly tripling the 2.4 million

tonnes of 2024.

Egypt also receives LNG via pipeline from

Jordan’s Aqaba import terminal, which imported

0.8 million tonnes in 2024. In addition, Israel

is a major pipeline supplier to Egypt with

around 10 bcm/year covering a fifth of Egyptian

demand. Should a regional conflict escalate

further, an extended stop of Israeli gas

exports to Egypt could imply even stronger LNG

intake into Egypt for the remainder of 2025.

Egyptian LNG imports. Source:

ICIS

(Gemma) The US and Iran are set to

meet in Oman on 15 June to continue ongoing

nuclear talks. The Israeli strike on Iran will

be on the agenda. US president Trump has urged

Iran to make a deal regarding its nuclear

programme and to prevent further attacks from

Israel, bit it is unlikely Iran will concede

without retaliation.

Where could commodity prices go in

coming days and weeks?

(Ajay Parmar, Director, Energy &

Refining) We expect Iran to retaliate and

tensions to escalate further. This will likely

cause oil prices to remain elevated for the

coming weeks. If a resolution is found later

this month, prices could begin to retreat, but

for now, we see them remaining elevated in June

and July as a result of this escalation.

(Ed Cox) The TTF is ever more

influenced by geopolitical events given

Europe’s dependency on LNG imports. Often, TTF

volatility does not match changes in regional

gas fundamentals as traders are changing

positions to consider wider macro views. It is

possible the TTF could swing by 5-10% daily

while uncertainty over further escalation

continues.

Even though oil pricing plays a limited role in

European gas price formulation, it is likely

the TTF would follow higher Brent in the

context of an overall bullish energy market.

(Rob Dalton) Even before recent

developments, the near-term outlook for

European gas markets had already tilted bullish

due to a summer injection demand gap. An

escalating conflict would heighten the risk of

a broader move higher across the entire near

curve, placing increased emphasis on refilling

storage sites in the near term.

How does the news impact your broader

view of the current energy market

complex?

(Matthew Jones) We held a webinar on

12 June in which we presented a bullish view

for the European energy commodity complex in H2

2025. We see significant upside risk to prices

in the coming months, stemming from

expectations for rising carbon prices, gas

storage targets shifting volume risk to winter,

the potential continuation of low wind speeds

and fears over the return of stress corrosion

issues at French reactors.

The Israeli attack on Iran and the potential

consequences we have outlined here further

support that bullish picture for the coming

months.

(Ed Cox) From an LNG perspective, the

fundamental outlook from Asia is not strong in

the short term, largely due to weak economic

performance from China. European gas looks more

bullish. But the correlation between the TTF

and Asian spot LNG is strong with the potential

for prices in both markets to rise further on

Middle East concerns, even if the immediate

fundamental impact is focused on Israeli gas

supply to Egypt.