Sinohope Technology Holdings Limited (HKG:1611) shares have continued their recent momentum with a 37% gain in the last month alone. The last month tops off a massive increase of 250% in the last year.

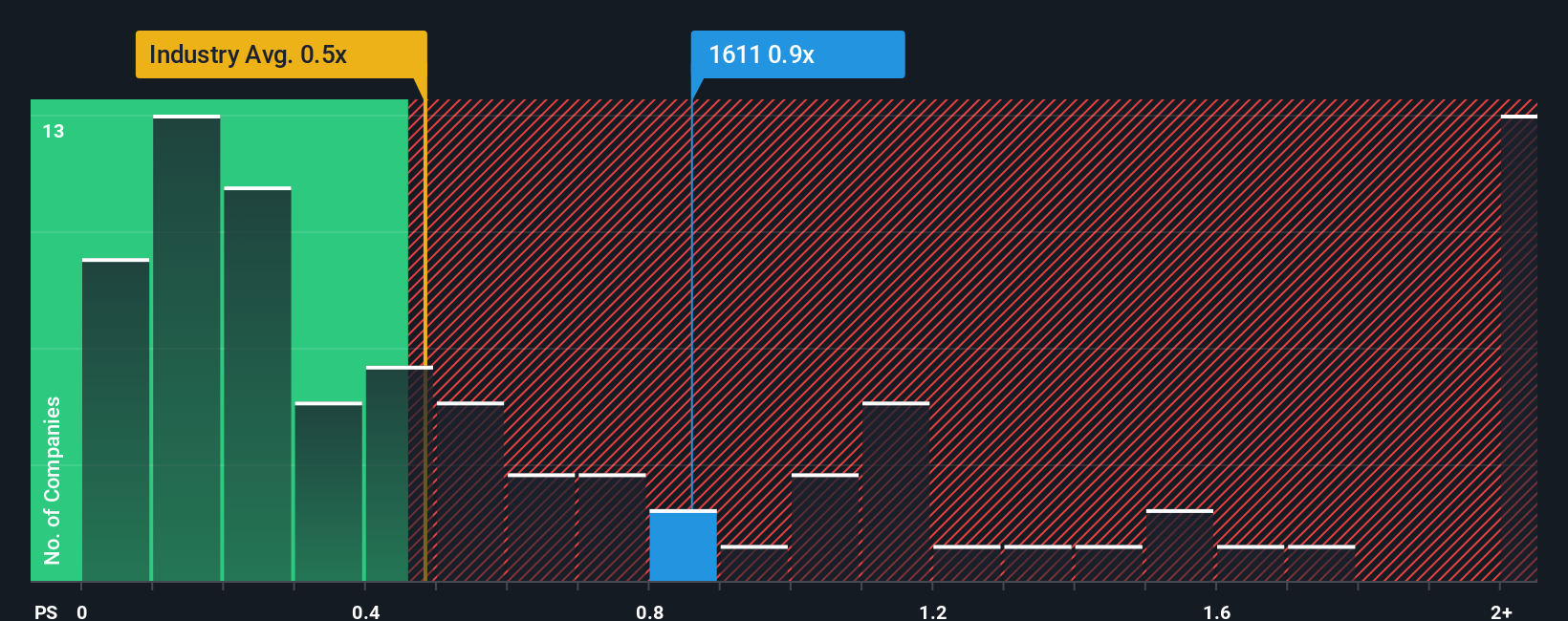

Even after such a large jump in price, you could still be forgiven for feeling indifferent about Sinohope Technology Holdings’ P/S ratio of 0.9x, since the median price-to-sales (or “P/S”) ratio for the Electronic industry in Hong Kong is also close to 0.5x. While this might not raise any eyebrows, if the P/S ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

See our latest analysis for Sinohope Technology Holdings

SEHK:1611 Price to Sales Ratio vs Industry August 31st 2025 What Does Sinohope Technology Holdings’ Recent Performance Look Like?

SEHK:1611 Price to Sales Ratio vs Industry August 31st 2025 What Does Sinohope Technology Holdings’ Recent Performance Look Like?

Recent times have been quite advantageous for Sinohope Technology Holdings as its revenue has been rising very briskly. The P/S is probably moderate because investors think this strong revenue growth might not be enough to outperform the broader industry in the near future. If you like the company, you’d be hoping this isn’t the case so that you could potentially pick up some stock while it’s not quite in favour.

Although there are no analyst estimates available for Sinohope Technology Holdings, take a look at this free data-rich visualisation to see how the company stacks up on earnings, revenue and cash flow. What Are Revenue Growth Metrics Telling Us About The P/S?

There’s an inherent assumption that a company should be matching the industry for P/S ratios like Sinohope Technology Holdings’ to be considered reasonable.

Taking a look back first, we see that the company’s revenues underwent some rampant growth over the last 12 months. Spectacularly, three year revenue growth has also set the world alight, thanks to the last 12 months of incredible growth. Accordingly, shareholders would have been over the moon with those medium-term rates of revenue growth.

Comparing that recent medium-term revenue trajectory with the industry’s one-year growth forecast of 16% shows it’s noticeably more attractive.

With this information, we find it interesting that Sinohope Technology Holdings is trading at a fairly similar P/S compared to the industry. Apparently some shareholders believe the recent performance is at its limits and have been accepting lower selling prices.

The Final Word

Its shares have lifted substantially and now Sinohope Technology Holdings’ P/S is back within range of the industry median. Typically, we’d caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

To our surprise, Sinohope Technology Holdings revealed its three-year revenue trends aren’t contributing to its P/S as much as we would have predicted, given they look better than current industry expectations. It’d be fair to assume that potential risks the company faces could be the contributing factor to the lower than expected P/S. While recent revenue trends over the past medium-term suggest that the risk of a price decline is low, investors appear to see the likelihood of revenue fluctuations in the future.

Having said that, be aware Sinohope Technology Holdings is showing 3 warning signs in our investment analysis, and 2 of those are concerning.

If these risks are making you reconsider your opinion on Sinohope Technology Holdings, explore our interactive list of high quality stocks to get an idea of what else is out there.

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.