As the European markets continue to flourish, with the STOXX Europe 600 Index reaching new highs and closing out 2025 with its strongest annual performance since 2021, investors are keenly eyeing stocks that may be trading below their fair value. In such a buoyant market environment, identifying undervalued stocks involves looking for companies with solid fundamentals that might not yet be fully recognized by the market.

Top 10 Undervalued Stocks Based On Cash Flows In EuropeNameCurrent PriceFair Value (Est)Discount (Est)STEICO (XTRA:ST5)€20.20€39.5748.9%Ottobock SE KGaA (XTRA:OBCK)€70.75€138.4548.9%Nokian Panimo Oyj (HLSE:BEER)€2.485€4.8849%Micro Systemation (OM:MSAB B)SEK63.40SEK126.7350%Galderma Group (SWX:GALD)CHF163.20CHF320.6349.1%Fodelia Oyj (HLSE:FODELIA)€5.46€10.7249.1%Esautomotion (BIT:ESAU)€3.10€6.1049.2%DEUTZ (XTRA:DEZ)€9.615€19.0349.5%Boliden (OM:BOL)SEK547.20SEK1093.2749.9%ArcticZymes Technologies (OB:AZT)NOK23.30NOK45.6849%

We’re going to check out a few of the best picks from our screener tool.

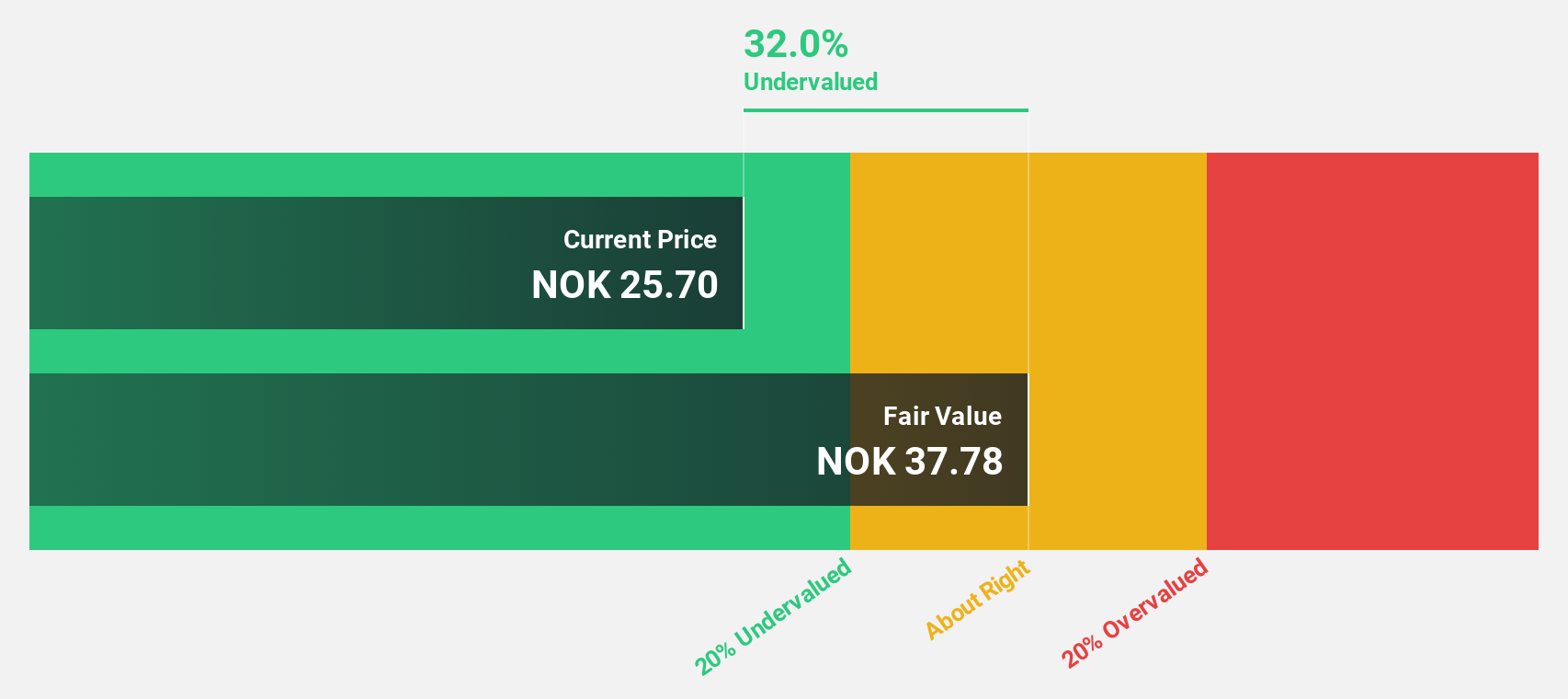

Overview: SmartCraft ASA offers software solutions tailored for the construction industry across Norway, Sweden, Finland, and the United Kingdom, with a market capitalization of NOK4.24 billion.

Operations: SmartCraft ASA generates revenue through its provision of software solutions to the construction sector in Norway, Sweden, Finland, and the United Kingdom.

Estimated Discount To Fair Value: 32%

SmartCraft is trading at NOK 25.7, significantly below its estimated fair value of NOK 37.77, reflecting a substantial undervaluation based on discounted cash flow analysis. Despite slower forecasted revenue growth of 11.6% annually compared to the desired threshold, earnings are expected to grow significantly at over 30% per year, outpacing the Norwegian market average. Recent buybacks and stable third-quarter results reinforce its financial stability amidst executive changes with an interim CFO appointment effective December 2025.

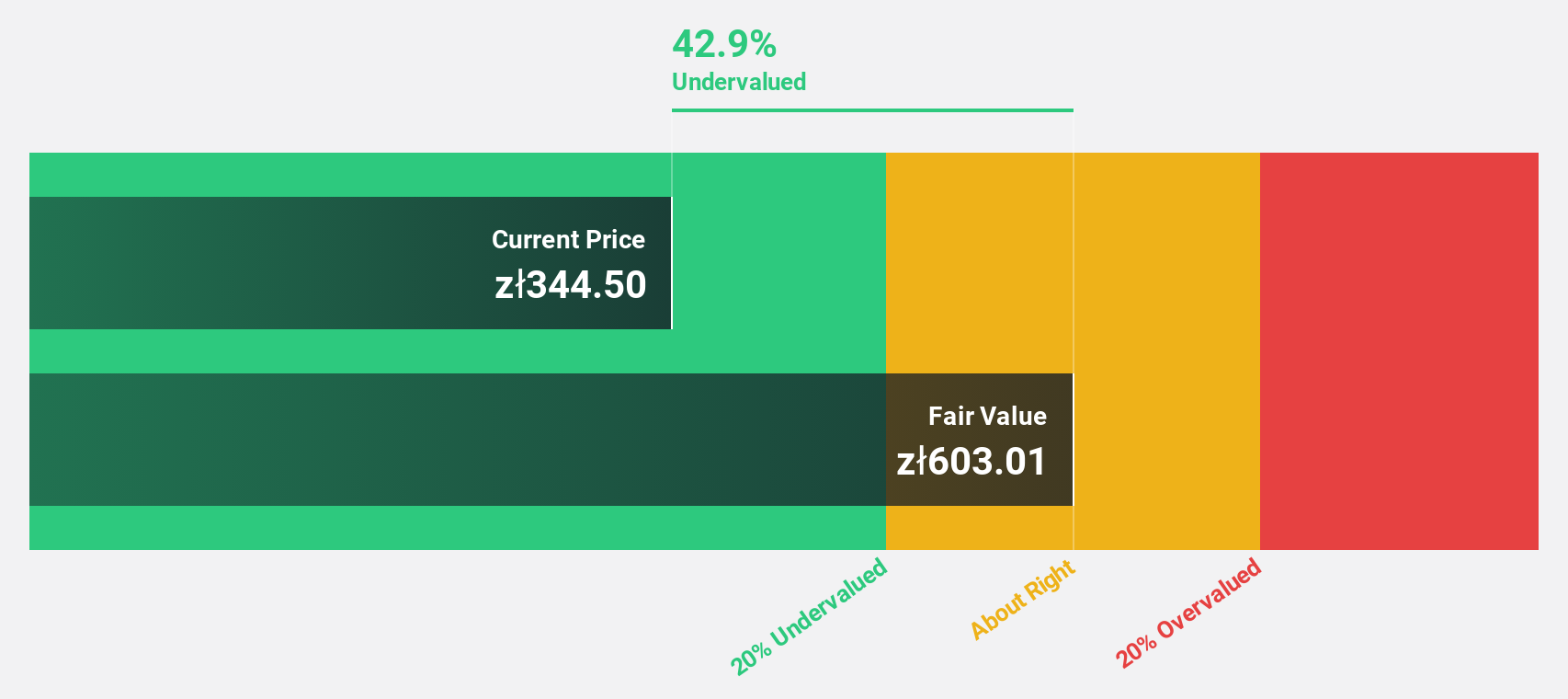

Overview: Mo-BRUK S.A. is involved in the processing of industrial, hazardous, and municipal waste across several European countries including Poland, Germany, Italy, Slovenia, Denmark, Romania, and Lithuania with a market cap of PLN1.21 billion.

Operations: Mo-BRUK S.A. generates revenue from processing industrial, hazardous, and municipal waste in multiple European nations such as Germany, Italy, Slovenia, Denmark, Romania, and Lithuania.

Estimated Discount To Fair Value: 42.9%

Mo-BRUK is trading at PLN 344.5, significantly below its estimated fair value of PLN 603.01, indicating a substantial undervaluation based on discounted cash flow analysis. Despite slower revenue growth forecasts of 5.5% annually, earnings are expected to grow significantly at 64.44% per year, outpacing the Polish market average. However, recent earnings reports show a net loss for both the third quarter and nine months ended September 2025 due to declining profit margins and increased losses compared to last year.

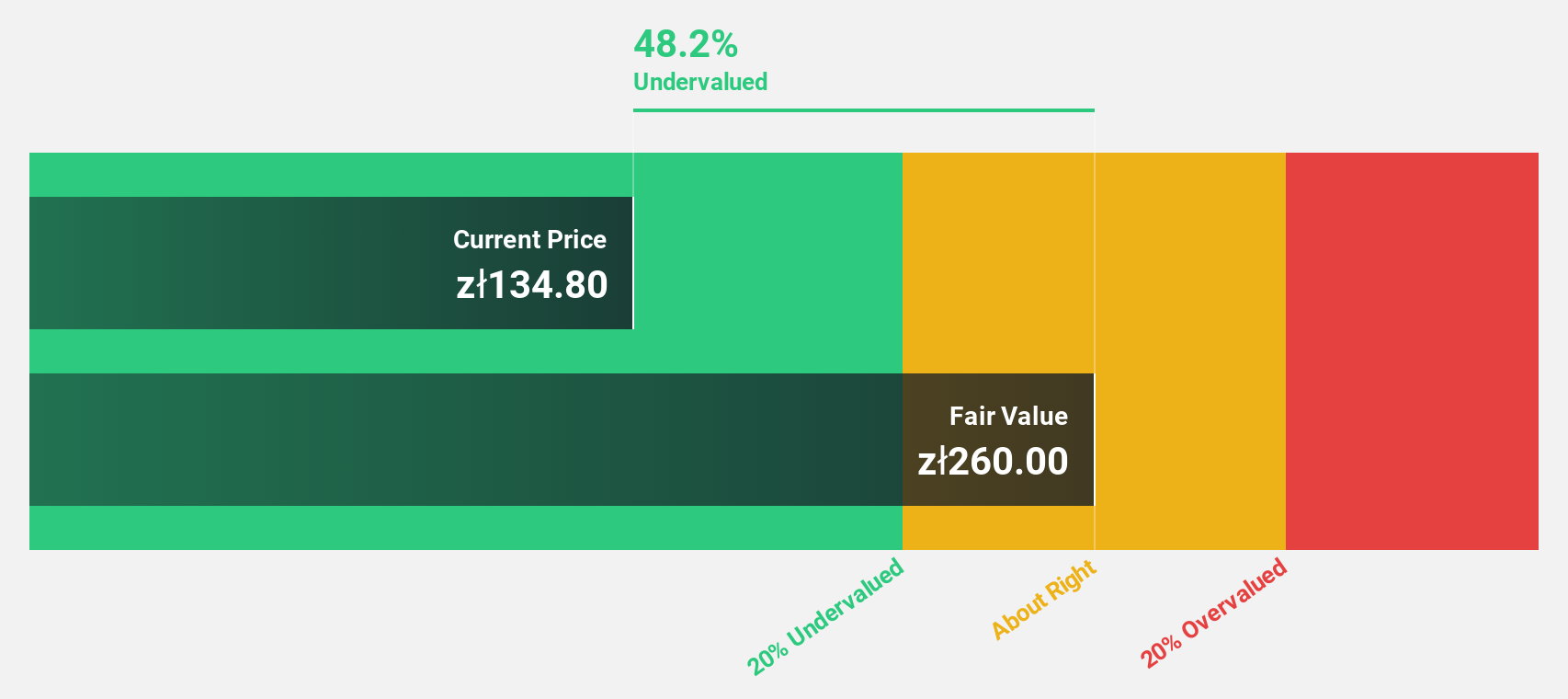

Overview: Unimot S.A. is an independent fuel importer involved in the wholesale and distribution of diesel oil and other liquid fuels both in Poland and internationally, with a market cap of PLN1.11 billion.

Operations: The company’s revenue segments include Liquid Fuels (PLN10.50 billion), Bitumen (PLN1.44 billion), Fuel Stations (PLN899.68 million), LPG (PLN896.15 million), Natural Gas (PLN815.85 million), Electric Energy (PLN520.70 million), Infrastructure and Logistics (PLN409.95 million), Solid Fuel (PLN154.88 million), and Renewable Energy Sources (PLN70.35 million).

Estimated Discount To Fair Value: 48.2%

Unimot, trading at PLN 134.8, is considerably undervalued against its fair value estimate of PLN 260. Despite a forecasted revenue growth of 8.3% annually, which is faster than the Polish market’s average, earnings are expected to rise significantly by 63% per year. However, interest payments remain inadequately covered by earnings. Recent reports show improved quarterly net income but a nine-month net loss compared to last year’s profit, highlighting financial volatility amidst growth prospects.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice.

It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com