LONDON, Oct 1 (Reuters) – The old truism that the stock market is not the economy risks underplaying how much today’s powerful investment trends could impact the prosperity and lives of the whole country.

Sign up here.

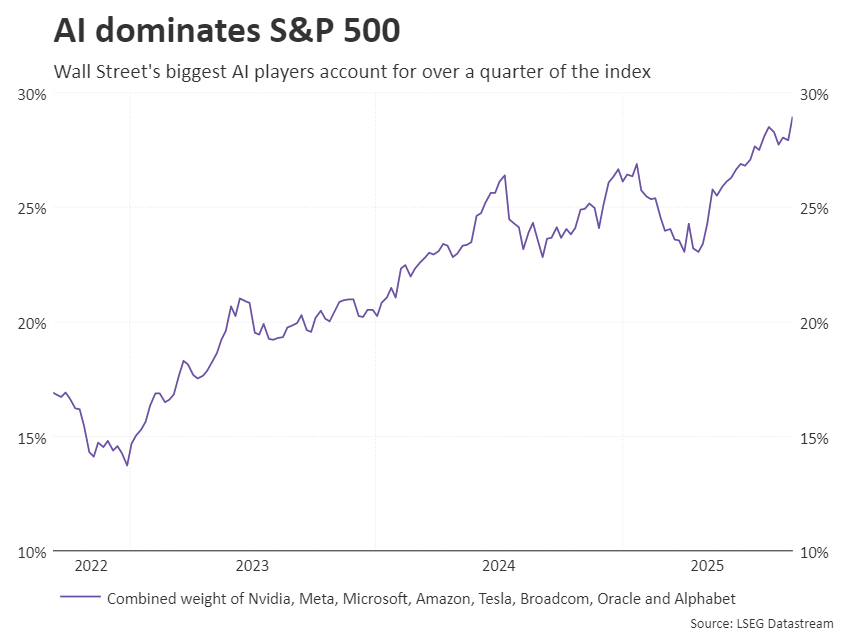

The so-called Magnificent Seven – U.S. tech companies that now make up a record 36% of the S&P 500’s market value – have seen their stock prices more than double over the past two years, after rebounding a whopping 60% from the troughs of this year.

AI dominates S&P 500

Whether this is a bubble is perhaps the biggest question facing the stock market and the U.S. economy at large.

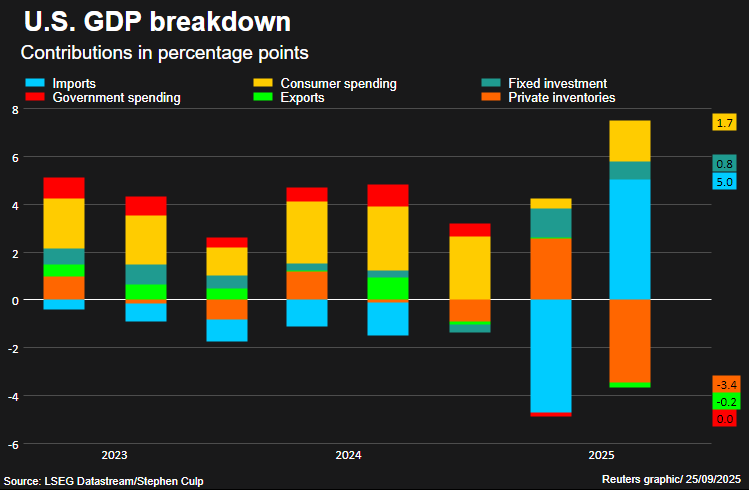

While the extraordinary capital expenditure on AI over the past year may only represent about 1% of U.S. GDP, its impact on growth has been massive.

That growth may have slowed a bit this quarter, but not much.

GDP contributors

What’s more, spending on data centers and infrastructure investment – up fourfold since 2020 – is fueling construction and wider industrial sector activity to boot.

In short, AI better work – or else.

THE MUSIC’S STILL PLAYING

The AI arms race is unlikely to grind to a halt any time soon.

Many questions about AI remain unanswered.

If you believe this is the future, with all the seismic impact on labor demand and productivity that adherents forecast, then it’s hard to see disappointment or reversal being a narrow investment event.

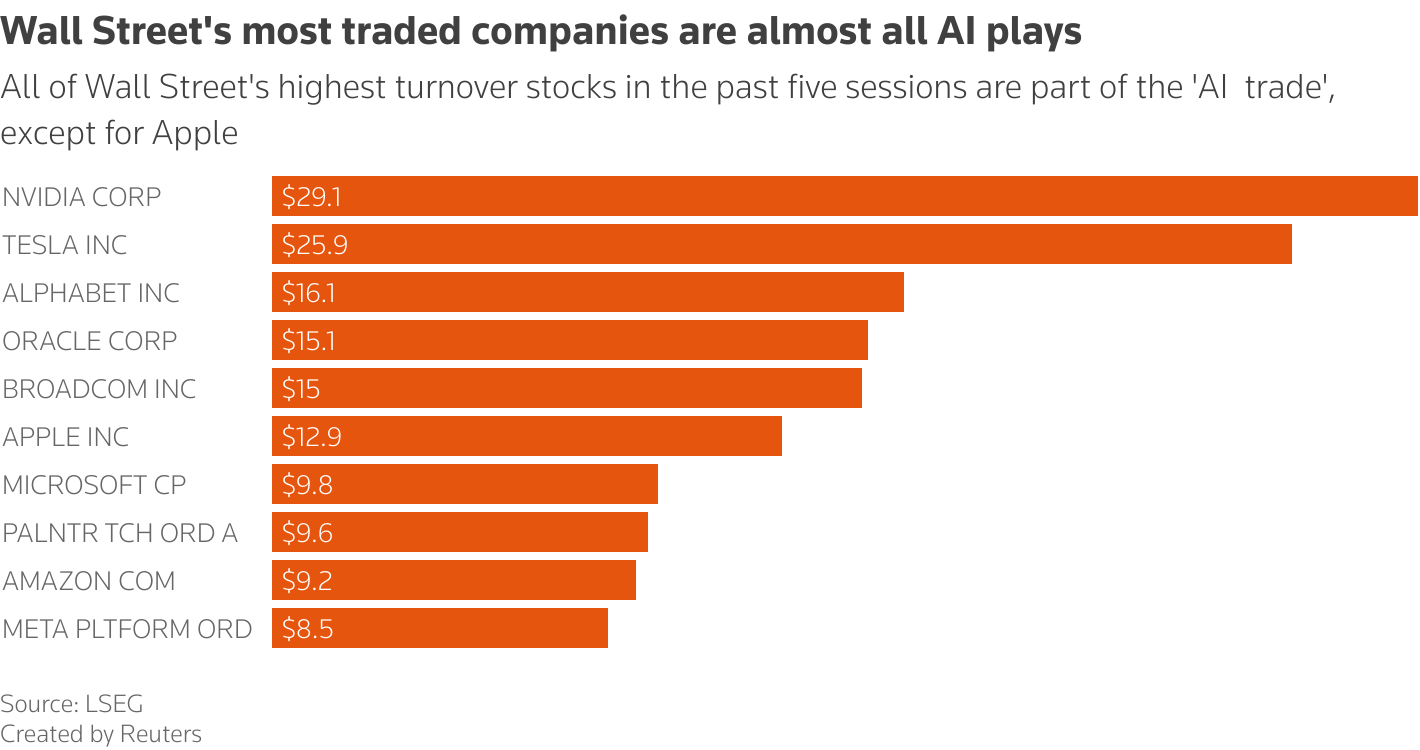

All of Wall Street’s highest turnover stocks in the past five sessions are part of the ‘AI trade’, except for Apple

If AI is a bubble and it bursts, it will likely reverberate through the real economy – both independently of and through the equity market.

One retort is to look back at the dotcom bubble that burst in 2000. That tech stock mania reversed without the entire economy collapsing – and some of the companies that survived eventually became today’s behemoths.

Interest rate cuts and a housing rebound partly saved the day back then. And it’s conceivable that we could see a repeat this time around in the event of a sudden AI market implosion.

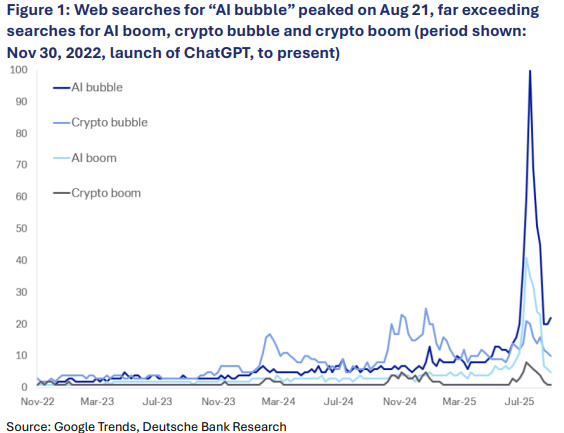

Deutsche Bank chart on web searches for “Ai bubble”

But skeptics certainly see the froth as well as the future in recent events.

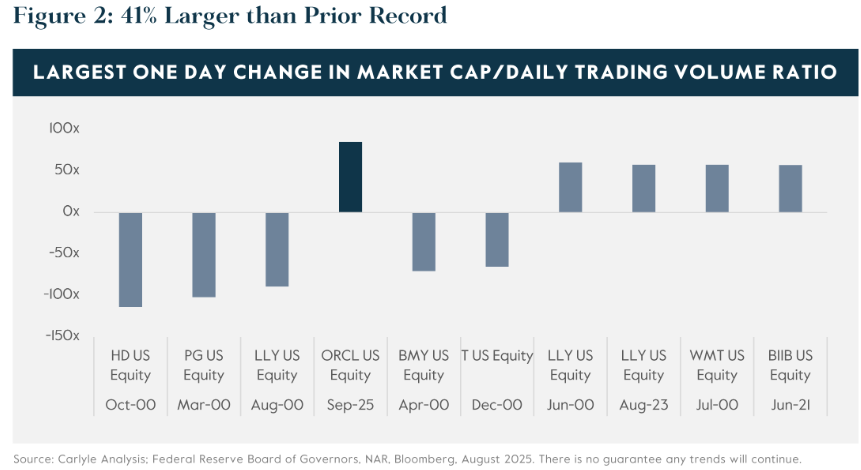

Thomas described the Oracle move, which was prompted by news of AI-related cloud contracts with OpenAI and others, as “the rarest of rare events,” with a single-day change in value equal to 85 times the stock’s average daily trading volume.

Carlyle chart on the historic scale of Oracle one-day price jump last month

The near tripling of its stock price over two years, to deliver a market cap that briefly topped a trillion dollars last month, is stunning given Oracle’s other underlying numbers.

Thomas points out that to deliver on the OpenAI deal, Oracle will have to lift its own capital spending by almost $100 billion over the next two years, an annualized growth rate of some 47%, even though its free cash flow has already fallen into negative territory for the first time since 1990.

There may be trouble ahead. If there is, the whole economy will shudder.

The opinions expressed here are those of the author, a columnist for Reuters

by Mike Dolan; Editing by Marguerita Choy

Our Standards: The Thomson Reuters Trust Principles., opens new tab

Opinions expressed are those of the author. They do not reflect the views of Reuters News, which, under the Trust Principles, is committed to integrity, independence, and freedom from bias.