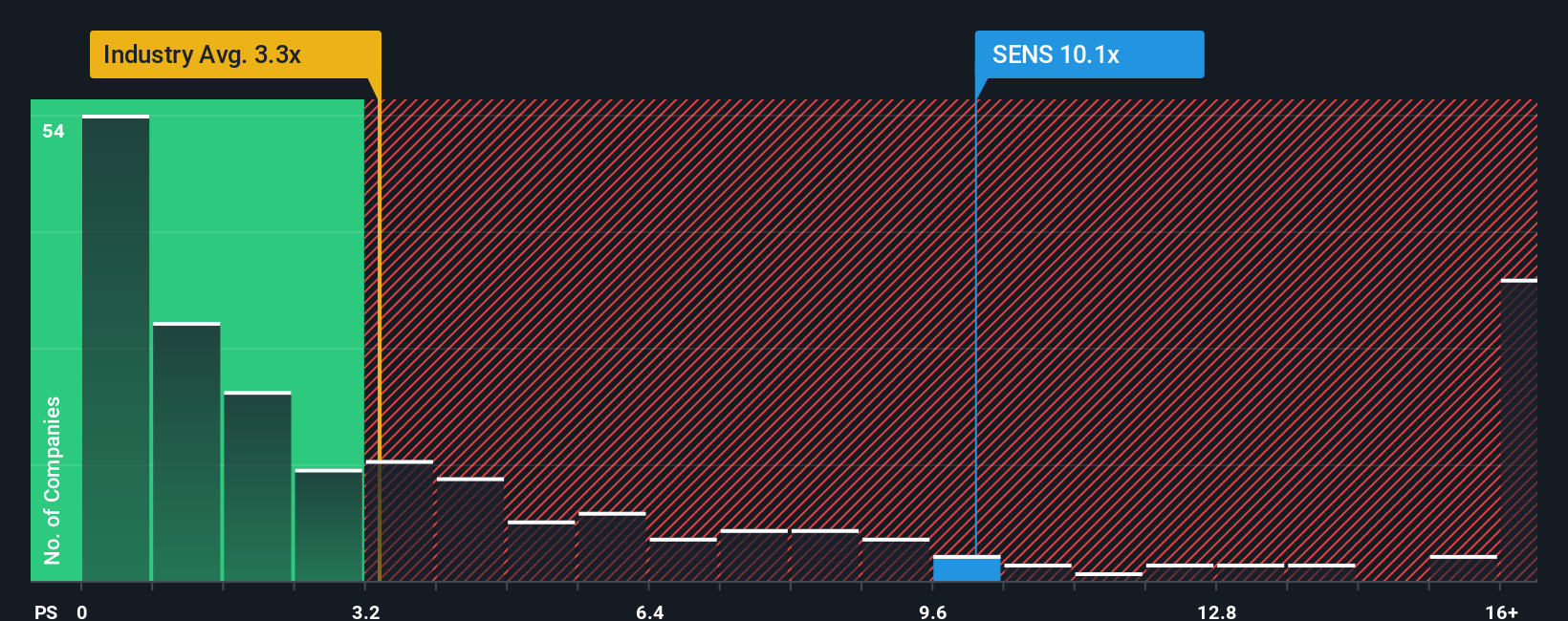

You may think that with a price-to-sales (or “P/S”) ratio of 9.9x Senseonics Holdings, Inc. (NASDAQ:SENS) is a stock to avoid completely, seeing as almost half of all the Medical Equipment companies in the United States have P/S ratios under 3.3x and even P/S lower than 1.2x aren’t out of the ordinary. Although, it’s not wise to just take the P/S at face value as there may be an explanation why it’s so lofty.

See our latest analysis for Senseonics Holdings

NasdaqGS:SENS Price to Sales Ratio vs Industry January 13th 2026 How Senseonics Holdings Has Been Performing

NasdaqGS:SENS Price to Sales Ratio vs Industry January 13th 2026 How Senseonics Holdings Has Been Performing

With revenue growth that’s superior to most other companies of late, Senseonics Holdings has been doing relatively well. The P/S is probably high because investors think this strong revenue performance will continue. However, if this isn’t the case, investors might get caught out paying too much for the stock.

Want the full picture on analyst estimates for the company? Then our free report on Senseonics Holdings will help you uncover what’s on the horizon. Do Revenue Forecasts Match The High P/S Ratio?

Senseonics Holdings’ P/S ratio would be typical for a company that’s expected to deliver very strong growth, and importantly, perform much better than the industry.

Taking a look back first, we see that the company grew revenue by an impressive 32% last year. The strong recent performance means it was also able to grow revenue by 98% in total over the last three years. So we can start by confirming that the company has done a great job of growing revenue over that time.

Looking ahead now, revenue is anticipated to climb by 63% per year during the coming three years according to the seven analysts following the company. That’s shaping up to be materially lower than the 112% per annum growth forecast for the broader industry.

In light of this, it’s alarming that Senseonics Holdings’ P/S sits above the majority of other companies. Apparently many investors in the company are way more bullish than analysts indicate and aren’t willing to let go of their stock at any price. Only the boldest would assume these prices are sustainable as this level of revenue growth is likely to weigh heavily on the share price eventually.

The Key Takeaway

We’d say the price-to-sales ratio’s power isn’t primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

Despite analysts forecasting some poorer-than-industry revenue growth figures for Senseonics Holdings, this doesn’t appear to be impacting the P/S in the slightest. The weakness in the company’s revenue estimate doesn’t bode well for the elevated P/S, which could take a fall if the revenue sentiment doesn’t improve. Unless these conditions improve markedly, it’s very challenging to accept these prices as being reasonable.

Before you settle on your opinion, we’ve discovered 2 warning signs for Senseonics Holdings (1 is concerning!) that you should be aware of.

If strong companies turning a profit tickle your fancy, then you’ll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.