In December 2025, EU imports of Russian gas increased 13% month-on-month, rising by 0.42 bcm compared to November. This growth was driven mainly by LNG imports, which rose 18% (0.33 bcm), while pipeline imports increased 6% (0.10 bcm).

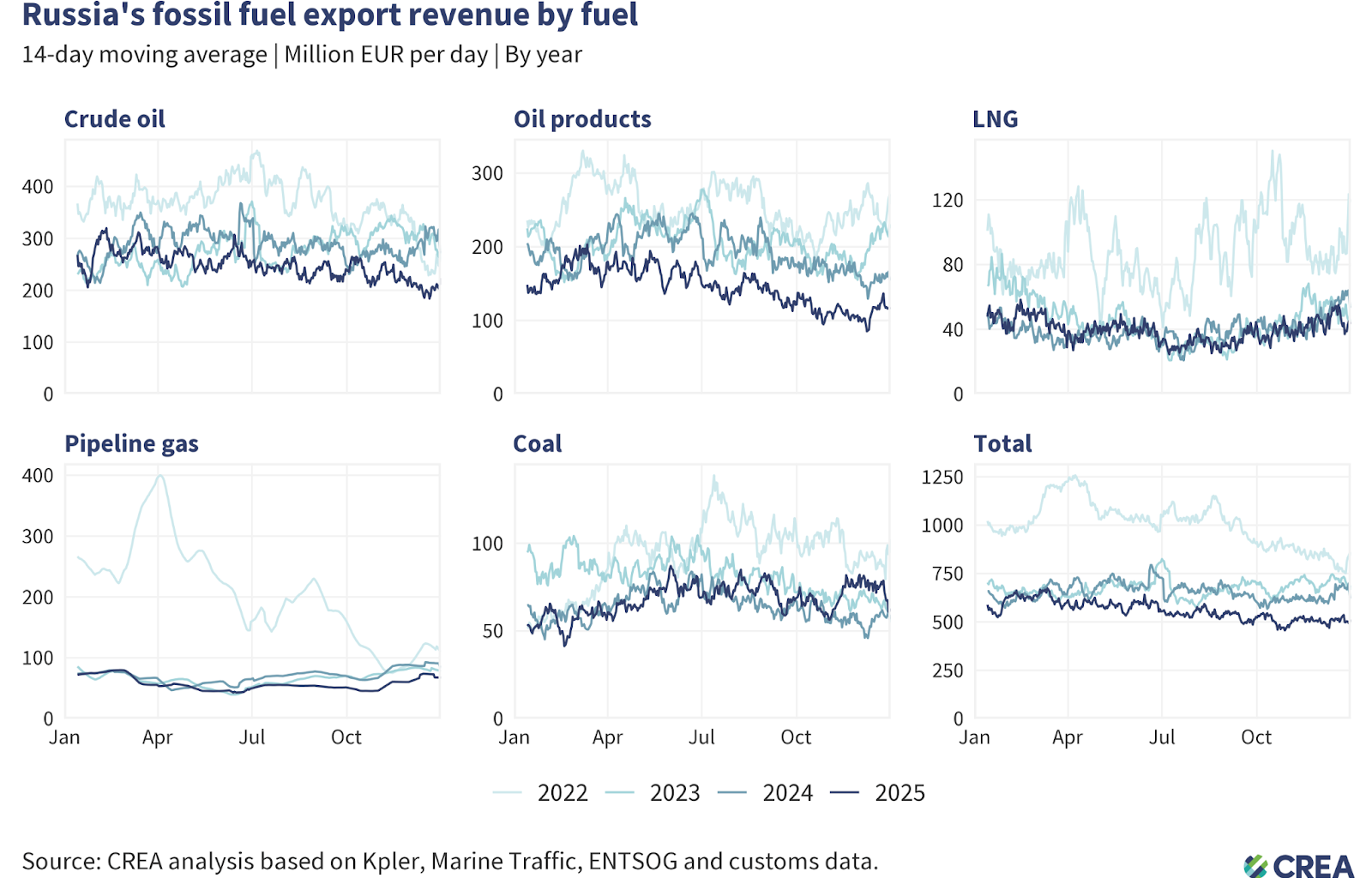

In 2025, EU imports of Russian gas declined 31% year-on-year, falling by 16.62 bcm. Pipeline imports dropped sharply 45% (13.68 bcm), while LNG imports fell 13% (2.94 bcm). Since the start of 2025, gas transit via Ukraine has completely stopped, leaving TurkStream as the only pipeline transporting Russian gas to the EU. Despite the overall decline, TurkStream flows increased 8% year-on-year, partially offsetting the loss of Ukrainian transit.

While there was a decrease in Russian gas flows into the EU, parallely there was a 10% year-on-year increase in power generation from fossil gas in 2025, equalling a total of 35.2 TWh. The increase means that overall gas imports for power generation increased and other sources made up for the fall in gas from Russia. The increase was weather-driven in the short term, but shows the need to rapidly increase clean electricity generation to reduce reliance on imported fossil fuels.

Coal and gas contributed to 26% of the EU’s total electricity production in 2025, a marginal increase from last year when fossil fuels contributed 24% to the total electricity mix.

There was a significant 17% (40.7 TWh) year-on-year increase in solar power generation, with almost every Member State increasing their electricity production from the source in 2025. This increase in solar power generation resulted in fossil gas savings of 81.4 TWh, equal to 11% of the bloc’s total gas in storage at the end of 2025. The growth in generation was driven by a sharp increase in capacity in 2023–24, but capacity growth slowed down in 2025, for the first time since 2016.

There was a marginal 2% (11.1 TWh) year-on-year reduction in wind power generation due to poorer wind conditions than the year before. The lack of growth however highlights the lacklustre pace of capacity additions. Weak capacity additions of both wind and solar in 2025 show the need to speed up permitting, resolve grid bottlenecks and address other obstacles to faster deployment.

The main reason for the increase in power generation from gas was a massive 15% (48 TWh) year-on-year drop in hydroelectric power generation, mainly due to hot weather and droughts exacerbated by a dry winter. It also meant that hydropower’s share in the total electricity mix dropped from 13% in 2024 to 11% in 2025.