IMF/WB annual meetings are rarely a market catalyst, but every once in a while they are. The last time this happened – prior to last week – was in October 2023, when the 10-year Treasury yield had risen towards 5 percent into the meetings and no one could figure out why. Every meeting began with the same question: “Why is 10-year going up so much?” The collective wisdom from those meetings was that the rise made no sense. The 10-year yield peaked soon after and has not gone back up to 5 percent ever since.

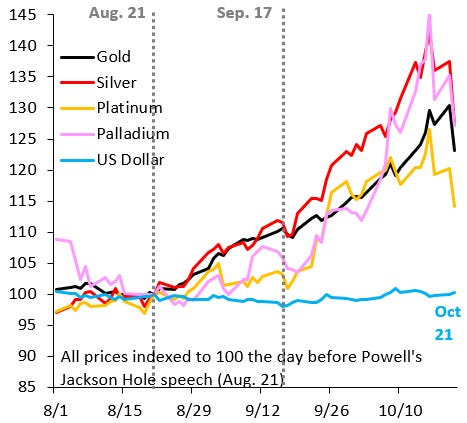

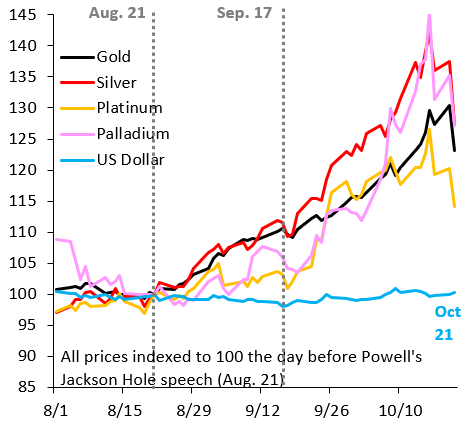

The set-up was very similar into last week’s IMF/WB meetings. Precious metals had been staging an incredible – and unfathomable – rally into the meetings and there was no explanation for what was going on. Once again, the meetings – with lots of face-to-face conversations – proved to be a turning point for markets, something I flagged in a post over the weekend. As the chart below shows, precious metals prices are tumbling this week. This particular bubble is bursting.

Two things are important to understand. First, in my opinion, the fall in precious metals prices is intricately linked to lots of foreign visitors – especially from Europe – upgrading their US growth view after getting bombarded with chatter on AI capital investment and productivity growth. US “exceptionalism” is making a comeback and may translate into a more bullish outlook for the Dollar. Second, the unwind of the precious metals bubble does not mean that the “debasement trade” is over. That trade is about markets trying to get ahead of what they see as inevitable monetization of debt overhangs across many advanced economies. The recent precious metals bubble is just one particular manifestation of that trade. Others are rising long-term yields on government debt and stronger currencies for countries with low debt. The debasement trade will be with us for many years and – since it’s fear-based – bubbles like the precious metals spike of recent weeks are inevitable.