William Clayton, a businessman who served successive US presidents and became one of the chief architects of the Marshall Plan, was no fan of tariffs. He rated the barriers erected during the Great Depression as one of the great crimes of the century. So it’s hard to imagine that Clayton, who believed that free trade was as important to prosperity as American aid and security guarantees, would remotely approve of Donald Trump’s efforts to reshape commerce.

The ongoing White House-engineered upheaval, which has pushed tariffs to levels unseen since the Smoot-Hawley law of 1930, will be costly—even if the full price isn’t immediately apparent. The global economy hasn’t suffered some of the direst consequences that were predicted in April. Demand for US assets has held up, despite the superficial allure of the ‘sell America’ narrative. The International Monetary Fund doubts growth will suddenly crater, and inflation hasn’t taken off. Has a bullet been dodged or is shock delaying the pain?

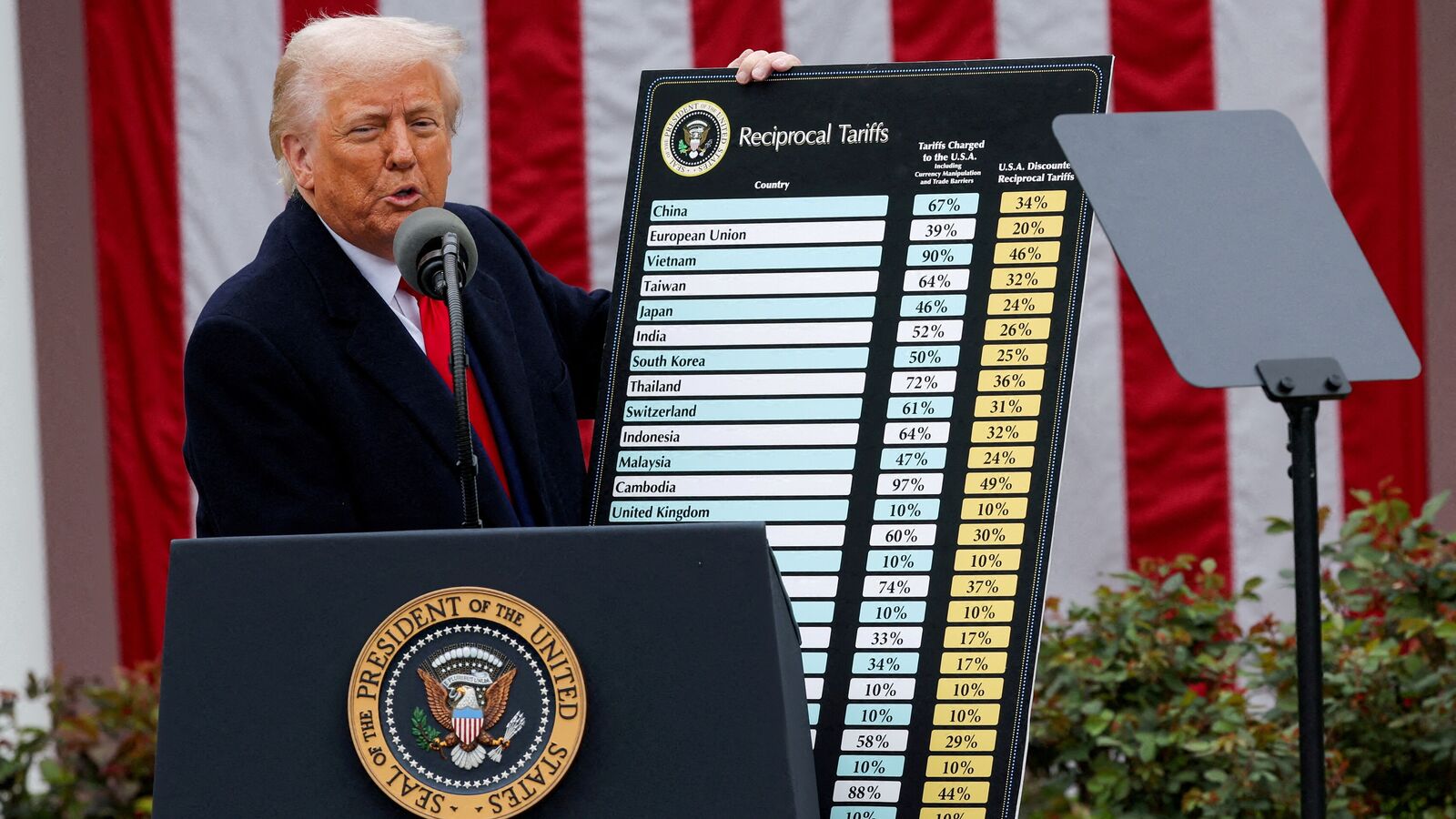

Also Read: Trump trade advisor Navarro’s diatribe against India is self-serving and narrow

It’s notable that countries aren’t exactly lining up to fire back. With the exception of China, which has escalated and retreated to match the White House rhythms, there’s been little by way of reprisals. “It’s not a war when only one side fights,” JPMorgan Chase economists said in a recent note. “The primary drag from the trade war will come from US tariff hikes, but we also looked for broad retaliation by US trading partners.” The counter-attack “has not materialized; in fact, barriers to US exports have been lowered,” they wrote.

By no means does the firm anticipate zero harm. Business confidence is down but not collapsing. Capital spending will be constrained. And while chances of recession are still high, a better outcome remains very plausible. This sort of guarded optimism—or qualified pessimism—is a break from the dark warnings.

Christine Lagarde, head of the European Central Bank, told leaders to prepare for a worst-case scenario where the US drags the world into destructive economic conflict. Canadian Prime Minister Mark Carney declared that relations with the US would be changed forever. Chinese President Xi Jinping has studiously matched American moves but also toned down his rhetoric and actions when appropriate. Washington and Beijing recently extended a pause on higher tariffs for 90 days.

Also Read: Bide your time: China’s playing a long game in its trade talks with America

India, which has been the subject of some bullish projections as China’s economy has slowed, is one of the few economies of significance that hasn’t cut a deal with Trump. But Prime Minister Narendra Modi also hasn’t gone measure for measure or shown a desire to get even with US businesses.

Yes, there has been indignity and hurt feelings. The governor of the Reserve Bank of India dismissed Trump’s claim that commerce was dead there. He touted India’s contribution to global growth—about 18% compared to around 11% for the US—and insisted the local economy was doing well. But this misses the fact that in pure size, America dwarfs India.

Brazil, a comer that struggles to make good on its potential, is also refusing to bend. President Luiz Inacio Lula da Silva loathes dependence on the US and wants to be treated as an equal. But Trump doesn’t like a court case against Lula’s predecessor for allegedly plotting a coup. Brazil is trying to develop an alternative to the dollar and places great store in commercial ties within the Brics group. Many of those nations and aspiring members have cut deals with Trump, or are likely to do so. Brazil will probably come to some arrangement.

Also Read: Barry Eichengreen: Trump’s trade offensive echoes Thatcher’s Falklands War

So has Trump gotten away with it? His aides reckoned access to the US market is too lucrative to pass up. They may have been right. It would also be naive to conclude there won’t be any cost. The global economy has slowed but not crashed, foreigners still purchase US Treasuries and it’s a safe bet that the greenback will be at the centre of the financial system for years.

But the nations humiliated won’t forget this experience. Asia’s economies will only get bigger and the siren call of greater integration with China will get louder. Trump’s efforts to destroy the existing order may yet prove an own goal. Just not this year.

Clayton, who became the top economic official at the State Department, believed that robust trade among shattered Western European nations was as important as physical rebuilding. The economic dislocation wrought by the conflagration had been underestimated; capitalism could revive the continent and prevent the political implosion of key countries.

According to Benn Steil’s book The Marshall Plan: Dawn of the Cold War, Clayton insisted that the US “must run this show.” Trump’s team brags about re-configuring the system that grew from the ideals of the post-war era. The hubris may ultimately prove misplaced. ©Bloomberg

The author is a Bloomberg Opinion columnist covering Asian economies.