The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 24 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

Redwire Investment Narrative Recap

At its core, the Redwire story is about believing in the acceleration of commercial space infrastructure, and the Axiom Space contract ties the company to one of the most visible next-generation commercial space stations. While this win does not fundamentally change Redwire’s biggest near-term challenge, achieving stable, profitable growth amid unpredictable government funding cycles and cost management on complex engineering projects, it does reinforce its role as a key commercial partner, potentially mitigating some revenue risks in the short term.

Among recent announcements, Redwire’s $25 million IDIQ contract with NASA for biotechnology facilities aboard the ISS stands out as both a signal of diversification and alignment with new commercial revenue streams beyond its core engineering contracts. This initiative in space-based pharmaceuticals connects directly to the company’s ability to weather volatility in government awards by building up commercial business lines and recurring revenues that support long-term resilience.

However, investors should also pay close attention to the risks tied to Redwire’s reliance on large, technically complex fixed price contracts, as cost overruns or EAC volatility can quickly affect margins and…

Read the full narrative on Redwire (it’s free!)

Redwire’s narrative projects $887.3 million in revenue and $73.2 million in earnings by 2028. This requires 50.3% annual revenue growth and a $322.7 million increase in earnings from -$249.5 million today.

Uncover how Redwire’s forecasts yield a $18.06 fair value, a 74% upside to its current price.

Exploring Other Perspectives RDW Community Fair Values as at Oct 2025

RDW Community Fair Values as at Oct 2025

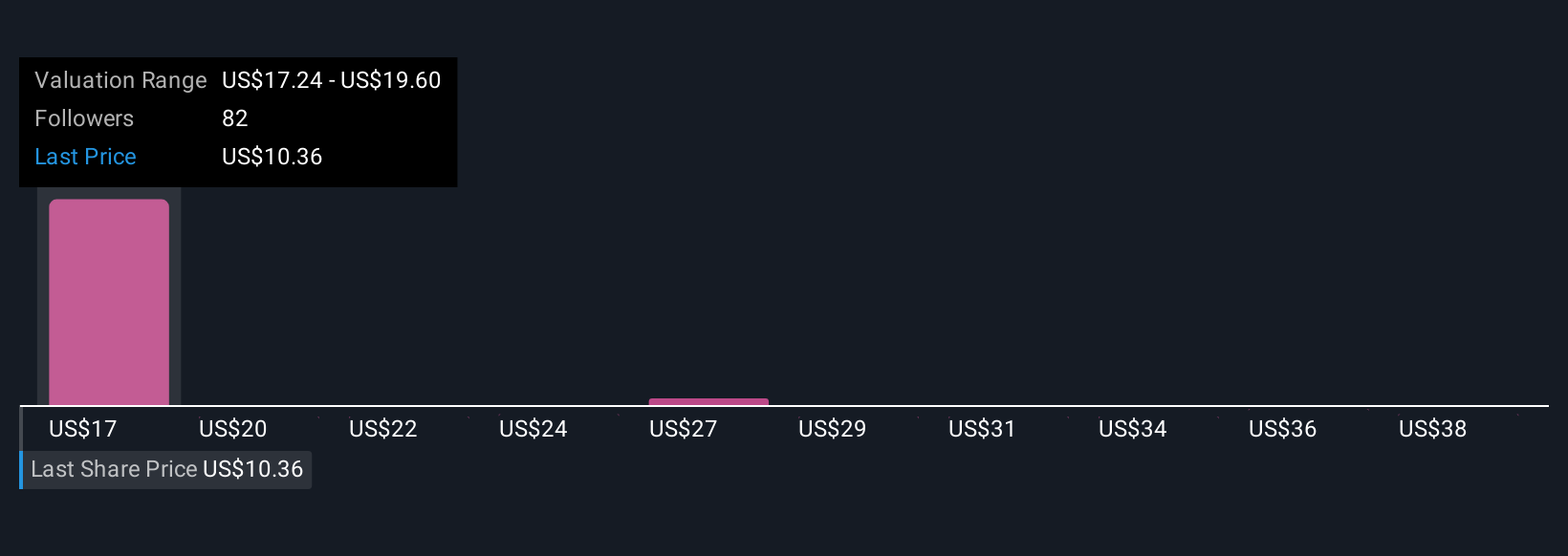

Ten recent estimates from the Simply Wall St Community put Redwire’s fair value anywhere from US$17.24 to US$40.80 per share. While community forecasts vary, ongoing exposure to large fixed price development contracts continues to raise earnings uncertainty and cost risk for Redwire’s business outlook.

Explore 10 other fair value estimates on Redwire – why the stock might be worth just $17.24!

Build Your Own Redwire Narrative

Disagree with existing narratives? Create your own in under 3 minutes – extraordinary investment returns rarely come from following the herd.

Ready For A Different Approach?

Markets shift fast. These stocks won’t stay hidden for long. Get the list while it matters:

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com