in line with normal range

Growing focus on Iran’s Hormuz Strait

closure rhetoric

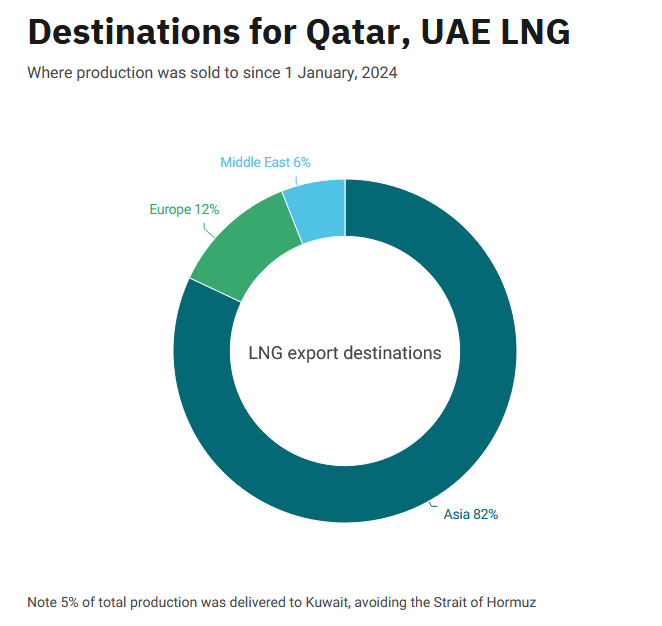

Over 80% of Qatari LNG goes to Asia but

highly relevant for Europe

LONDON (ICIS)–LNG production from Qatar and

the UAE – the two countries that sit the other

side of the Strait of Hormuz from global buyers

– continues as normal, according to ICIS data.

Disruption to shipping signals is making the

accurate tracking of LNG vessels harder, and

more ballast Qatari vessels are waiting east of

Hormuz than normal before going to Ras Laffan

to load.

ICIS data on Monday 23 June showed that 43

vessels had loaded from Ras Laffan in the last

15 days, unchanged from the same period last

year.

This is down by one from the previous 15-day

period, but this is not an unusual deviation

given the scale of 77.4mtpa production.

A total of four cargoes loaded from the UAE’s

Das Island over the past 15 days, up by one

from last year, down by one from the previous

15 days, according to ICIS data.

ICIS analysts have observed a number of vessels

near Qatar registering false positions via

their AIS signal data.

But ICIS identified the laden 138,000cbm

Disha

as having crossed Hormuz east on Sunday 22

June, as well as the 152,000cbm Al

Areesh and the 174,000cbm Al

Sakhamah.

The 138,000cbm Raahi

appears to have crossed west in ballast on 23

June.

KEY LNG TRADE FLOWS

spot prices have moved up since early June due

to growing security concerns in the Middle

East, and are back to the highest levels since

February.

While the TTF now reacts immediately to major

geo-political news given the depth of market

participants, liquidity, and Europe’s

dependency on LNG imports, East Asian spot LNG

pricing remains less liquid, and highly

influenced by the European market.

That said, the ICIS East Asia Index remains at

a volatile premium to the TTF, despite limited

new LNG demand signals from Asian buyers.

Since the start of 2024, 82% of Qatari LNG has

gone to Asian markets, according to ICIS data,

with Europe now accounting for a much smaller

share.

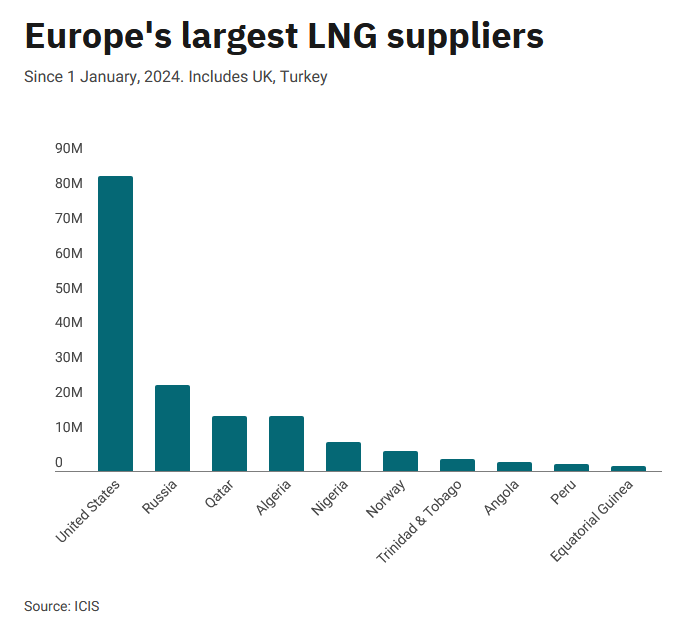

Rising US LNG production has stepped in to

dominate Europe’s LNG supply.

The UK, for example, now imports much more from

the US than it does from Qatar.

Major LNG buyers continue to analyse potential

risks to current supply from the Middle East

situation, and are well aware of the impact

even a small reduction in Qatari deliveries

would have.

While this would hit Asian buyers most

directly, it would also impact European markets

if higher Asian spot prices pulled US LNG away

from Europe.

BULLISH PRICES

An Asian price premium of up to $0.50/MMBtu to

the TTF – typical of the last month – would

likely mean sufficient US LNG flows to both

Europe and Asia to cover demand and reflects a

reasonably well-balanced market.

In the event of a cut in supply to Asia, the

EAX would rise, taking the TTF with it given

Europe’s dependency on LNG.

The Asian premium to TTF would likely need to

rise to at least $2/MMBtu to pull much larger

volumes of US LNG away from Europe.

Further TTF price rises would filter through

across European energy markets.

In Asia, most LNG is still sold on an oil price

link which is currently well below spot prices

– although oil prices would naturally also be

impacted by Hormuz disruption.

It is unlikely, however, that outright gas and

LNG prices would substantially deviate between

the two regions as both would compete for

cargoes.

Higher spot LNG prices would also dent demand

from many Asian buyers.

Any extended closure of Hormuz appears highly

unlikely given likely pressure that would come

from major economic and military powers against

Iran.

But even short-term disruption could lift LNG

and gas prices and lead to significant

scrambling from sellers and buyers needing to

use all available optimization and risk

management tools at their disposal.

Alex Froley contributed to this story