I guess I’m too dumb to understand what’s going on here

Do you think that we are having a labor pull back but it is hidden by people doing uber?

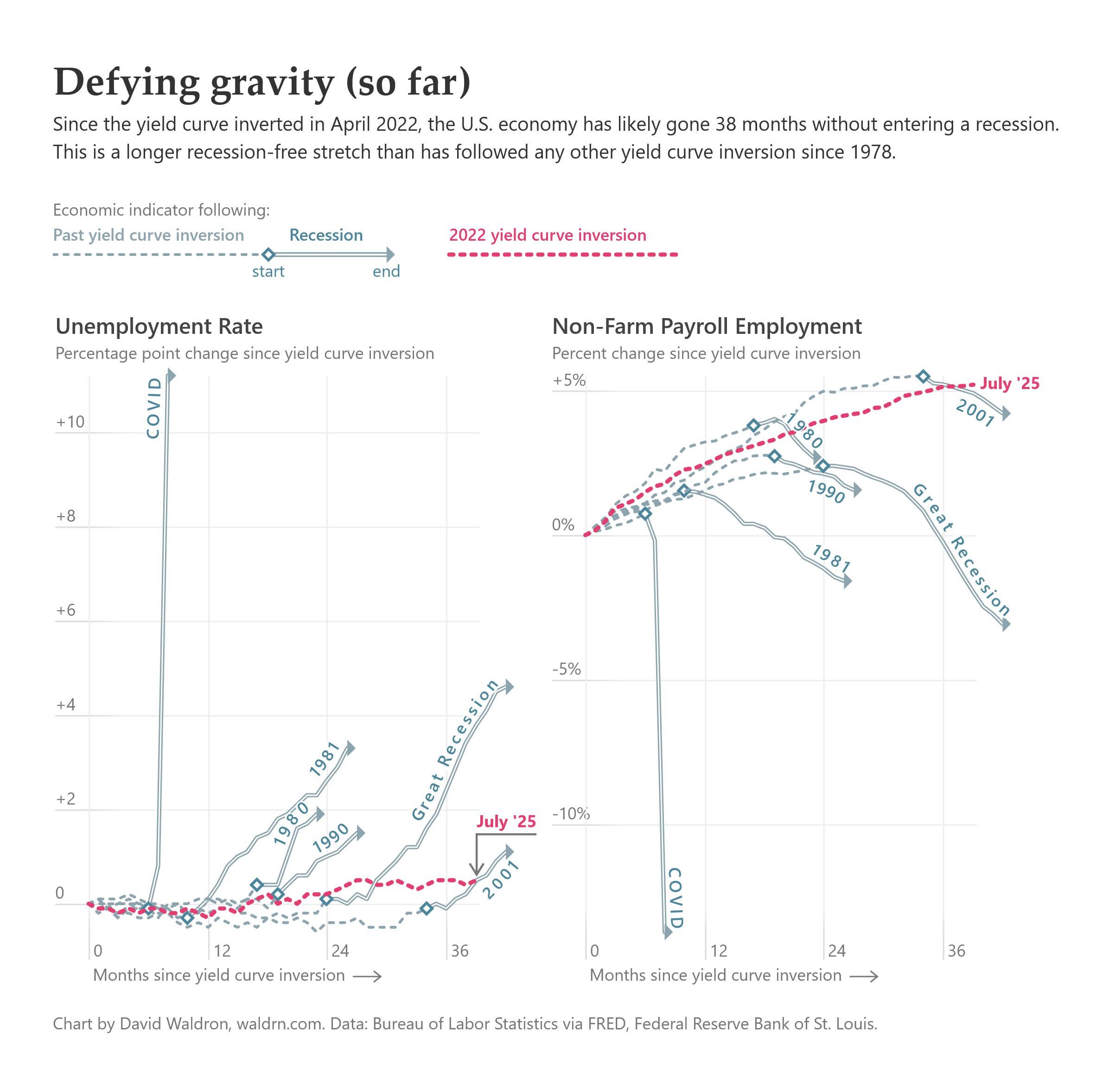

Actual beautiful data on this sub, nice work.

This is well done and well presented. Took a bit to understand, but it’s all there and makes sense. Nicely done.

The likely answer is because of relatively enormous cash injection from private capital investment in AI infrastructure (data centres). (It’s ~2% of US GDP despite being less than 0.1% in 2022).

So lots of companies pouring as much cash as they can in covers what would normally be a recession.

The issue is that data center infrastructure really is not as robust and durable as previous large scale private investment infrastructure, I.e. the rate at which you have to replace them is much more than something like train lines.

A good read here for anyone who wants more https://paulkedrosky.com/honey-ai-capex-ate-the-economy/

My takeaway from this is covid even mire fucked up than I remember, and I remember it was fucked up…

Yield curve inversions predicting recessions was always a stupid take. There are multiple problems but the quick version is that it made sense only in a falling rate environment where inflation was a secondary concern of the central bank. As soon as rates bounced off of historic lows and inflation became the leading concern it breaks down because a central bank can cut rates for two reasons: (a) it is worried about unemployment rising (as the yield curve fanatics know) or (b) because inflation has been successfully tackled (which boggled the minds of the sort of people who put so much weight in the yield curve). Those using the yield curve inversion as a worthwhile predictor post 2020 have essentially confused (b) with (a).

Rates inverted (i.e. people thought long term rates would be lower than current rates) not because unemployment would rise but because people expected that inflation would be successfully overcome causing people to understand that the rates of a year or two ago were unsustainably and in the medium term unnecessarily high.

This is good data and pretty well presented except for the missing examples where the yield curve inverted but no recession was captured.

1966

1980-1981 lasting 410 days. With recessions “bookends”

1998

It would be nice to see it compared to these other years

So I guess the big question is how long can we Wile E Coyote this and keep going before we realize how far off the cliff we are and is there somewhere safe to land

![[OC] U.S. labor market trend since the 2022 yield curve inversion](https://www.europesays.com/wp-content/uploads/2025/08/cqtbax4fczgf1-1920x1024.jpeg)

10 comments

Data is from BLS via FRED (PAYEMS and UNRATE).

Tools used were R and d3.js.

[Full blog post](https://blog.waldrn.com/p/is-the-yield-curve-still-useful-for). Also Reddit’s image compression seems to have really butchered this one so there’s a higher-res one in the post.

I guess I’m too dumb to understand what’s going on here

Do you think that we are having a labor pull back but it is hidden by people doing uber?

Actual beautiful data on this sub, nice work.

This is well done and well presented. Took a bit to understand, but it’s all there and makes sense. Nicely done.

The likely answer is because of relatively enormous cash injection from private capital investment in AI infrastructure (data centres). (It’s ~2% of US GDP despite being less than 0.1% in 2022).

So lots of companies pouring as much cash as they can in covers what would normally be a recession.

The issue is that data center infrastructure really is not as robust and durable as previous large scale private investment infrastructure, I.e. the rate at which you have to replace them is much more than something like train lines.

A good read here for anyone who wants more https://paulkedrosky.com/honey-ai-capex-ate-the-economy/

My takeaway from this is covid even mire fucked up than I remember, and I remember it was fucked up…

Yield curve inversions predicting recessions was always a stupid take. There are multiple problems but the quick version is that it made sense only in a falling rate environment where inflation was a secondary concern of the central bank. As soon as rates bounced off of historic lows and inflation became the leading concern it breaks down because a central bank can cut rates for two reasons: (a) it is worried about unemployment rising (as the yield curve fanatics know) or (b) because inflation has been successfully tackled (which boggled the minds of the sort of people who put so much weight in the yield curve). Those using the yield curve inversion as a worthwhile predictor post 2020 have essentially confused (b) with (a).

Rates inverted (i.e. people thought long term rates would be lower than current rates) not because unemployment would rise but because people expected that inflation would be successfully overcome causing people to understand that the rates of a year or two ago were unsustainably and in the medium term unnecessarily high.

This is good data and pretty well presented except for the missing examples where the yield curve inverted but no recession was captured.

1966

1980-1981 lasting 410 days. With recessions “bookends”

1998

It would be nice to see it compared to these other years

So I guess the big question is how long can we Wile E Coyote this and keep going before we realize how far off the cliff we are and is there somewhere safe to land

Comments are closed.