Europe Digital Oilfield Market Size

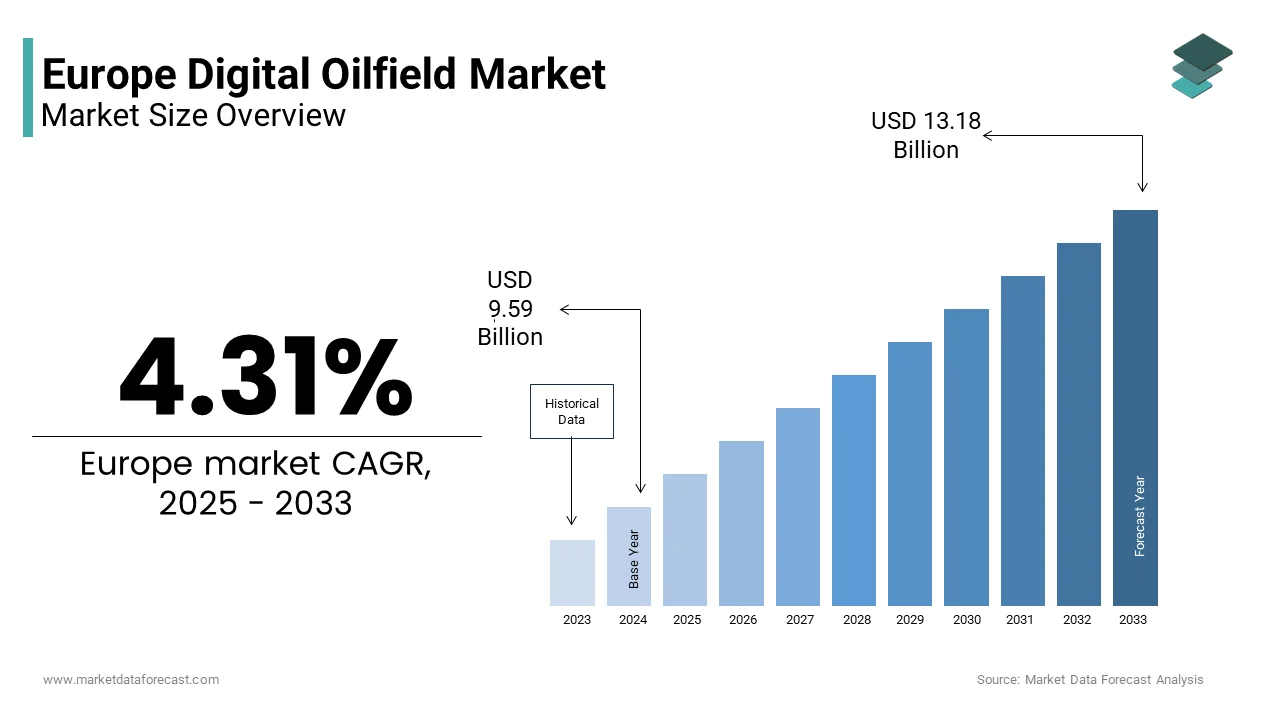

The Europe digital oilfield market size was valued at USD 9.19 billion in 2024 and is anticipated to reach USD 9.59 billion in 2025 to USD 13.18 billion by 2033, growing at a CAGR of 4.31% during the forecast period from 2025 to 2033.

The digital oilfield is the integration of advanced technologies such as artificial intelligence, the industrial Internet of Things, real-time data analytics, and automated control systems into upstream oil and gas operations to enhance reservoir recovery, optimize production, and reduce operational emissions. The European Commission’s Energy Technology Observatory identifies digital oilfield solutions as key enablers of “brownfield revitalization” in aging infrastructure where physical upgrades are cost-prohibitive.

MARKET DRIVERS Regulatory Pressure to Reduce Methane Emissions and Flaring

The stringent EU environmental regulations are compelling operators to adopt digital oilfield technologies to monitor and curtail methane leaks and routine flaring, which is fuelling the growth of Europe’s digital oilfield market. The EU Methane Regulation, enacted in 20,23, mandates quarterly leak detection and repair using advanced optical gas imaging or continuous monitoring systems for all facilities producing over 10000 barrels of oil equivalent per day. Equinor and Wintershall Dea have already deployed satellite-based methane detection platforms combined with AI-powered anomaly alerts across their Norwegian and German assets. These compliance imperatives are accelerating investments in sensor networks, edge computing, and cloud-based analytics to ensure continuous environmental accountability.

Aging Infrastructure and Declining Reservoir Productivity

The oil and gas fields are among the world’s oldest, with average operational ages exceeding 35 years, driving urgent adoption of digital oilfield solutions to sustain output, which is levelling up the growth Europe’sope digital oilfield market. In response, Aker BP and Equinor have implemented integrated operations centers that fuse seismic data, downhole pressure readings, and multiphase flow meter outputs to dynamically adjust well parameters and identify bypassed oil zones. Similarly, Romania’s OMV Petrom has digitized over 200 onshore wells using wireless sensor networks that reduce manual inspection frequency by 60% while improving uptime. The European Network of Transmission System Operators for Gas reports that digital twin models are now standard in field redevelopment plans approved under the EU’s Innovation Fund. This technological retrofitting of legacy assets is essential to maintain Europe’s domestic hydrocarbon supply amid declining investment and geopolitical uncertainty.

MARKET RESTRAINTS Limited Capital Expenditure Allocation for Digital Transformation

Many European oil and gas operators remain constrained in funding comprehensive digital oilfield rollouts due to capital discipline and energy transition priorities. This is restricting the growth of the Europe digital oilfield market. According to the European Central Bank’s 2023 Sectoral Investment Survey, only 14% of upstream oil and gas firms in the EU allocated more than 10% of their capital expenditure to digital initiatives, a decline from 22% in 2021. As per the International Energy Agency, total upstream investment in Europe fell to 18.4 billion US dollars in 202,3, with over 65% directed toward maintenance and compliance rather than innovation. Smaller independent operators, which manage 43% of Europe’s producing wells as per the European Association of Independent Oil and Gas Producers, often lack the scale to justify multi-million euro digital platform deployments. Additionally, the European Investment Bank reports that green financing mechanisms such as the Innovation Fund exclude pure efficiency upgrades unless tied to verified emission reduction,,s creating a misalignment between digitalization benefits and funding eligibility. This financial conservatism delays the adoption of integrated operations and predictive analytics, particularly in onshore fields in Hungary, Poland, and IItalywhere margins are thinnest.

Fragmented Data Standards and Legacy System Incompatibility

The significant technical barriers due to heterogeneous legacy control systems and the absence of unified data protocols across operators and basins are limiting the growth of the Europe digital oilfield market. As per the European Energy Research Alliance, interoperability gaps between vendor-specific software from Schlumberger,,r Halliburton,n and Baker Hughes prevent seamless data aggregation even within single operator portfolios. Furthermore, the European Standardization Committee has yet to ratify a continent-wide ontology for upstream data despite ongoing work under the Energistics consortium. This fragmentation increases integration costs, extends deployment timelines,e, and undermines the reliability of AI-driven insights.

MARKET OPPORTUNITIES Integration of Digital Twins for Brownfield Asset Optimization

The deployment of high-fidelity digital twins to extend the life and improve the economics of mature fields is anticipated to bolster the growth of the Europe digital oilfield market. As per DNV Norway’s Aker BP has achieved a 15% increase in recovery factor on the Valhall field by continuously calibrating its digital twin with real-time downhole and surface data. Similarly, TotalEnergies implemented a cloud-based twin for its onshore Lacq field in France, reducing unplanned downtime by 28% through vibration and temperature anomaly prediction. The European Network of Transmission System Operators for Gas notes that digital twins are now required in all field abandonment delay requests submitted to national regulators. Moreover, the Joint Research Centre estimates that widespread twin adoption across EU brownfields could unlock an additional 420 million barrels of recoverable oil by 2035.

Expansion of Remote Operations Centers Enabled by 5G and Edge Computing

The rollout of industrial 5G and edge computing infrastructure is enabling centralized remote operations centers that enhance safety and reduce offshore staffing costs, which is attributed to the growth of Europe’s digital oilfield market. According to the European Telecommunications Standards Institute, over 28 offshore platforms in the North Sea and Norwegian Sea were connected to private 5G networks by the end of 202,3, providing sub-10-millisecond latency for real-time control of subsea valves and pumps. As per the Norwegian Ministry of Petroleum and Energy, Equinor’s remote operations center in Stavanger now supervises 90% of its offshore production, ion withon-platformm personnel reduced by 35% since 2021.

MARKET CHALLENGES Cybersecurity Vulnerabilities in Connected Field Infrastructure

The increasing digitization of Europe’s oilfields has expanded the attack surface for cyber threats targeting critical operational technology systems is degrading the growth of Europe’s digital oilfield market. According to the European Union Agency for Cybersecurity, some oil and gas operators in the EU reported attempted breaches of industrial control systems in 202,3, with 12 incidents resulting in temporary production disruption. As per the Norwegian National Security Authority, a 2023 ransomware attack on a North Sea service provider temporarily disabled real-time pressure monitoring on three platforms requiring manual overrides. The European Commission’s NIS2 Directive mandates stricter security measures for energy operators, but many legacy SCADA systems lack encryption and multi-factor authentication,n making compliance costly. Furthermore, the European Defence Agency warns that state-sponsored actors are increasingly probing digital oilfield networks for strategic disruption potential, particularly in the Baltic and Black Sea regions.

Workforce Skills Gap in Data Science and Digital Operations

The transition to digital oilfields is hindered by a shortage of personnel skilled in data analytics, machine learning, and integrated operations is also slowly degrading the growth of Europe’s digital oilfield market. According to the European Centre for the Development of Vocational Training, only oil and gas engineers in the EU have formal training in data science or AI applications as of 2023. Furthermore, the European Commission’s Pact for Skills has yet to include upstream digital competencies in its energy workforce roadmap despite commitments to a just transition. This human capital deficit slows the realization of value from digital investments and increases reliance on vendor lock-in.

REPORT COVERAGE

REPORT METRIC

DETAILS

Market Size Available

2024 to 2033

Base Year

2024

Forecast Period

2025 to 2033

CAGR

4.31%

Segments Covered

By Process, Solution, Application, And Region

Various Analyses Covered

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

Regions Covered

UK, France, Spain, Germany, Italy, Russia, Sweden

Market Leaders Profiled

Slb (U.S.), Halliburton (U.S.), Weatherford (U.S.), Siemens (Germany), Osprey Informatics (Canada), IBM (U.S.), Digi International (U.S.), Microsoft (U.S.), Baker Hughes (U.S.), Kongsberg Digital (Norway), Rockwell Automation (U.S.), Accenture (Ireland), Honeywell Process Solutions (U.S.), ABB (Switzerland), Emerson (U.S.), National Oilwell Varco (U.S.)

SEGMENTAL ANALYSIS By Process Insights

The production optimization segment held 41.3% of the Europe digital oilfield market share in 202,4, with the urgent need to maximize output from aging assets with declining well performance. Equinor’s implementation n AI-powered red choke valve automation on the Troll platform increased daily output by 1800 barrels without additional drilling. Similarly, Wintershall Dea integrated vibration and temperature sensors on rod pumps in its German onshore fields, cutting maintenance costs by 31%. The European Commission’s Innovation Fund has approved 14 production optimization projects since 2022 that combine edge computing with reservoir data to enable closed-loop control. This focus on near-term yield enhancement from existing infrastructure ensures production optimization remains the largest process segment.

The reservoir optimization segment is inclined to grow the fastest CAGR of 12.8% from 2025 to 20,3, with the need to improve recovery factors in Europe’s highly depleted basins, where conventional modeling fails to capture complex geology. According to the European Association of Geoscientists and Engineers, digital rock physics and 4D seismic inversion now enable dynamic reservoir simulation with weekly update cycles instead of annual static models. In Romania, OMV Petrom deployed machine learning algorithms to reinterpret legacy seismic data, identifying 3.2 million barrels of bypassed oil in the Neptun Deep area. Furthermore, the European Commission mandates that all field redevelopment plans submitted under the Hydrogen and Decarbonization Fund include reservoir optimization components to justify extended production licenses.

By Solution Insights

The services segment accounted in holding 48.3% of the Europe digital oilfield market share in 2024 o,, owing to the complexity of deploying and maintaining integrated digital systems across heterogeneous field environments. As per the International Association of Oil and Gas Producers, digital transformation projects in Europe average 14 months in duration, with 60% of the budget allocated to consulting deployment and training services. Schlumberger and Halliburton have established dedicated digital delivery centers in Aberdeen and Hamburg to support real-time operations for North Sea clients. The European Defence Agency also notes that national security concerns over critical infrastructure have increased demand for EU-based cybersecurity audit and incident response services.

The software segment is likely to grow at an anticipated CAGR of 14.2% from 2025 to 203,3 with the cloud migration,n subscription licensing,d h and rise of modular SaaS platforms that democratize access for smaller operators. As per Equinor, its cloud-based Field Development Planning suite reduced scenario modeling time from weeks to hours, enabling faster investment decisions. In Germany, Wintershall Dea adopted a pay-per-well software model from aMa unich-basedd startup to monitor 120 onshore assets without upfront capital costs. Furthermore, the NIS2 Directive requires auditable software logs for all safety-critical systems, driving demand for compliant digital workflows.

By Application Insights

The offshore operations segment held a significant share of the Europe digital oilfield market in 2024 due to the high cost complexity and safety risks associated with North Sea and Norwegian Continental Shelf assets. As per the Norwegian Ministry of Petroleum and Energy, 92% of offshore fields now use integrated operations centers that fuse real-time downhole data, a subsea control system,,s and weather forecasting to enable remote decision making. Additionally, offshore fields generate 10 to 15 times more sensor data per well than their onshore counterparts, necessitating advanced analytics infrastructure.

The onshore segment is emerging swiftly at a fastest CAGR of 11.5% from 2025 to 2033 with the digitization of mature low margin fields inGermanyt Romaniay,, where manual monitoring is no longer economically viable. Over 1200 onshore wells in the EU are operated by small companies with fewer than 50 employees who are now adopting low-cost wireless sensor networks and mobile dashboards. The OMV Petrom’s digital retrofit of 210 onshore wells in 2023 cut inspection visits by 65%, while improving gas lift efficiency.

COUNTRY ANALYSIS United Kingdom Digital Oilfield Market Analysis

The United Kingdom digital oilfield market held 22.3% of the share in 2024 with its mature North Sea assets and robust digital infrastructure. Companies like BP and Harbour Energy operate remote centers in Aberdeen that monitor subsea wells using fiber optic sensing and cloud analytics. The UK’s North Sea Transition Authority requires digital methane monitoring on all facilities producing over 5000 barrels per day as part of its Methane Action Plan. Additionally, the Offshore Energies UK association reports that digital twin adoption saved 420 million pounds in operational costs in 2023.

Germany Digital Oilfield Market Analysis

Germany was ranked next with 14.3% of the Europe digital oilfield market share in 2024, with its extensive onshore oil and gas fields primarily in Lower Saxony. According to the Federal Institute for Geosciences and Natural Resources, Germany operates over 1800 onshore we, many over 40 years old, which are now being retrofitted witwith low-powerT sensors and predictive maintenance software. Wintershall Dea’s digital pilot in Barnstorf reduced rod pump failures by 38% in 2023 using vibration analytics. Furthermore, the Fraunhofer Institute for Energy Economics has developed open-source reservoir simulation tools funded by the Ministry for Economic Affairs to support independent operators.

Italy’s digital oilfield market growth is likely to grow with the digitization of small onshore fields in Emilia Romagna and emerging offshore monitoring in the Adriatic Sea. The company also uses satellite-based methane detection over its Val d’Agri field to comply with EU regulations. Furthermore, Eni’s Green Data Center in Milan processes 12 terabytes of field data daily for predictive analytics. Italy’s strategy combines regulatory compliance, operational efficiency, and green computing to sustain marginal fields in a decarbonizing energy landscape.

COMPETITIVE LANDSCAPE

Competition in the Europe digital oilfield market is characterized by a mix of global oilfield service giants, European energy majors, and agile tech startups vying to deliver integrated digital solutions under tightening regulatory and economic constraints. While Schlumberge, Halliburton,,n and Baker Hughes dominate through comprehensive platforms and long-standing operator relationships, niche European firms are gaining traction by offering specialized tools for methdetectioctio,,n legacy system interoperability, ty and SME affordability. The market is not driven by price but by compliance capability, deployment speed, and demonstrable efficiency gains in mature fields. Energy majors like Equin, TotalEnergies, and Eni also exert influence by developing proprietary digital systems and selectively licensing them to partners. Regulatory alignment with the EU Methane Regulation, NIS2 Directive, and Innovation Fund criteria has become a key differentiator. Fragmentation persists due to basin-specific challenges and operator size diversity y,, et consolidation is emerging through strategic alliances. Ultimately s success hinges on balancing technological sophistication with pragmatic implementation in Europe’s complex and decarbonizing upstream landscape.

KEY MARKET PLAYERS

A few of the market players in the Europe digital outfield market include

Slb (U.S.) Halliburton (U.S.) Schlumberger Weatherford (U.S.) Baker Hughes Siemens (Germany) Osprey Informatics (Canada) IBM (U.S.) Digi International (U.S.) Microsoft (U.S.) Baker Hughes (U.S.) Kongsberg Digital (Norway) Rockwell Automation (U.S.) Accenture (Ireland) Honeywell Process Solutions (U.S.) ABB (Switzerland) Emerson (U.S.) National Oilwell Varco (U.S.) Top Players In The Market Schlumberger is a global technology leader in digital oilfield solutions with deep integration across Europe’s upstream sector, particularly in the North Sea and Norwegian Continental Shelf. The company provides its DELFI cognitive E&P environment to major operators, or data-driven decision making across exploration,,n production, and reservoir management. In 2023, Schlumberger expanded its digital delivery center in Aberdeen to support real-time remote operations for UK and Norwegian clients. It also launched a cloud-based methane monitoring module compliant with the EU Methane Regulation, integrating satellite and ground sensor data. Through strategic partnerships with Equinor and TotalEnergies, Schlumberger has embedded its AI-powered production optimization tools into daily workflows. These initiatives reinforce its position as a trusted enabler of Europe’s digital energy transition and regulatory compliance. Halliburton plays a pivotal role in the Europe digital oilfield market through its DecisionSpace 365 cloud platform and automated drilling solutions deployed across onshore and offshore assets. The company supports operators in Germany, Romania, and the UK with integrated data lakes that unify legacy seismic maintenance records. In early 2024, Halliburton opened a dedicated cybersecurity operations hub in Hamburg to address NIS2 Directive requirements for critical energy infrastructure. It also enhanced its iCruise intelligent rotary steerable system with edge analytics to reduce drilling time in complex Central European geologies. Baker Hughes is a key contributor to Europe’s digital oilfield transformation through its BHC3 AI suite and equipment health monitoring systems deployed from the North Sea to the Black Sea. The company collaborates with Aker BP, Equino,,r and Eni to deliver predictive maintenance and autonomous well control solutions that reduce downtime and emissions. In 2023, Baker Hughes launched a modular digital twin service tailored for small and mid-sized operators in Germany and Italy, enabling affordable access to reservoir simulation and production forecasting. It also integrated real-time methane detection into its compression and pumping systems to support compliance with the EU Methane Regulation. These targeted innovations position Baker Hughes as a critical partner in Europe’s push for efficient, sustainable hydrocarbon operations. Top Strategies Used By The Key Market Participants

Key players in the Europe digital oilfield market are prioritizing cloud native software platforms that enable scalable data integration across legacy and modern field systems. Companies are embedding artificial intelligence and machine learning into production and drilling workflows to deliver predictive insights and autonomous control. Strategic investments in remote operations centers and G-enabled edge computing infrastructure support staffing reduction and real-time decision-making, particularly offshore. Partnerships with national regulators and operators ensure compliance with EU mandates on methane monitoring, cybersecurity emissions reporting. Cybersecurity by design is being integrated into all digital solutions to meestringenthstringent NISDirectiveve requirements.

MARKET SEGMENTATION

This research report on the Europe digital outfield market is segmented and sub-segmented into the following categories.

By Process

Production Optimization Reservoir Optimization Drilling Optimization Others

By Solution

Services Software Hardware

By Application

By Country

UK France Spain Germany Italy Russia Sweden Denmark Switzerland Netherlands Turkey Czech Republic Rest of Europe