Berkshire Hathaway’s sizable purchase of over 4 million shares in Chubb (CB) during the third quarter is turning heads. The move comes immediately after Chubb posted record underwriting income and another strong quarterly earnings beat.

See our latest analysis for Chubb.

Chubb’s share price momentum has quietly accelerated, with a 10% jump in the last month fueling its longer-term climb. While headline events like Berkshire Hathaway’s sizable stake and Chubb’s record underwriting performance have caught Wall Street’s attention, recent executive moves and the launch of a new AI-powered platform show the company is not standing still. Overall, steady performance and a one-year total shareholder return of 3.7% underscore Chubb’s blend of stability and growth potential, even as some institutional investors recalibrate their holdings.

If the current flurry of innovation and leadership change has you rethinking your approach, now is an ideal time to discover fast growing stocks with high insider ownership

With all this momentum and attention, the key question is whether Chubb’s recent rally means the stock is undervalued, or if the market has already priced in its future growth, leaving little room for upside.

Most Popular Narrative: 3.9% Undervalued

Although Chubb’s share price closed at $295.49, the most widely followed narrative puts its fair value higher, setting the stage for potential upside. The market appears to be pricing in cautious optimism, with near-term results and long-term strategies under a close watch.

Capital deployment through ongoing share repurchases (new $5B authorization), growing dividends, and selective M&A is creating upward pressure on earnings per share (EPS). At the same time, robust cash flow and a strong capital position provide flexibility for further shareholder returns.

Curious which financial levers this narrative is banking on? Behind this valuation is a hidden mix of buybacks, margin boosts, and bold profit targets. Want the full story powering Chubb’s outlook? The key details will surprise you.

Result: Fair Value of $307.50 (UNDERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, rising competition in core insurance lines and increasing claims expenses due to litigation and natural disasters could quickly challenge Chubb’s current momentum.

Find out about the key risks to this Chubb narrative.

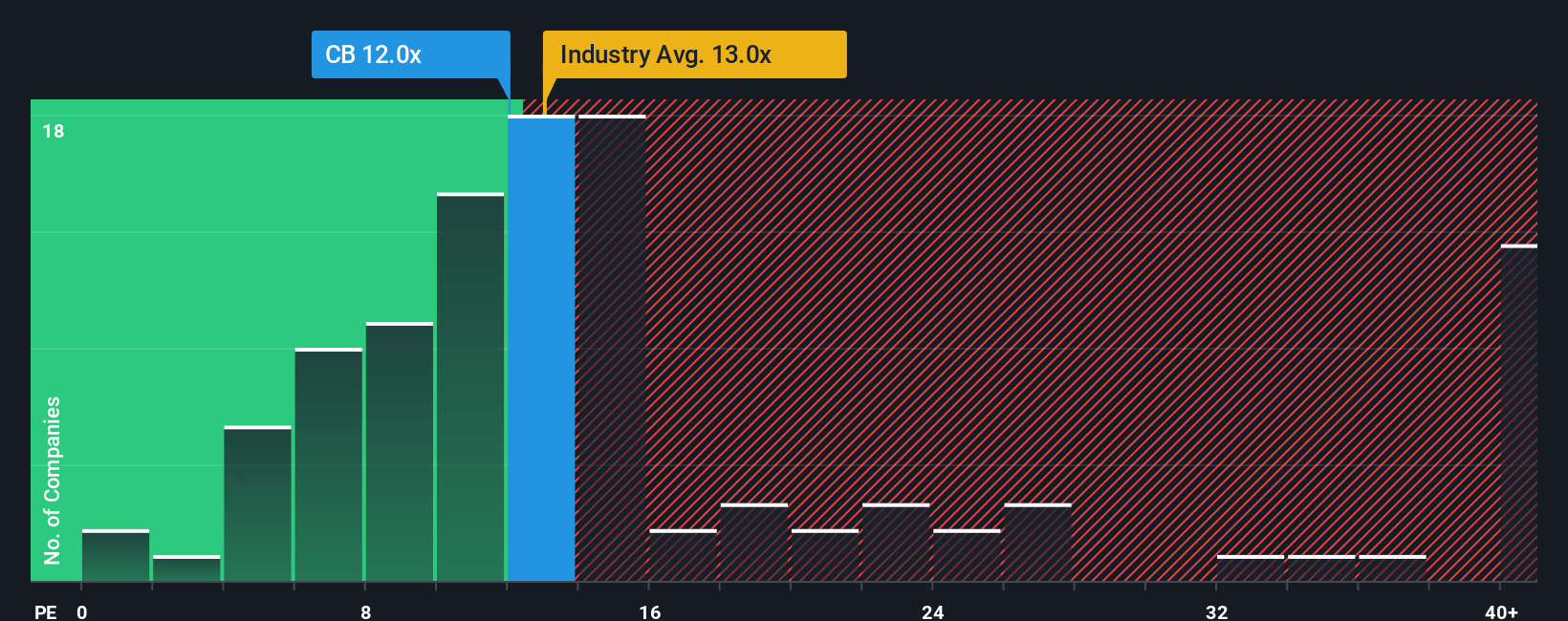

Another View: What Does the Earnings Multiple Tell Us?

Looking at Chubb through the lens of earnings multiples, its current price-to-earnings ratio of 12x looks attractive compared to the US Insurance industry average of 13x and stands above its peer average of 10.2x. Notably, this is still below its estimated fair ratio of 13.5x. This gap suggests investors may be underestimating the company’s true value, but it also raises questions around valuation risk as markets shift.

See what the numbers say about this price — find out in our valuation breakdown.

NYSE:CB PE Ratio as at Nov 2025 Build Your Own Chubb Narrative

NYSE:CB PE Ratio as at Nov 2025 Build Your Own Chubb Narrative

If you want a different perspective or trust your own research process, you can easily build a unique Chubb story in just a few minutes. So why not Do it your way?

A great starting point for your Chubb research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Investment Ideas?

Don’t let market opportunities pass you by. The right screener can help you uncover stocks that align with your goals and give you a powerful investing edge.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com