See our latest analysis for Marathon Petroleum.

After a remarkable run-up earlier in the year, Marathon Petroleum’s recent share price pullback suggests the market is pausing to reassess the outlook amid changing sector winds. Momentum remains strong overall, with a year-to-date share price return of nearly 28% and a 12.7% total shareholder return over the past twelve months. Confidence in the company’s long-term performance appears resilient, especially given its sizable five-year total return.

If you’re watching industry moves and want fresh ideas, this is the perfect moment to discover fast growing stocks with high insider ownership.

With strong historic returns and a recent pullback, the question now looms: does Marathon Petroleum remain undervalued by the market, or has its impressive growth potential already been fully priced in?

Most Popular Narrative: 4.4% Undervalued

Marathon Petroleum’s most followed valuation view puts its fair value at $189.17, just above the last close of $180.89. All eyes are on whether upbeat refinery margins and sector tailwinds can keep up the pace.

Bullish analysts cite robust refining margins and strong margin capture, with recent quarters outperforming expectations and margin strength persisting despite calls for a decline.

Curious about what’s driving this positive valuation? It all revolves around anticipated margin improvements and bold profit projections, layered on top of controversial analyst growth assumptions. There is more to the story, so don’t miss what’s behind the fair value number.

Result: Fair Value of $189.17 (UNDERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, rising electrification and tougher environmental policies could erode demand for refined fuels. This could put pressure on Marathon Petroleum’s future revenue and margins.

Find out about the key risks to this Marathon Petroleum narrative.

Another View: Peering Through the Earnings Lens

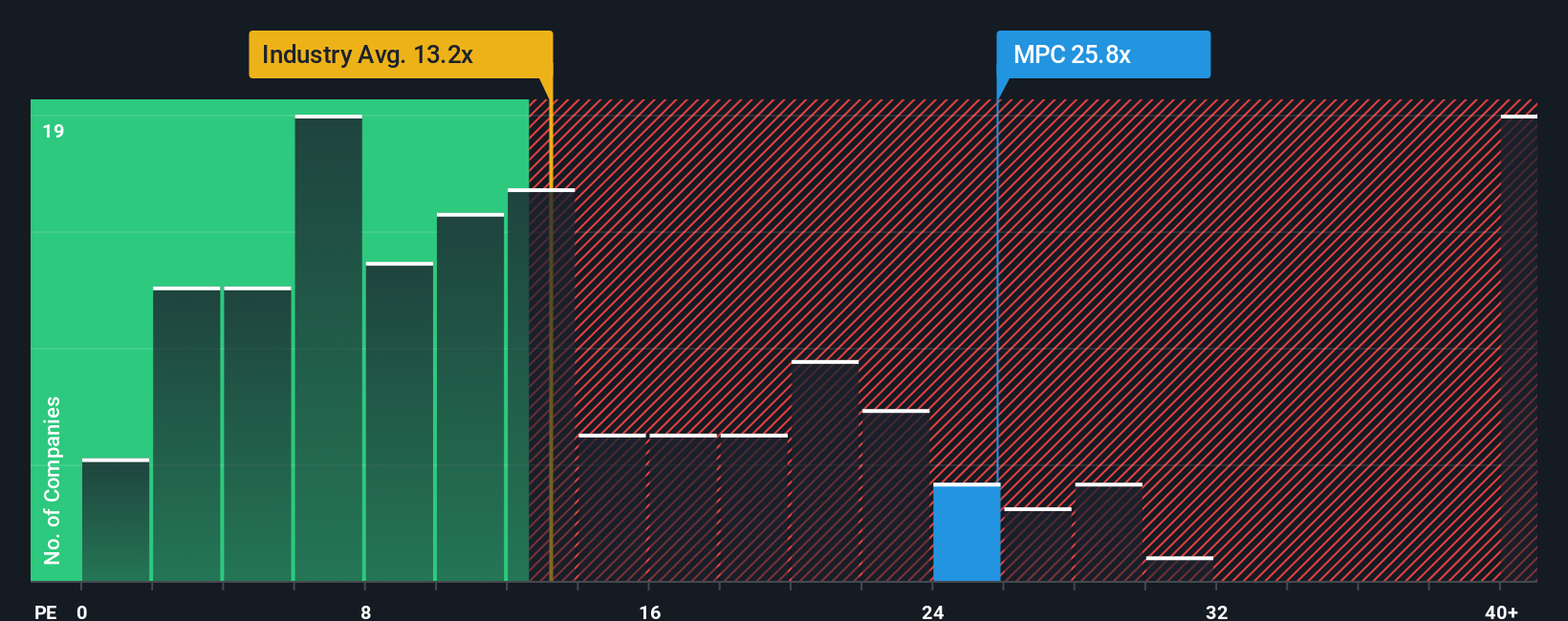

Looking at valuation through the lens of price-to-earnings, Marathon Petroleum trades at 25.8 times earnings. This is noticeably higher than the US Oil and Gas industry average of 13.4 times and also above the market-implied fair ratio of 21.2. This points to potential overvaluation based on earnings multiples. Could this premium signal risk if sentiment shifts?

See what the numbers say about this price — find out in our valuation breakdown.

NYSE:MPC PE Ratio as at Oct 2025 Build Your Own Marathon Petroleum Narrative

NYSE:MPC PE Ratio as at Oct 2025 Build Your Own Marathon Petroleum Narrative

For those who like to dig into the details firsthand or take a different perspective, you can craft your own view in just a few minutes using Do it your way.

A great starting point for your Marathon Petroleum research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Ready for More Smart Investment Moves?

If you want to spot unique opportunities you might otherwise miss, let Simply Wall Street’s powerful screener uncover stocks aligning with your strategy and goals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com