In recent weeks, European markets have experienced a downturn, with the pan-European STOXX Europe 600 Index declining by 1.10% amid profit-taking and geopolitical tensions. As investors navigate these choppy waters, identifying small-cap stocks that may be undervalued can present opportunities for those looking to capitalize on market inefficiencies. A good stock in this context is one that demonstrates strong fundamentals and potential for growth despite broader economic challenges.

Top 10 Undervalued Small Caps With Insider Buying In EuropeNamePEPSDiscount to Fair ValueValue RatingBytes Technology Group16.7×4.1×26.13%★★★★★☆Speedy HireNA0.3×27.21%★★★★★☆Cairn Homes12.5×1.6×28.92%★★★★★☆BEWINA0.4×40.87%★★★★★☆Fastighets AB Trianon13.4×4.4x-204.88%★★★★☆☆Nyab21.5×0.9×37.16%★★★☆☆☆Oxford Instruments39.0x2.0x18.23%★★★☆☆☆Renold10.7×0.7x-0.16%★★★☆☆☆J D Wetherspoon10.2×0.3x-0.04%★★★☆☆☆Social Housing REITNA7.0x35.02%★★★☆☆☆

Let’s explore several standout options from the results in the screener.

Simply Wall St Value Rating: ★★★★☆☆

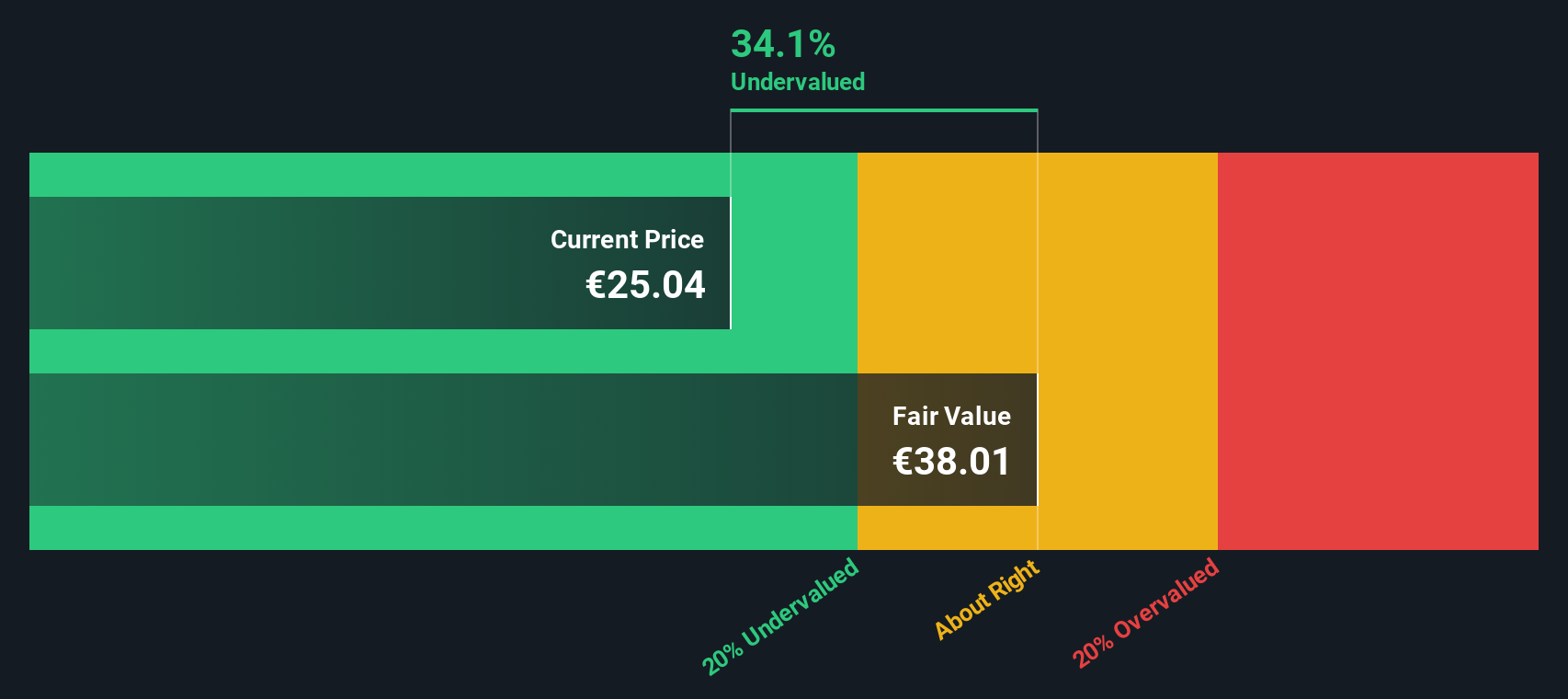

Overview: Basic-Fit operates a network of fitness clubs primarily across Benelux, France, Spain, and Germany with a market capitalization of €1.95 billion.

Operations: The company generates revenue primarily from its operations in Benelux and the combined regions of France, Spain, and Germany. Over recent periods, the gross profit margin has shown a trend around 79.96%. Operating expenses include significant contributions from depreciation and amortization, alongside sales and marketing efforts.

PE: -399.3x

Basic-Fit, a European fitness chain, has seen its share price fluctuate significantly over the past three months. Despite reporting a net loss of €7.9 million for H1 2025, compared to last year’s €4.2 million profit, they remain optimistic with revenue guidance between €1.375 billion and €1.425 billion for the full year 2025. Insider confidence is evident as insiders purchased shares from March to June 2025, totaling €10 million in buybacks. Earnings are projected to grow annually by 45.75%, indicating potential value despite current challenges with external borrowing risks.

Simply Wall St Value Rating: ★★★★☆☆

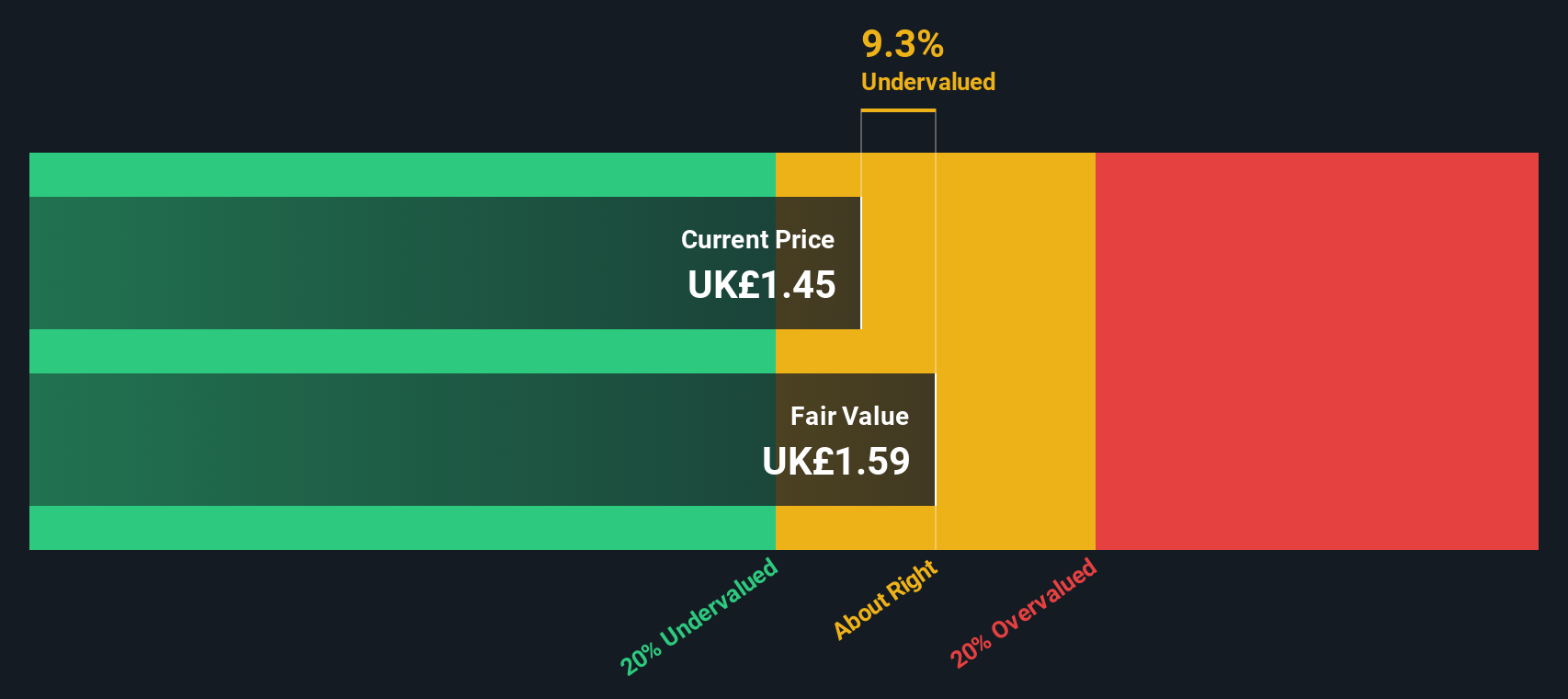

Overview: NCC Group is a global cyber security and risk mitigation company with operations focused on providing services such as escrow solutions and comprehensive cyber security offerings, with a market cap of approximately £0.58 billion.

Operations: Cyber Security generates the majority of revenue at £246.18 million, while Escode contributes £65.95 million. The gross profit margin has shown variability, peaking at 42.28% and dipping to 27.97%. Operating expenses have been a significant component, with general and administrative expenses being a notable portion of these costs across periods.

PE: -30.4x

NCC Group, a European cybersecurity firm, stands out in the small-cap sector with its potential for growth. Despite relying on external borrowing for funding, which carries higher risk than customer deposits, NCC is projected to see earnings grow by 61% annually. Insider confidence is evident as insiders have been purchasing shares consistently over the past year. This activity suggests belief in the company’s future prospects and potential value within its industry context.

Simply Wall St Value Rating: ★★★★★☆

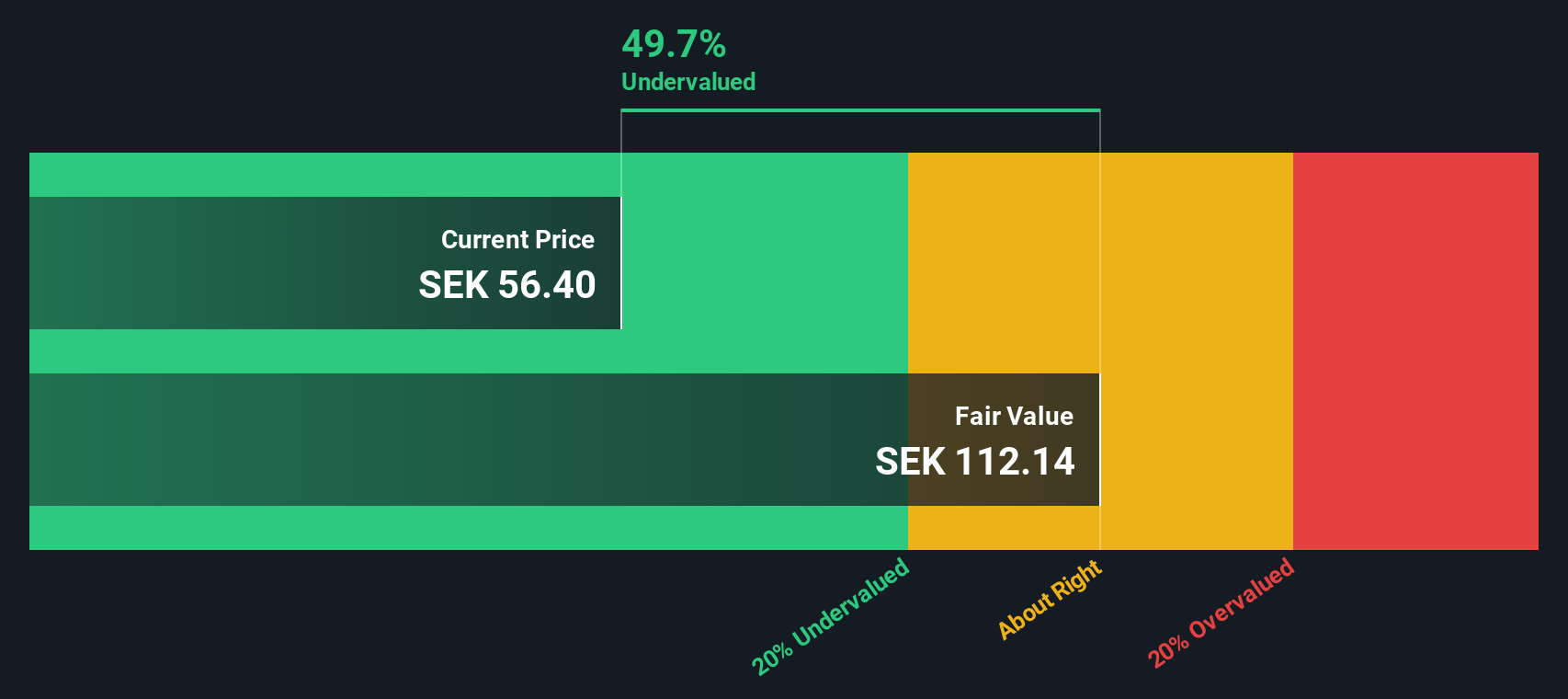

Overview: Svedbergs Group operates in the bathroom furniture and fixtures industry, encompassing brands like Cassoe, Thebalux, Sved-Bergs, Macro Design, and Roper Rhodes, with a market capitalization of approximately SEK 1.91 billion.

Operations: Svedbergs Group’s primary revenue streams are derived from its segments, with Roper Rhodes contributing the most at SEK 1.17 billion, followed by Thebalux and Sved-Bergs. The company’s gross profit margin has shown a notable increase, reaching 46.70% in recent periods. Operating expenses are primarily driven by sales and marketing activities, which represent a significant portion of costs alongside general and administrative expenses.

PE: 16.5x

Svedbergs Group’s recent earnings report shows promising growth, with second-quarter sales climbing to SEK 570.5 million and net income rising to SEK 51.3 million from the previous year. The company’s basic earnings per share increased to SEK 0.97, reflecting solid operational performance. Insider confidence is evident as they purchased shares in early 2025, suggesting belief in future prospects despite reliance on higher-risk external borrowing for funding needs. Earnings are projected to grow annually by 13.59%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Discover if Basic-Fit might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com