Europe Ride Sharing Market Size

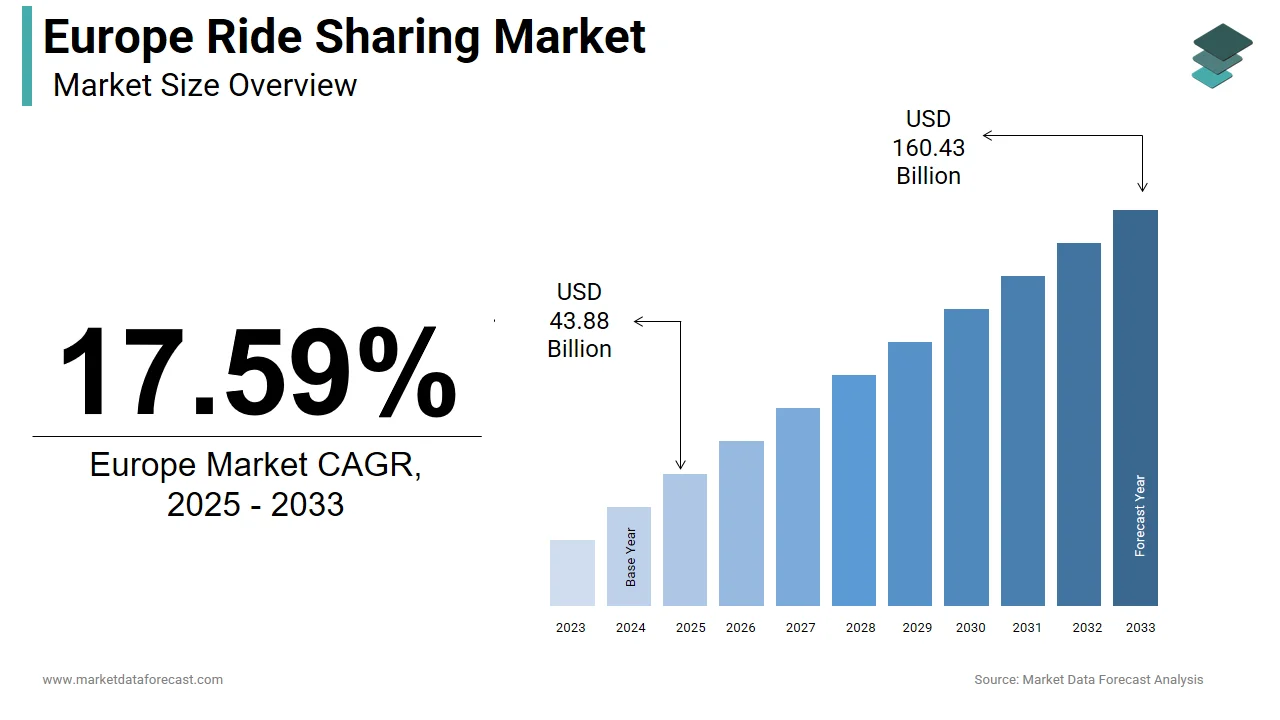

The size of the Europe ride-sharing market was worth USD 37.32 billion in 2024. The regional market is anticipated to grow at a CAGR of 17.59% from 2025 to 2033 and be worth USD 160.43 billion by 2033 from USD 43.88 billion in 2025.

Ride sharing refers to the technology-enabled on-demand transportation services that connect passengers with private drivers through digital platforms for point-to-point urban and interurban mobility. Unlike traditional taxi services ride ride-sharing operates under dynamic pricing models, algorithmic dispatch, and cashless transactions primarily via smartphone applications. Its growth is deeply intertwined with Europe’s evolving urban planning priorities, sustainability mandates, and shifting consumer attitudes toward vehicle ownership. According to sources, a significant majority of the European population lives in urban areas, where traffic congestion is a major problem. In response, cities like Paris, Berlin, and Amsterdam have implemented low-emission zones that restrict access for older combustion engine vehicles, prompting residents to seek cleaner alternatives. As per research, many cities are now offering integrated mobility-as-a-service (MaaS) platforms. These platforms bundle various transportation methods, such as ride-sharing, public transit, bike sharing, and other micro-mobility options, into a single service. Furthermore, there is a growing trend, particularly among younger adults, towards preferring access to transportation rather than personal ownership, reflecting a fundamental behavioral shift that underpins the structural relevance of ride sharing beyond mere convenience.

MARKET DRIVERS Urban Congestion and Declining Private Vehicle Ownership Among Youth

Persistent traffic congestion and a cultural shift away from car ownership among younger Europeans are propelling the growth of the Europe ride-sharing market. According to studies, the commuter in major European cities like Rome and London spends a significant number of hours annually stuck in traffic, which equates to nearly two full work weeks lost to idling. This inefficiency has accelerated the appeal of on-demand alternatives that optimize route planning and reduce the need for personal vehicles. Critically, vehicle ownership among Europeans under 30 has declined sharply. Ride sharing fills the mobility gap for non-owners, particularly for off-peak or last-mile trips where buses and trains are infrequent. This trend is not temporary but structural as urban density increases and younger generations prioritize experiential spending over asset accumulation, making ride sharing a default mobility layer in Europe’s multimodal ecosystem.

Integration with Public Transit and Mobility as a Service Platforms

Ride sharing is increasingly embedded within a broader Mobility as a Service framework that unifies public and private transport options into a single digital interface. This further boosts the expansion of the Europe ride-sharing market. In some cities, the app, which includes Bolt and local taxi services, reduced private car usage among subscribers. This integration addresses the critical “first and last mile” problem where public transit coverage is incomplete. National governments are actively supporting this synergy. Operating as a supportive service, ride-sharing improves the overall efficiency and scope of public transportation networks, thereby ensuring their governmental approval and continued use by people in many places.

MARKET RESTRAINTS Stringent National Regulations Classifying Drivers as Employees

Several European jurisdictions have enacted labor laws that reclassify ride-sharing drivers as employees rather than independent contractors, significantly increasing operational costs and limiting scalability, which in turn restrains the growth of the European ride-sharing market. The rulings stem from strong labor union advocacy and a continental emphasis on worker protections, but they fundamentally alter the asset-light model that underpins global ride-sharing economics. Companies must now bear fixed labor costs irrespective of demand fluctuations, making surge pricing and flexible supply unviable. This regulatory divergence creates compliance complexity and disincentivizes investment in markets where profitability is structurally constrained by social policy imperatives.

Local Opposition and Municipal Bans in Historic City Centers

Many European cities have imposed restrictions or outright bans on ride-sharing vehicles in historic or environmentally sensitive districts to preserve urban character and reduce traffic, which hinders the expansion of the Europe ride-sharing market. These measures reflect a broader tension between digital disruption and urban stewardship. Unlike North America, Europe’s compact medieval city layouts were never designed for high vehicle throughput, and local governments prioritize livability over convenience. Such caps not only constrain supply but also fragment service availability, creating geographic dead zones. The widespread adoption of zero-emission-only zones in response to tighter climate goals is expected to raise fleet transition costs and disadvantage smaller operators who cannot afford the capital investment required to electrify their fleets.

MARKET OPPORTUNITIES Electrification of Fleets and Green Mobility Partnerships

The transition to electric vehicles creates a major growth opportunity for the Europe ride-sharing market. This is because European cities enforce zero-emission mandates and consumers prioritize sustainability. Governments are accelerating this shift through incentives. These policies lower the total cost of ownership and enhance brand image. Moreover, corporate clients increasingly mandate green transportation for employee travel. Electrification thus transforms compliance into a competitive advantage, enabling platforms to access premium segments and public funding.

Expansion of Shared Ride and Pooling Models for Cost Efficiency

Shared ride or pooling services, where multiple passengers traveling in the same direction share a vehicle, offer a compelling solution to affordability and congestion challenges, which is setting fresh prospects for the expansion of the Europe ride-sharing market. This model appeals to price-sensitive users and aligns with municipal goals. Moreover, during major events, shared rides accounted for a share of all platform trips, reducing the need for additional vehicles. Shared services offer a scalable compromise for dense cities, improving economic and environmental efficiency by balancing the needs of public transit users with those of private hire customers.

MARKET CHALLENGES Driver Shortages Due to Regulatory and Economic Pressures

A sustained shortage of qualified drivers, driven by tightening regulations and unfavorable economics, holds back the growth of the Europe ride-sharing market. A full-time driver’s typical net income has decreased, making the profession less viable. This is contributing to high turnover rates, with many drivers leaving the sector each year. The situation is exacerbated by new entry barriers. Operational costs and regulatory hurdles are rising. In some regions, new requirements like mandatory professional licenses and stringent local knowledge tests impose additional financial and time burdens on prospective drivers. These conditions deter new entrants and accelerate churn among existing ones. A lack of stable and motivated drivers leads to an unreliable service, which causes longer wait times, higher costs, and users abandoning the service for private or public transport.

Fragmented Data Privacy and Cross-Border Operational Barriers

Varying national regulations on data protection and transport in the region prevent ride-sharing companies from offering scalable and seamless cross-border services, which in turn constrains the expansion of the Europe ride-sharing market. “The General Data Protection Regulation provides a starting point, but countries layer on extra, localized requirements concerning data in the mobility industry. Furthermore, driver licensing is not mutually recognized. The fragmentation prevents the emergence of truly pan-European services and forces companies to duplicate compliance infrastructure in each market. The market’s current fragmentation, a result of differing national rules, stifles innovation and hinders the achievement of economies of scale; a unified approach, such as that proposed by the EU Urban Mobility Framework, is essential.

REPORT COVERAGE

REPORT METRIC

DETAILS

Market Size Available

2024 to 2033

Base Year

2024

Forecast Period

2025 to 2033

Segments Covered

By Type, Commute Type, Application Type, and Country

Various Analyses Covered

Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities

Country Covered

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe.

Market Leaders Profiled

Uber Technologies Inc., DiDi Global Inc., Gett, Grab, Bolt Technology OÜ, Careem, Cabify España S.L.U., Lyft, Inc., Zimride, car2go Group GmbH, and Others.

SEGMENTAL ANALYSIS By Type Insights

The e-hailing segment held the leading share of the Europe ride-sharing market in 2024. The dominance of the e-hailing segment is propelled by its alignment with smartphone penetration on on-demand expectations, and urban mobility patterns across the continent. The near-universal adoption of smartphones among urban Europeans is a key enabler of this segment. Unlike station-based models, which require fixed docking points and dedicated parking spaces, e-hailing leverages existing road networks and private vehicles, making it instantly scalable in dense cities where space is constrained. Furthermore, e-hailing integrates effortlessly with digital payment ecosystems. This frictionless experience reinforces user preference and ensures e-hailing remains the default choice for spontaneous urban travel.

The station-based ride-sharing segment is expected to exhibit a noteworthy CAGR of 12.3% from 2025 to 2033 due to municipal partnerships and integration with public transit networks in mid-sized cities where traffic density is moderate but last-mile connectivity is weak. Unlike large capitals, where e-hailing dominates, station-based models thrive in cities like Utrecht and Graz, where local governments control dedicated pick-up and drop-off zones near train stations and hospitals. These zones reduce cruising and congestion while ensuring predictable wait times. Apart from these, station-based services appeal to older and less tech-savvy users who prefer scheduled pickups over dynamic booking. Corporate clients also favor this model for employee shuttling. This structured reliability makes station-based sharing a strategic component of Europe’s multimodal future.

By Commute Type Insights

The intercity ride-sharing segment was the largest in the Europe ride-sharing market and captured a 52.4% share in 2024. The leading position of the intercity ride-sharing segment is attributed to Europe’s dense network of secondary cities connected by highways but underserved by high-frequency rail or air links. The cost advantage over trains and rental cars is a major accelerator of this segment. In Eastern Europe, the gap is wider. Moreover, ride sharing fills service gaps where public transport is sparse. This functional necessity, combined with price sensitivity, ensures intercity sharing remains the backbone of cross-regional mobility, especially among students and budget-conscious travelers.

The corporate commute segment is predicted to witness the highest CAGR of 14.1% between 2025 and 2033. The rapid expansion of the corporate commute segment is fueled by corporate sustainability mandates and duty of care policies that prioritize secure, trackable, and carbon accountable employee transportation. Multinational companies are increasingly replacing traditional car allowances with managed ride-sharing programs. Additionally, ride sharing offers superior safety features, including real-time GPS tracking, driver background checks, and automatic incident reporting, which fulfill employer liability requirements. This convergence of cost control compliance and ESG goals positions corporate sharing as a strategic pillar of future workforce mobility.

By Application Type Insights

The Android segment led the Europe ride-sharing market in 2024. The platform’s broader device affordability and deeper penetration in Southern and Eastern Europe, where budget smartphones dominate the market, largely contribute to the growth of the Android segment. The widespread accessibility ensures that ride-sharing apps reach a broader socioeconomic base, including part-time drivers who rely on older devices. Moreover, Android’s open architecture allows for deeper integration with local payment systems such as iDEAL in the Netherlands and BLIK in Poland, which are not universally supported on iOS. Apart from these, Android’s background processing efficiency enables longer battery life during navigation critical for drivers completing multiple trips daily. This functional and economic alignment cements Android as the backbone of Europe’s ride-sharing ecosystem.

The iOS application segment is estimated to register the fastest CAGR of 9.8% during the forecast period. The swift acceleration of the iOS application segment is driven by its stronghold in premium and corporate ride-sharing segments across Western and Northern Europe. This growth further stems from iOS’s concentration among high-income professionals who constitute the core user base for premium services. Corporate travel programs also favor iOS due to superior enterprise security features. Additionally, Apple Pay integration offers seamless one-tap payment. This premium positioning ensures iOS remains the growth leader even as Android maintains volume dominance.

COUNTRY LEVEL ANALYSIS France Ride Sharing Market Analysis

France dominated the Europe ride-sharing market by accounting for a 22.6% share in 2024. The supremacy of France in the regional market is attributed to its progressive yet stringent regulatory framework that balances innovation with social equity. The country was the first in Europe to introduce the Loi Thévenoud, which established professional licensing for drivers and minimum vehicle standards, setting a template later adopted by Spain and Italy. France’s leadership is reinforced by strong public-private collaboration. This regulatory foresight, combined with high smartphone penetration and cultural openness to digital services, ensures France remains Europe’s most dynamic and influential ride-sharing market.

United Kingdom Ride Sharing Market Analysis

The United Kingdom was the second-largest player in the Europe ride-sharing market and captured a 19.5% share in 2024. The growth of the UK market is propelled by its dominance in premium and corporate segments, particularly in London. According to sources, a share of ride-sharing trips in the capital exceeds 20 pounds, reflecting high-income user concentration and business travel demand. The UK also hosts Europe’s most active corporate ride-sharing adoption. Despite Brexit-related driver shortages, the market remains resilient due to strong digital infrastructure. The UK has the highest mobile payment adoption in Europe. Apart from these, London’s congestion charge and ultra-low emission zone incentivize shared rides. This blend of economic incentives, corporate integration, and financial digitization sustains the UK’s pivotal position.

Germany Ride Sharing Market Analysis

Germany expanded steadily in the Europe ride-sharing market due to its rigorous sustainability standards and rapid fleet electrification. The country’s approach emphasizes integration over disruption. Free Now, a joint venture between BMW and Mercedes, operates as a mobility aggregator combining ride sharing e e-scooters, and public transit in one app used by millions of Germans. Moreover, Germany enforces some of Europe’s strictest driver protections. This balance of green policy, social responsibility, and multimodal innovation cements Germany’s leadership.

Spain Ride Sharing Market Analysis

Spain is growing moderately in the Europe ride-sharing market owing to its extensive inter-city carpooling culture and high youth adoption. Spain has experienced significant growth in inter-city ride-sharing, particularly on key routes such as Madrid-Barcelona, Valencia, and Seville, often complementing existing high-speed rail services. This mode of transport has become essential for mobility, especially in areas with less frequent or expensive rail options. The success of ride-sharing in Spain is influenced by a young demographic and geographic factors, including limited rail connectivity in rural regions, which creates a vital transport alternative. Apart from these, cities like Barcelona have partnered with platforms to provide subsidized rides during public transit strikes, ensuring service continuity. This organic integration into daily life, combined with low-cost accessibility, makes Spain a resilient and high-volume market.

Italy Ride Sharing Market Analysis

Italy is anticipated to expand in the Europe ride-sharing market during the forecast period due to extreme urban density, historic city restrictions, and mass tourism. In Italy, a strong trend exists where the vast majority of ride-sharing activity is concentrated in major urban centers. Factors such as narrow streets and difficult parking in cities like Rome, Milan, Naples, Turin, and Florence make private car ownership less practical, increasing reliance on these services. Tourism also significantly boosts demand, especially in popular destinations like Venice and Florence, where a substantial portion of summer trips are booked by international visitors. This fusion of necessity tourism and regulatory adaptation ensures Italy’s sustained relevance in the European landscape.

COMPETITIVE LANDSCAPE

Competition in the Europe ride-sharing market is characterized by a tripartite dynamic between global tech platforms, European homegrown operators, and automotive-backed mobility aggregators. Unlike other regions, Europe’s fragmented regulatory landscape prevents winner-take-all dominance, forcing companies to adapt to local labor, environmental, and transport laws. This has elevated the importance of compliance, collaboration, and sustainability over pure scale. Bolt leverages its European identity to gain policy favor while Uber counters with global capital and corporate solutions. Free Now benefits from automotive integration and public trust. New entrants face high barriers due to driver acquisition costs, regulatory licensing, and city-level caps on vehicle numbers. Consequently, competition centers on service quality, fleet modernization, public partnerships, and ESG credentials rather than price wars, ensuring a mature and multifaceted market structure.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe ride-sharing market include

Uber Technologies Inc. DiDi Global Inc. Gett Grab Bolt Technology OÜ Careem Cabify España S.L.U. Lyft, Inc. Free Now Zimride car2go Group GmbH TOP PLAYERS IN THE MARKET Bolt is a leading European ride-sharing platform headquartered in Tallinn with deep operational roots across multiple cities in the region. The company distinguishes itself through aggressive pricing, localized customer support, and a strong focus on driver welfare, including fuel subsidies and insurance partnerships. It also integrated multimodal options such as e-scooters and public transit routing into its app across Germany and the Netherlands, enhancing its position as a Mobility as a Service provider. These initiatives reinforce Bolt’s identity as a homegrown European alternative to global giants while advancing sustainability and user convenience. Uber maintains a significant presence in the Europe ride-sharing market through its scalable technology infrastructure and diversified service portfolio, including Uber, Uber Green, and Uber Connect. The company has strategically aligned with European regulatory frameworks by classifying thousands of drivers as employees in countries like France and the Netherlands. It also achieved carbon-neutral rides in London and Amsterdam through verified offset programs and EV incentives. These moves demonstrate Uber’s commitment to compliance, stakeholder engagement, and premium segment growth while leveraging its global brand equity. Free Now is a pan-European mobility platform co-owned by Mercedes-Benz and BMW, offering ride-hailing, e-scooter sharing, and taxi integration across 100 cities. The company leverages its automotive heritage to prioritize vehicle quality, safety, and electrification, with over 60 percent of its fleet now electric or hybrid. It also introduced real-time carbon footprint tracking for every trip, enabling users to make environmentally conscious choices. By positioning itself as a regulated, integrated, and sustainable mobility partner, Free Now bridges the gap between legacy automotive giants and digital disruption. TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe ride-sharing market are prioritizing full fleet electrification to comply with urban zero-emission mandates and appeal to eco-conscious consumers. They are forming strategic partnerships with municipal governments to operate as complementary public transport extensions, particularly in rural and suburban zones. Companies are investing in multimodal integration by bundling ride sharing with e-scooter bikes and transit data within a single app. Regulatory compliance is being proactively addressed through driver reclassification benefit packages and transparent data sharing with city authorities. Additionally, platforms are expanding corporate mobility programs, offering enterprises trackable, safe, and carbon-accountable employee transportation solutions.

MARKET SEGMENTATION

This research report on the Europe ride-sharing market has been segmented and sub-segmented into the following categories.

By Type

By Commute Type

Intercity Long Distance Corporate

By Application Type

By Country

United Kingdom France Spain Germany Italy Russia Sweden Denmark Switzerland Netherlands Rest of Europe