Undoubtedly, such stocks are hard to find, and even if you do, you need the patience to sit tight. What often drives such rallies are industry tailwinds, government focus, management changes, or business restructuring. But what’s really behind their rise? And after such a steep rally, is there still steam left?

Let’s take a look.

It all starts with PG Electroplast Ltd

PG Electroplast has delivered a return of 20,000%, rising from ₹4 on 17 July 2020 to ₹802 today.

The company has transformed into a dominant player in the electronic manufacturing services (EMS) space—a sector benefiting from a strong structural industry tailwind. Back then, it primarily manufactured plastic mouldings for sectors like consumer durables.

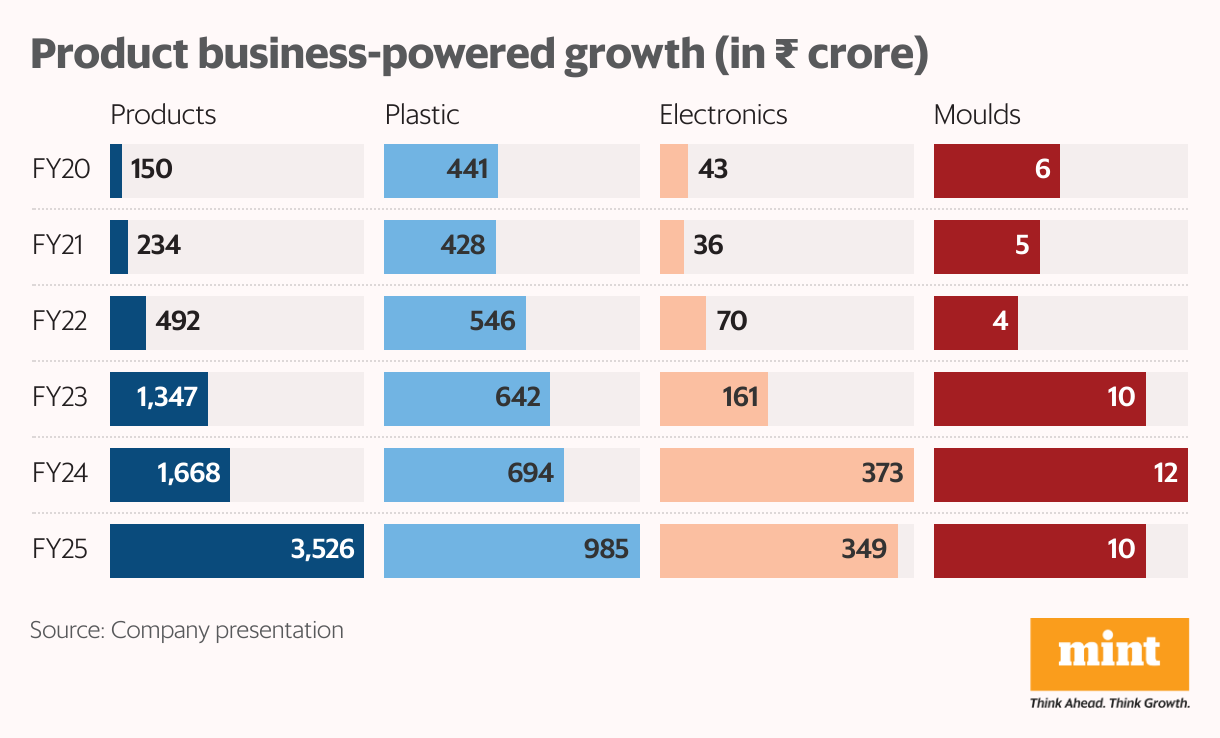

In 2019-20, this segment contributed the most to its revenue, accounting for 69% ( ₹441 crore) of its total revenue of ₹640 crore. The rest (24%) came from product segments (room ACs, washing machines, and air coolers). Its other segments include electronics (televisions and printed circuit boards) and appliance manufacturing.

However, the China+1 manufacturing theme and the government’s push for ‘Make in India’ through production-linked incentives (PLIs) brought a transformational shift not just for PG Electroplast, but for the entire EMS sector.

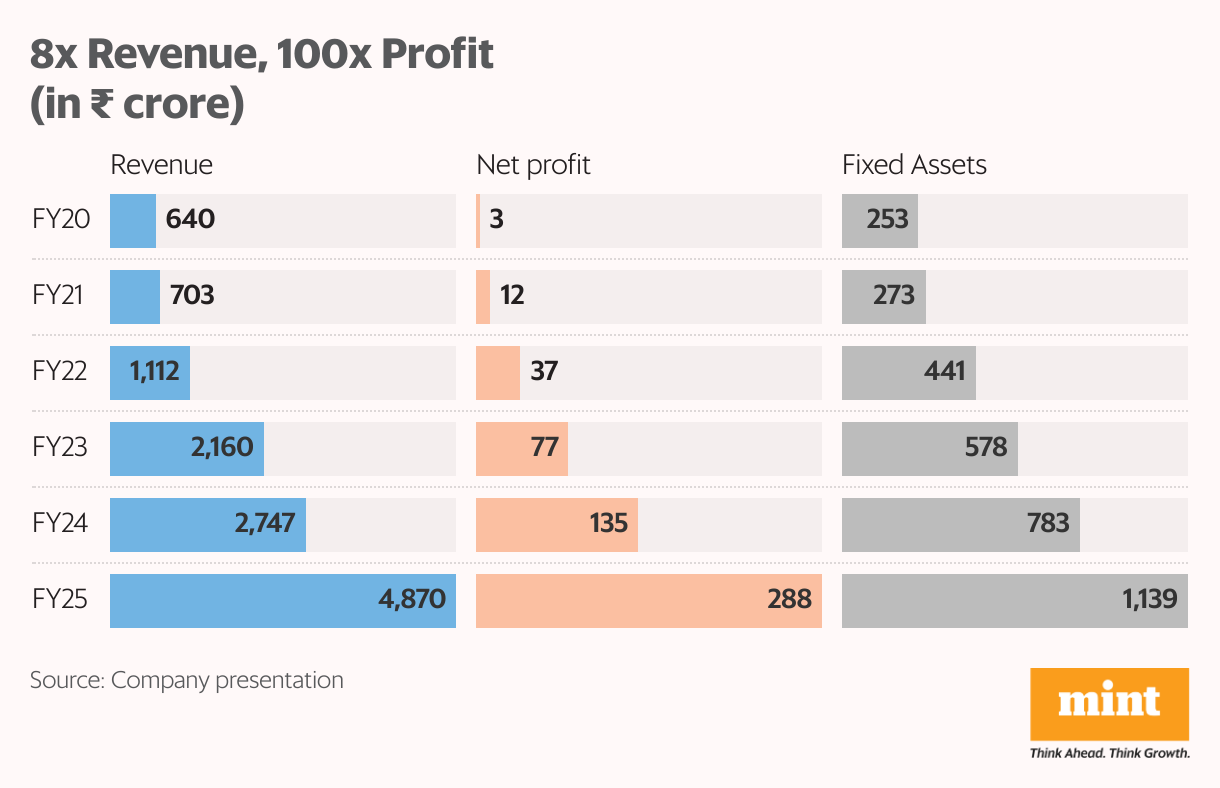

This shift is evident in the product segment’s revenue, which rose 15-fold to ₹3,526 crore in 2024-25, from just ₹150 crore in 2019-20. The segment now contributes 71% to its total revenue, which also grew about 8X to ₹4,870 crore.

At the same time, the plastic moulding division’s contribution fell to 20%, from 69%. The company’s net profit surged 100X to ₹288 crore, from just ₹2.6 crore in 2019-20. Such a steep jump in profitability is typically what drives multibagger returns.

Return ratios have also seen a sharp rerating. Return on equity (RoE) expanded to 15% (19% in 2023-24) from 13.4%. Return on capital employed (RoCE) has almost doubled to 27%—showing efficient utilization of capacity.

None of this would have been possible without expanding manufacturing capacity. The company’s fixed assets have grown 4X to ₹1,139 crore, from ₹253 crore in 2019-20.

Looking ahead, PG is well-positioned to benefit from a structural long-term tailwind in the EMS space. Rapid urbanization, government reforms, low penetration of consumer durables, and the China+1 theme are all expected to sustain growth momentum.

The company expects revenue to rise 30% to ₹6,345 crore in 2025-26, with 75% coming from the product business. Net profit is also expected to rise 39% to ₹405 crore. To support this growth, PG is also expanding its manufacturing footprint.

It is setting up a washing machine facility at Greater Noida in Uttar Pradesh, a refrigerator plant in the South, and an AC capacity in Maharashtra’s Supa. However, valuations leave little room for error.

It trades at a price-to-earnings (P/E) multiple of 80, well above its five-year median of 55. But it still trades at a discount to its closest peer, Dixon Technologies (India) Ltd, which trades at 123X earnings.

Transformers and Rectifiers joins the 100-bagger club

Transformers and Rectifiers (India) Ltd has delivered a return of 10,000%, rising from ₹5 on 15 July 2020 to ₹510 today. That means your investment of ₹1 lakh would be worth ₹1 crore today.

The company is a leading player in transformer and reactor manufacturing in India, with a global presence. Its diverse product range includes power transformers (up to 500 MVA), furnace transformers, rectifier and distribution transformers, as well as speciality transformers.

Its products are used across industries, including power distribution, petrochemicals, pharmaceuticals, power transmission, metal processing, cement, and railways. The company has also ventured into renewable-focused segments, including transformers for solar applications and green hydrogen.

Its customer base includes all the leading players, including NTPC, JSW, Tata Power, Siemens Energy, Torrent Power, Blue Star, and Hindustan Zinc.

The company has been a key beneficiary of rising infrastructure investment in India. The government capital expenditure, growing global power demand, and rapid expansion of data centres have all contributed to strong demand for power equipment, including transformers.

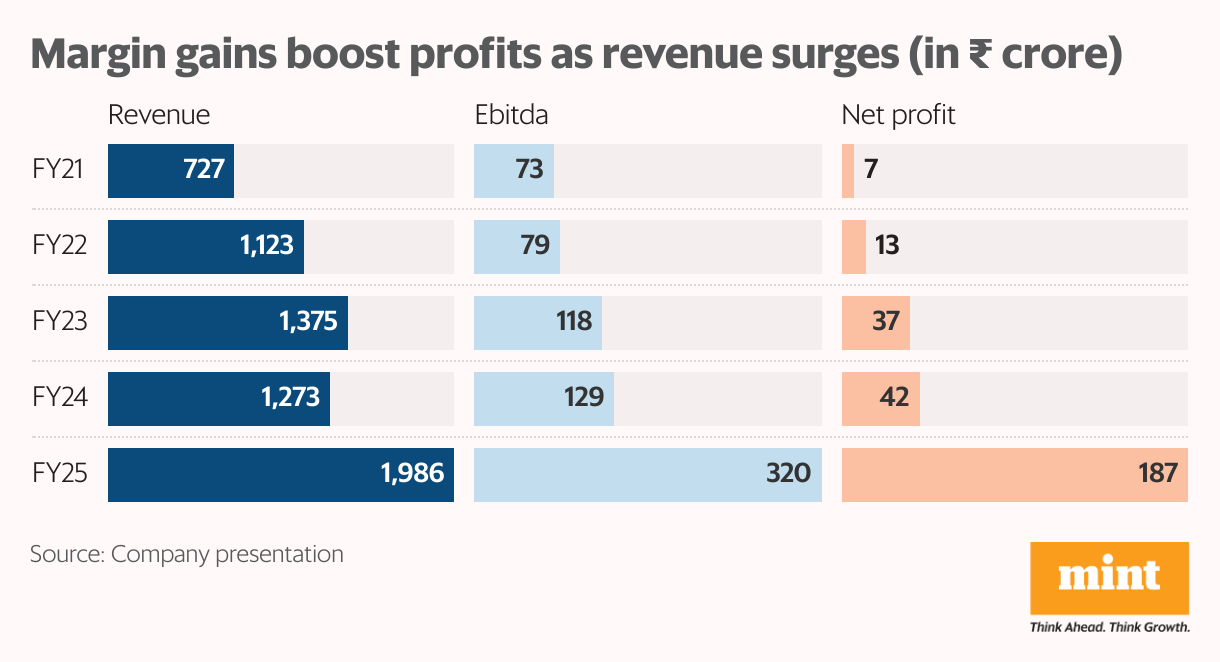

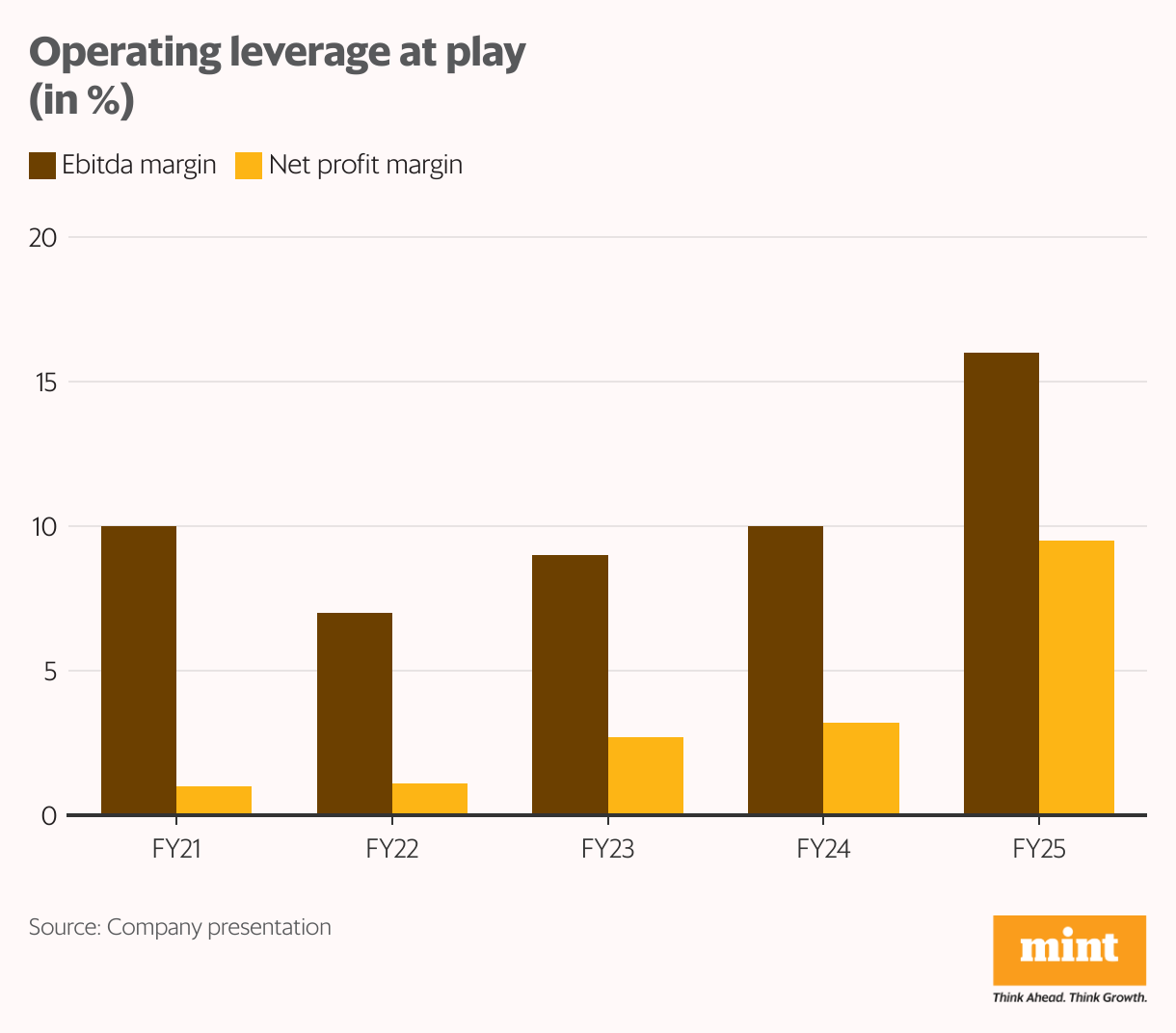

The numbers reflect this momentum. Revenue has grown at a compound annual growth rate (CAGR) of 28% during FY21-FY25, rising from ₹727 crore to ₹1,950 crore. Ebitda margin expanded from 10% to 16% as operating leverage kicked in, while net profit margin surged by 860 basis points to 9.5% in 2024-25. Ebitda stands for earnings before interest, taxes, depreciation, and amortization.

With improved margins, the company’s net profit rose nearly 27-fold, from ₹7 crore to ₹187 crore during the same period. RoCE also nearly doubled to 23%, from 12%. Yet, the growth story may still have more legs.

As of 31 March 2025, the order book stands at ₹5,132 crore, providing strong revenue potential. In addition, order inquiries worth over ₹22,000 crore are currently under negotiation.

The company has set an ambitious target to become a $1 billion ( ₹8,600 crore) revenue player by 2027-28. This implies a sharp CAGR of 64% between 2024-25 and 2027-28—a target that management remains confident of achieving through strong execution, innovation, and financial discipline.

Notably, it expects profit growth to outpace revenue expansion, supported by operating leverage and other efficiencies. The company aims to maintain a consistent margin of 16-17% going forward and improve it further through operational efficiencies.

Key strategic priorities include strengthening backwards integration, investing in automation and digital transformation, and focusing on clean, sustainable energy solutions in alignment with India’s power sector goals.

It has also acquired a controlling stake in a CRGO processing unit—a key input that accounts for 32%-35% of transformer manufacturing costs. This move ensures 100% backwards integration, offering a price, margin, and product quality advantage. This is expected to enhance competitiveness in order booking and profitability.

The company is also expanding its manufacturing capacity to meet rising demand. A 15,000 MVA capacity expansion kicked off in Q1FY25, with Phase 1 operations expected to begin by May 2025. This phase will contribute about half the incremental volume, with full capacity becoming commercially available by Q2FY26.

Additionally, it also expects a 22,000 MVA extra-high voltage transformer expansion to be completed by Q4FY26. These projects will increase its capacity from 40,000 MVA to 75,000 MVA. The company also plans to enter the fast-growing HVDC (High Voltage Direct Current) segment soon.

That said, after such a steep rally, it now trades at a P/E of 72, in line with its five-year median of 64.

What’s behind SG Finserv’s 180x run

SG Finserv became part of the APL Apollo Group following its acquisition in 2022. It was initially set up to meet the funding needs of dealers associated with APL Apollo Tubes, the group’s flagship company.

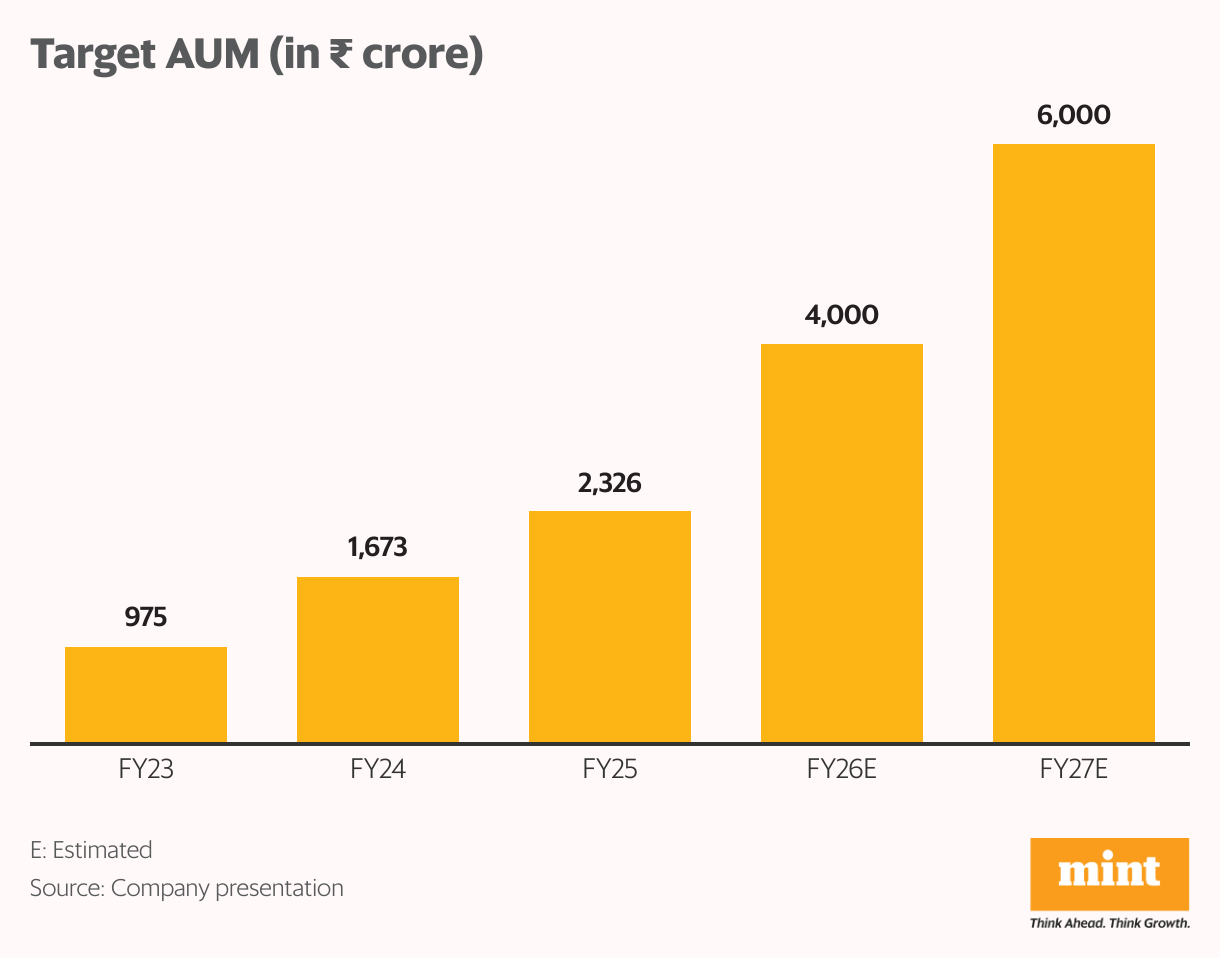

As of 31 December 2022, the company’s assets under management (AUM) stood at ₹736 crore, when it had just begun financing APL vendors. Over time, it expanded its scope to offer financing solutions to SMEs, MSMEs, and other corporate entities.

The AUM has since grown over threefold to ₹2,326 crore. The portfolio is geographically diversified, with the North contributing 44%, followed by the South (30%), the West (23%), and the East (3%).

Notably, it holds zero gross non-performing assets. Around 80% of the book is backed by a charge on funded inventory and receivables generated through sales, which maintains a light asset quality.

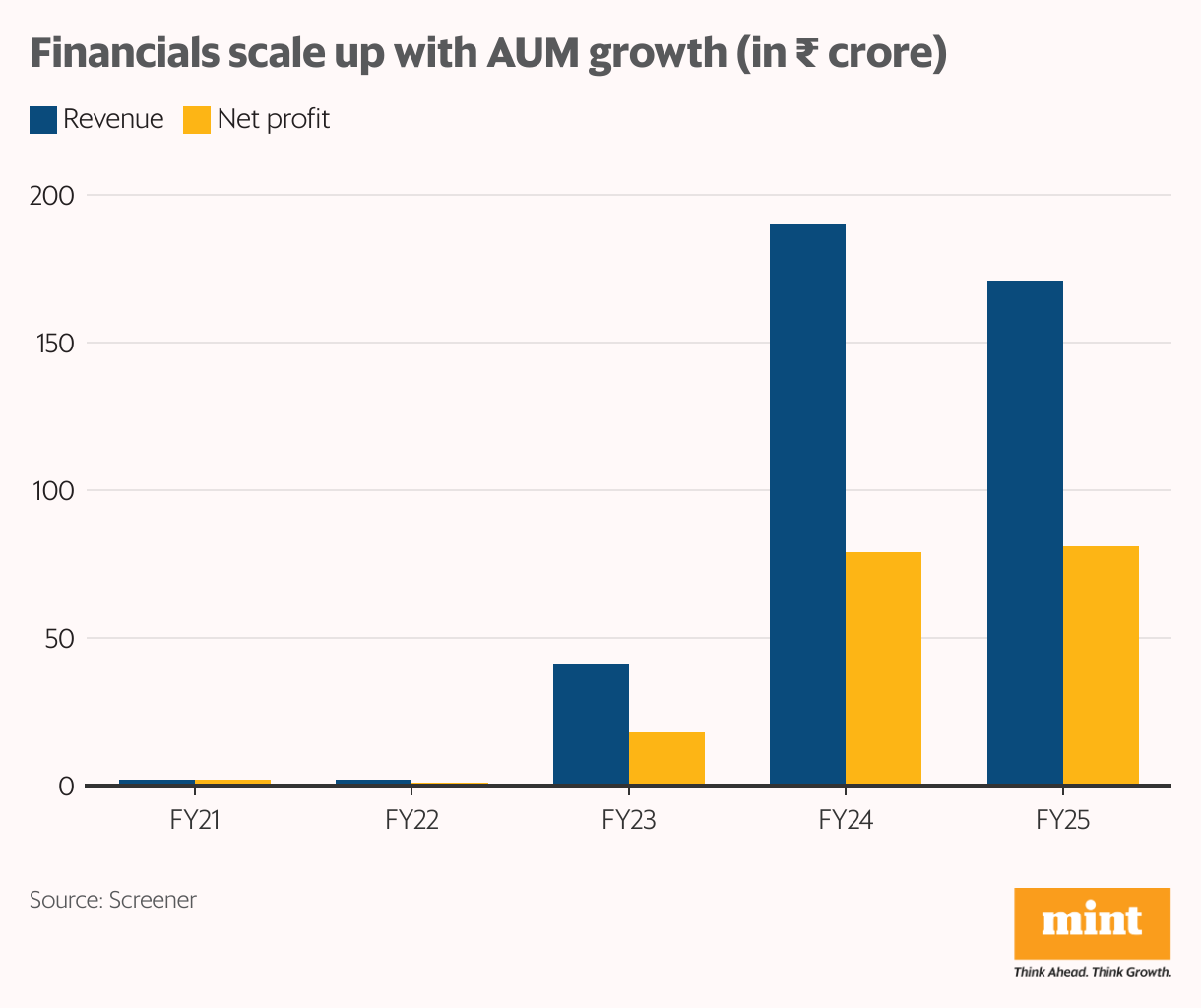

With AUM growing rapidly, revenue grew from ₹2 crore in FY22 to ₹171 crore in FY25. Net profit also rose from ₹1 crore to ₹81 crore in the same period. The company’s share price has surged 18,348%, from ₹2.2 on 22 July 2020 to ₹404 today.

But it’s a company poised for rapid growth, with plans to scale its AUM to ₹6,000 crore by 2026-27. To drive this expansion, it is partnering with large corporations, including the Tata group, Vedanta, Ashok Leyland, and Adani Group.

Backing this effort, memorandums of understanding worth ₹5,500 crore are already in place, laying the groundwork for the next leg of growth.

Madhusudan Kela holds a 1.7% stake in the company as of Q4FY25. The stock trades at a price-to-book ratio of 2.6, below its five-year median of 3X.

Conclusion

These three companies may have delivered extraordinary returns, but each benefited from a mix of industry tailwinds, business reinvention, and financial discipline. While past performance has been stellar, future gains will likely depend on execution, margin sustainability, and valuations that leave little room for error. For investors, the key lies in distinguishing between momentum and long-term fundamentals.

About the author: Madhvendra has over seven years of experience in equity markets and has cleared the NISM-Series-XV: Research Analyst Certification Examination. He specialises in writing detailed research articles on listed Indian companies, sectoral trends, and macroeconomic developments.

Disclosure: The writer does not hold the stocks discussed in this article.

The purpose of this article is only to share interesting charts, data points, and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educational purposes only.