Global gas markets are shifting tone as the first signs of winter emerge across the northern hemisphere. Europe enters the season with storage near record levels, the United States experiences renewed volatility in Henry Hub prices, and Asian LNG premiums widen as colder weather forecasts intersect with logistical bottlenecks. What looked like a comfortable balance only weeks ago is beginning to show the familiar signs of seasonal strain.

Natural Gas is not repeating the dramatic pattern of late-2022, but it is clearly exiting the low volatility phase that defined much of the past three months. Weather uncertainty, shipping delays and the sensitive structure of the LNG value chain are combining to lift risk premia across key benchmarks. The movement is controlled rather than explosive, yet meaningful enough for traders to reassess positioning.

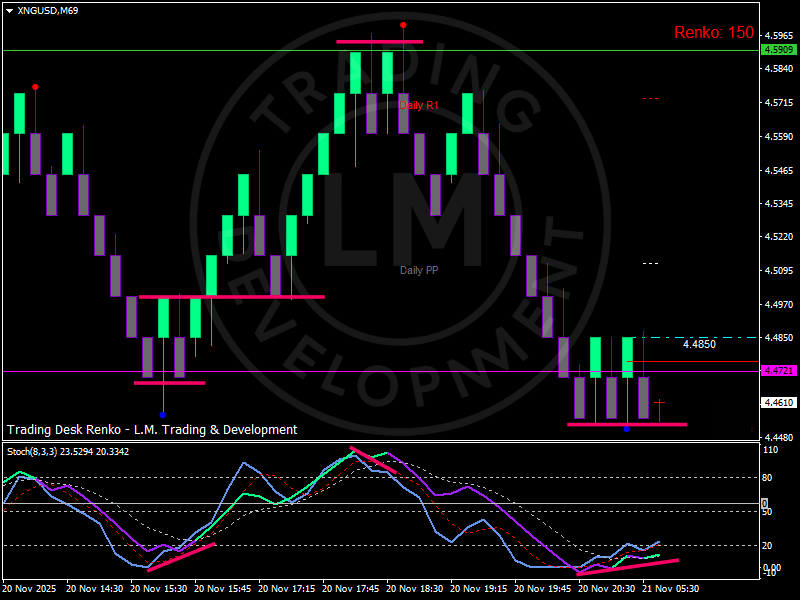

The Renko structure of XNGUSD reflects this shift with surprising clarity. After rejecting the 4.59 dollars zone, price has moved into a tight consolidation around 4.48 dollars, while momentum indicators approach a potential inflection from oversold conditions. This pattern aligns with the broader fundamental narrative. The market is not short of gas, but the buffer is fragile and the system is entering its seasonal window of stress.

Europe’s storage comfort hides logistical and weather risks

European gas inventories remain historically high for this time of year. Front month TTF eased through most of October and early November as mild temperatures prolonged the injection season and LNG arrivals remained steady. At first glance, this would suggest a balanced winter scenario.

Yet two factors are beginning to challenge that perception.

The first is weather. Forecast models for late November and early December indicate a colder shift across central and northern Europe. Even moderate cold spells can erase parts of the storage advantage, especially when heating demand accelerates from a low base. Storage is a buffer, not a guarantee. Market participants have responded by adding optionality, widening the near term risk premium.

The second factor is logistics. Several LNG cargoes headed to Europe have experienced delays linked to congestion at key maritime routes and weather disruptions affecting loading schedules. The delays are not severe, but they highlight the structural vulnerability of a system that relies heavily on timely cargo rotation. A few days’ disruption can affect prompt pricing in a market sensitive to weather driven demand spikes.

Combined, these dynamics explain why TTF has begun to trade with more volatility despite high storage levels.

United States supply is strong but Henry Hub is becoming more reactive

On the supply side, the United States remains the backbone of LNG exports. Production is robust, and pipeline flows into liquefaction facilities remain near capacity. However, Henry Hub prices have shown renewed volatility. This is partly linked to early winter weather patterns and partly to the behaviour of the forward curve.

The front of the curve is tightening, while the back end remains more muted. This flattening carries two messages. First, traders expect short term stress linked to weather and LNG maintenance flows. Second, the broader outlook for Spring 2026 remains stable, suggesting that structural supply is more than adequate.

This alignment between strong structural supply and short term seasonal tension is a hallmark of mature gas markets, and it is exactly what is appearing in the price action.

Asia’s premium widens as winter competition re-emerges

Asian buyers have reappeared on the spot market after a period of reduced activity. The JKM premium over European benchmarks has widened, reflecting both winter demand and improved procurement activity in Japan and South Korea.

China’s demand remains variable, affected by industrial output cycles, but utilities continue to secure winter supply to avoid the tight conditions experienced in previous years. The competition between Atlantic and Pacific basins is not severe, but it is enough to shift marginal cargo flows and contribute to upward pressure on prompt prices.

This widening Asia Europe spread is one of the clearest signs that the global LNG system is transitioning into its seasonal stress phase.

The Renko structure confirms the building tension

The technical picture on Natural Gas aligns smoothly with this macro backdrop.

The Renko chart of XNGUSD shows a decisive rejection near 4.59 dollars, a level that coincides with previous supply clusters and aligns with daily resistance. From there, price has retraced into a tight consolidation band around 4.48 dollars, with recurring brick reactions near the lower boundary.

Renko chart of XNGUSD highlighting the early winter consolidation around 4.48 dollars as global LNG markets enter a new seasonal stress window.

The oscillator reveals a subtle but visible momentum divergence, showing that sellers are losing marginal strength even as price tests the base of the structure. This type of divergence in a seasonal context often anticipates a short term bounce or a period of rotational volatility.

Importantly, price remains above the 4.46 dollars floor, a zone that has acted as support on multiple Renko sequences. Holding above this area preserves the possibility of renewed upward rotation if weather risks intensify or if LNG delays increase.

For short term traders, the range between 4.46 and 4.59 dollars becomes the key tactical zone. A break above 4.59 dollars would indicate that the market is pricing in more aggressive winter stress. A break below 4.46 dollars would suggest a reduction in weather risk or smoother LNG flows.

At this stage, neither extreme has been validated. The structure remains balanced but tense.

Why winter 2025–2026 is different from previous years

The current situation does not replicate the extreme conditions of 2022 or the rapid repricing events of early 2023. Stated differently, the market is not reacting to systemic shortages. It is reacting to the intersection of seasonal uncertainty and logistical sensitivity.

Several structural features differentiate the current winter from past cycles.

First, storage capacity is larger and better distributed across Europe. This reduces the probability of sudden dislocations but does not eliminate short term price risk.

Second, LNG infrastructure has expanded. The number of floating regasification units deployed in Europe has increased, enhancing flexibility.

Third, global supply chains have not yet regained full reliability. Maritime congestion and weather disruptions continue to create noise, and this noise becomes relevant in winter.

Fourth, investor positioning in the gas complex is lighter than in previous cycles. This means that when volatility appears, it tends to produce more reactive flows.

Together, these elements create a winter environment characterized by controlled risk rather than systemic fragility.

Outlook: A winter shaped by weather and logistics rather than structural scarcity

Looking ahead, Natural Gas is likely to navigate a tight band of winter volatility rather than a breakout trend. Prices will respond to temperature forecasts, LNG cargo timing and the behaviour of the Atlantic Pacific spread.

If Europe experiences sustained cold periods, TTF could lift materially even with high storage levels. If LNG delays accumulate, prompt prices will respond quickly. If Asia intensifies buying, the basin competition will tighten global flows.

On the other hand, if weather remains mild and logistical issues ease, the market may continue to trade inside a contained range, allowing the current consolidation to extend into December.

Traders should pay attention to the 4.46 dollars support and the 4.59 dollars resistance. These boundaries represent the technical translation of the market’s macro uncertainty.

Natural Gas is neither oversupplied nor scarce. It is entering a seasonal phase where both upside and downside require confirmation from physical fundamentals.

Conclusion

LNG and Natural Gas markets are entering the winter window with a mix of comfort and vulnerability. Storage is high, supply is strong and long term fundamentals remain stable. Yet weather risks, logistical pressure and regional competition introduce seasonal tension into the system.

The Renko structure captures this balance perfectly. Natural Gas trades inside a controlled consolidation, showing neither breakdown nor breakout, waiting for the next catalyst. Whether that catalyst comes from temperature shifts, shipping delays or Asian procurement will determine the winter trajectory.

For traders, the message is straightforward. Winter volatility is returning, but it is returning in a measured and structurally coherent way. Natural Gas is preparing for the seasonal test that defines every year, but this time the story is more about logistics and timing than structural scarcity.