Cyprus has recently enacted significant amendments to its tax legislation, introducing robust defensive tax measures aimed at countering aggressive tax planning involving low-tax jurisdictions (LTJs) and non-cooperative jurisdictions (NCJs), often referred to as “blacklisted” jurisdictions (BLJs). Businesses with structures involving Cyprus and entities in such jurisdictions, such as holding, financing and IP structures, must urgently review their arrangements to mitigate substantial tax exposures and administrative penalties.

The new tax legislation includes key amendments to the Income Tax Law (ITL), the Special Defence Contribution Law (SDCL), and the Assessment and Collection of Taxes Law (ACTL), along with the Regulatory Administrative Act (Κ.Δ.Π.) 110/2025. While the BLJ measures, particularly withholding taxes (WHTs), became effective in April 2025, the LTJ measures, encompassing WHTs and deduction denials, are appliable from January 2026.

I. Key Provisions

For the purposes of these new measures, a “non-cooperative jurisdiction” or BLJ is defined as a third-country jurisdiction included in the latest updated Annex I of the EU list of non-cooperative jurisdictions for tax purposes, as published in the Official Journal of the European Union in the previous calendar year. As of October 2024, this list comprises 11 countries: American Samoa, Anguilla, Fiji, Guam, Palau, Panama, Russia, Samoa, Trinidad and Tobago, US Virgin Islands, and Vanuatu.

A “jurisdiction with a low corporate tax rate” is identified as a third-country jurisdiction where the corporate tax rate is less than 50% of Cyprus’ corporate tax rate, equating to less than 6.25%. A potential list of LTJ can be derived from the Tax Foundation list of Countries Without General Corporate Income Tax 2024 and the Dutch list of states without a profit tax or with a profit tax at a rate of less than 9% (Bahamas, Bahrain, Belize, Bermuda, British Virgin Islands, Cayman Islands, Guernsey, Isle of Man, Jersey, Saint Barthelemy, Tokelau, Turks and Caicos Islands, Wallis and Futuna Islands).

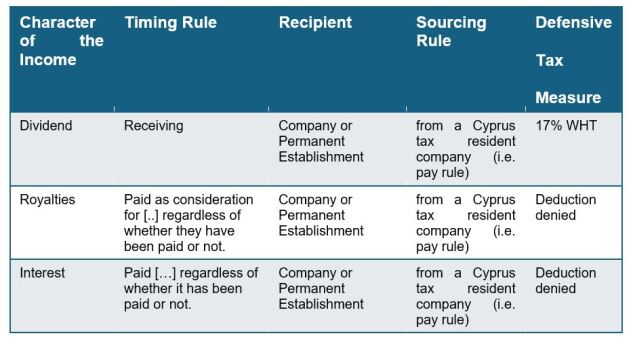

Table 1: Tax Issues To Consider for Payments Made to Low-Tax Jurisdictions (Effective Date Jan. 1, 2026)

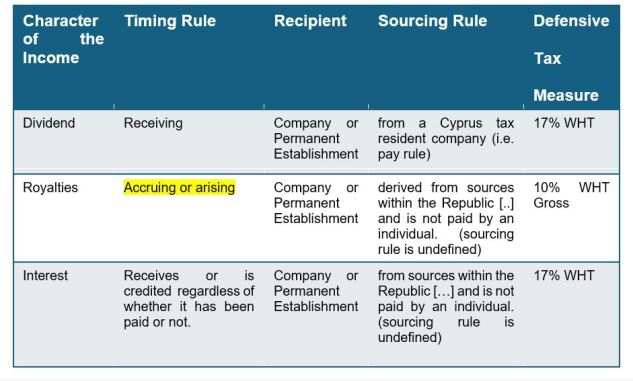

Table 2: Tax Issues To Consider for Payments Made to Blacklisted Jurisdictions (Already in force)

Notably, the new defensive measures are expected to apply to a significant number of recipients as the ITL provides for a broad definition of the term “company” that has the meaning assigned to this term by the Cyprus Companies Law and includes any body with or without legal personality, or public corporate body, as well as every company, fraternity or society of persons, with or without legal personality, including any comparable company incorporated or registered outside the Republic and a company listed in the First Schedule; but it does not include a partnership.

It is important to note that, unlike the denial of deduction for interest and royalty payments under the LTJ and the imposition of withholding tax on LTJ and BLJ, where the sourcing rule for payments made to non-residents is determined by the residency of the payer (i.e., a “pay” rule), the legislative provisions governing WHT on payments made to BLJ for interest and royalties do not define a specific sourcing rule. Accordingly, both the “pay” rule and the “use” rule should be taken into account when assessing the applicable withholding tax obligations.

Finally, the new tax law is silent for payments made or notional payments under the Authorised OECD Approach by Cyprus permanent establishments to LTJ or NCJ.

A. ITL Amendments: Erosion of Deductions and New Withholding Taxes

The amendments to the ITL introduce significant changes, primarily focusing on the denial of deductions for certain payments and the imposition of new WHTs.

1. Non-Deductible Expenses (ITL art. 11(17))

This pivotal provision targets IP-related payments and interest payments made by Cyprus-resident companies. Specifically, deductions are disallowed for:

Payments (or accrued amounts) for intellectual property rights, exploitation rights, compensation rights, copyrights, trademarks, design rights, secret manufacturing processes, types, processes, or any “similar property”; andInterest payments (whether paid or accrued).

These disallowances apply when such payments are made to a company that is either tax resident in a low-tax jurisdiction or incorporated/registered in a low-tax jurisdiction and not tax resident in a jurisdiction with a non-low tax rate.

A crucial aspect of article 11(17)(a) is its application to “connected persons”. The provision explicitly limits its scope to payments made within a control relationship. This means it applies only if:

The recipient company directly or indirectly controls the Cyprus payer, holding more than 50% of voting rights, capital, or profit share; orThe Cyprus payer similarly controls the recipient; orA common third party (individual or entity) controls both the Cyprus payer and the recipient with a similar threshold. This 50% threshold covers both vertical and lateral ownership chains.

The definition of “connected persons” for these rules is broad, encompassing not only direct or indirect control (>50% voting rights, capital, or profit share) but also spousal or familial relationships up to the third degree, including in-laws.

An exemption for listed securities exists, whereby interest paid on securities listed on a recognized stock exchange is excluded. However, this carve-out does not apply if the Cyprus payer is aware that the interest is ultimately paid to a controlled low-tax entity, demonstrating a knowledge-based anti-abuse mechanism.

The rules also extend to:

Permanent establishments (PEs) of foreign companies located in low-tax jurisdictions, with a carve-out if the PE’s parent company is tax resident in a non-low-tax, non-blacklisted jurisdiction; and Certain conditions related to taxation at a minimum 15% rate (e.g., under Pillar Two EU Directive or OECD GloBE Rules) are met.

Perhaps the most significant element is the embedded General Anti-Avoidance Rule (GAAR). This clause is triggered if a “regulation or series of regulations” has been implemented with a main purpose (or one of the main purposes) of obtaining a tax advantage that undermines the section’s intent, and critically, lacks valid commercial reasons reflecting economic reality. The application of this GAAR is governed by a Ministerial Decree (Κ.Δ.Π. 110/2025). According to this Ministerial Decree, the GAAR is triggered if the recipient company fails to comply with two or more specific substance-related criteria, including:

At least one board member having the qualifications and authority to make decisions related to the company’s revenue-generating activities, assets, or rights, and performing their duties actively and independently. At least one member of its decision-making board of directors being resident in the recipient company’s tax jurisdiction (or within daily commuting distance). The company having office premises where its directors and employees perform their duties in its tax jurisdiction. The majority of board meetings being held in the recipient company’s tax jurisdiction. Operating expenses (including directors’ fees and personnel costs) paid to persons within the recipient company’s tax jurisdiction being commensurate with its activities. The group structure not being solely designed for the recipient company to collect interest or royalties and transfer almost all of it to an affiliated company, resulting in negligible taxable profit to facilitate capital flow to the beneficial owner. This detailed list of criteria for substance aims to challenge artificial arrangements and promote genuine economic activity.

Importantly, to avoid double taxation or overreach, ITL article 11(17)(a) does not apply if the expenses are already subject to WHT under ITL article 21 (general WHT on royalties) or SDCL article 3(2)(b1) (WHT on interest to BLJs). Notably, BLJ provisions take priority over LTJ provisions.

2. Tax on Payments to Non-Cooperative Jurisdictions (ITL art. 21A)

This article specifically addresses payments to BLJs. It imposes a 10% tax on any gross amount of income derived from Cyprus as consideration for the use or right to use IP or similar intangible rights. This tax applies if the recipient is a non-resident company that is either resident in a non-cooperative jurisdiction or incorporated/registered there and not tax resident elsewhere in a cooperative jurisdiction. Payments made by individuals are explicitly excluded from this tax, focusing its application on corporate-level arrangements. Furthermore, article 21A ensures no duplication, as it does not apply to payments already subject to WHT under article 21 of the ILT. Provisions regarding associated enterprises, connected persons, GAAR, and permanent establishments in article 21A of the ILT are broadly similar to those in article 11(17)(a) of the ITL.

3. Treaty Renegotiation (ITL art. 34(3))

Cyprus has also legislated an obligation to initiate renegotiation of its double tax treaties (DTTs) under specific circumstances. This obligation is triggered if a treaty counterparty is:

A low-tax jurisdiction, and the existing treaty does not allocate taxing rights to Cyprus on dividends paid to residents of that jurisdiction; and Listed in Annex I of the EU list of non-cooperative jurisdictions, and the treaty does not allocate taxing rights to Cyprus on dividends, interest, or royalties paid to residents of that jurisdiction. In both scenarios, the renegotiation obligation arises three years after the jurisdiction’s classification as low-tax or its inclusion in Annex I of the EU list of NCJs. Transitional provisions apply for jurisdictions already listed or qualifying when the 2025 law was published. This signals Cyprus’ intent to align its treaty network with its new defensive measures.

B. Special Defence Contribution Law Amendments: Dividend and Interest Withholding Taxes

The SDCL introduces new WHTs on dividend and interest payments.

1. WHT on Dividend Payments (SDCL art. 3(2)(a1))

A 17% WHT is now imposed on dividends paid by a Cyprus tax-resident company to a non-resident company if two conditions are met:

Recipient Jurisdiction Status: The recipient company is either resident in an LTJ (or incorporated/registered there and not resident in a cooperative jurisdiction) OR resident in an NCJ (or incorporated/registered there and not tax resident elsewhere); andOwnership/Control Link: A control relationship exceeding 50% exists, either through the recipient controlling the Cyprus payer, the Cyprus payer controlling the recipient, or a common person/persons controlling both entities, assessed via voting rights, capital ownership, or entitlement to profits.

The SDCL also includes deemed dividend provisions to prevent anti-avoidance. If assets are distributed as part of a capital reduction and their value exceeds the paid-up capital, the excess is treated as a dividend subject to the 17% WHT. Additionally, any asset transfer for profit distribution or capital reduction must be assessed at market value to deter artificial undervaluation. The provisions regarding application to associated enterprises, definition of connected persons, exemption for listed securities, GAAR, the application to PEs and Pillar 2 rules are broadly similar to those found in ITL Article 11(17)(a).

2. WHT on Interest Payments (SDCL art. 3(2)(b1))

A 17% WHT is imposed on interest income received or credited (even if not paid) to a non-resident company, provided the recipient company is in a non-cooperative jurisdiction (or incorporated/registered there and not tax resident in a cooperative jurisdiction) and the interest arises from sources within Cyprus (excluding certain deposit interest and interest not paid by an individual). Similar to the dividend and ITL provisions, aspects such as application to associated enterprises, connected persons, listed securities exemption, GAAR, and PE rules are broadly aligned.

C. ACTL Amendments: Enforcement Through Fines

To ensure enforceability, article 50H of the ACTL introduces a structured administrative fine system for non-compliance with the transparency, substance, and information-retention requirements under the new ITL and SDCL provisions. These compliance obligations include performing due diligence, maintaining documentation, and making audits available to the Tax Department.

A graduated penalty regime has been established for non-compliance following a 60-day grace period:

For delays between day 61 and day 90, a fine of EUR 2,000 is imposed. For delays between day 91 and day 120, the fine increases to EUR 4,000. For delays of day 121 or never, the fine reaches EUR 10,000. If the fine is not paid voluntarily, the Commissioner may initiate civil proceedings, as the fine is treated as a civil debt owed to the Republic of Cyprus.II. Conclusion

Cyprus’ recent tax reforms represent a comprehensive effort to address international concerns regarding tax avoidance through LTJs and BLJs. By introducing strict deduction denials, new withholding taxes, mandatory DTT renegotiations, and administrative fines for non-compliance, Cyprus is actively enhancing its tax transparency and demonstrating its commitment to global tax standards. Businesses with existing or planned holding, financing, and intellectual property structures involving Cyprus and these jurisdictions must urgently assess their current arrangements to ensure full compliance, review their operational

This article does not necessarily reflect the opinion of Bloomberg Industry Group, Inc., the publisher of Bloomberg Law, Bloomberg Tax, and Bloomberg Government, or its owners.

Author Information

Christos Theophilou is a tax partner at STI Taxand in Cyprus.

Write for Us: Author Guidelines.