![Backtesting YouTube Finfluencer Stock Picks vs. S&P 500 (Risky Inverse strategy beat the market) [OC]](https://www.europesays.com/wp-content/uploads/2025/07/vdjczxauqrdf1-1920x1024.png)

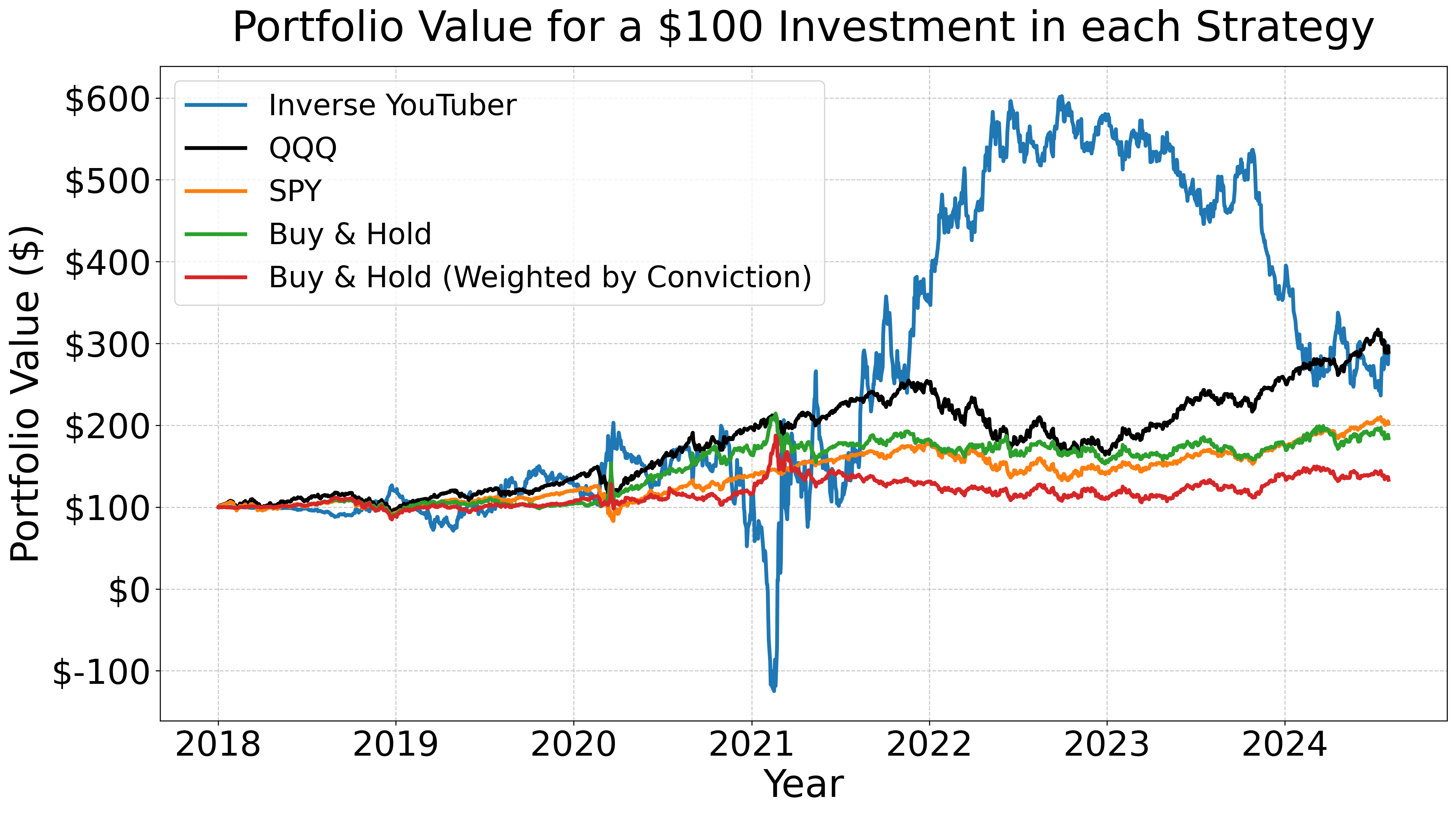

Portfolio value on a $100 investment: The Inverse YouTuber strategy outperforms QQQ and S&P 500, while all other strategies underperform.

Data Source: Hundreds of recommendation videos by YouTube financial influencers (2018–2024).

Tools Used: Matplotlib, manual annotation, backtesting scripts.

Original Source Article: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=5315526

Posted by mgalarny

8 comments

Forgot to add the code in my post sorry! [https://github.com/gtfintechlab/VideoConviction/blob/master/back_testing/graphics.ipynb](https://github.com/gtfintechlab/VideoConviction/blob/master/back_testing/graphics.ipynb)

Like when YouTubers say buy you don’t buy and when they say don’t buy you buy?

So the port does well in a bear market. Not so well otherwise.

From the abstract:

> While high-conviction recommendations perform better than low-conviction ones, they still underperform the popular S&P 500 index fund. An inverse strategy-betting against finfluencer recommendations-outperforms the S&P 500 by 6.8% in annual returns but carries greater risk (Sharpe ratio of 0.41 vs. 0.65).

How do you go from $100 to -$120 back to positive cash with normal investments??

[edit] Everyone is completely missing the point. Every other line here represents a “normal” investment strategy where you max losses are $100. OP just casually mixed in a much riskier strategy. The comparison is nonsense.

I love it: *pmud dna pmup* strategy

Could you try doing the same thing for crypto?

For selling, are you accounting for borrowing costs to short the stock? I skimmed the paper but didn’t see mention of it.

What was the ratio of buy to sell recommendations? Am I correct to assume that there are way more buy recommendations than sell?

I know this paper is mostly about your VideoConviction model, but to nitpick: The Inverse YouTuber strategy would need to pay a lot of borrowing fees, right? Is this accounted for?

Comments are closed.