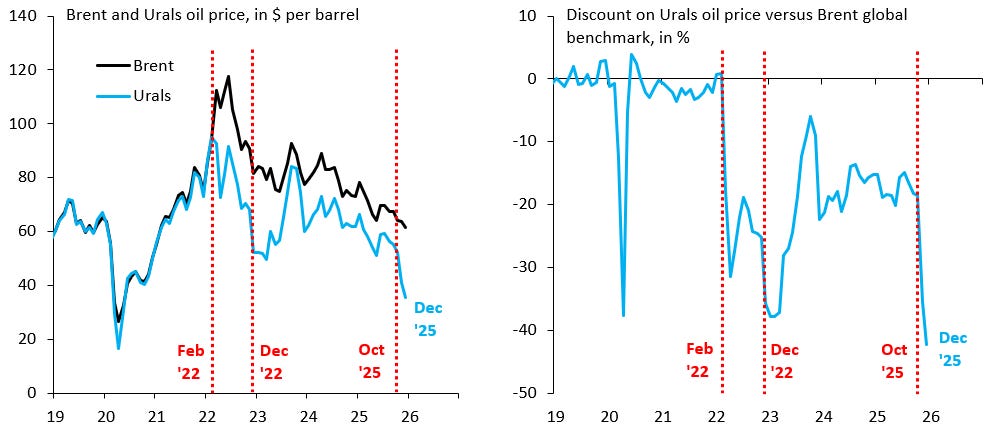

Back in October, the Trump administration announced sanctions on Russia’s two biggest oil companies: Rosneft and Lukoil. At the time, I wrote that this was a very big deal for two reasons: (i) it marks the first time the Trump administration has used sanctions against Russia; and (ii) it sharply raises the stigma around buying Russian oil, as secondary sanctions by the US carry the threat of freezing potential buyers out of Dollar payment networks. I predicted that the discount on Urals crude versus Brent would widen significantly, which is exactly what’s happened. In percentage terms, the Urals oil price has fallen to a record low versus Brent. This hits Russia hard and runs counter to the wide-spread narrative that President Trump is sympathetic towards Putin. Maybe he is, but the truth is more complex and nuanced.

The black line in the left chart above is the global benchmark Brent oil price. The blue line is the Urals oil price. The right chart shows the discount of Urals versus Brent in percent. This discount has widened sharply at different points since Russia’s invasion: (i) it widened right after the invasion in February 2022 when markets shunned Russian oil for fear of Western sanctions; (ii) it widened further in December 2022 when the G7 announced the oil price cap on Russia; and (iii) it went to its widest ever in December 2025 after the bulk of Rosneft and Lukoil sanctions took effect in November 2025.

The sharp drop in the Urals oil price – to levels last seen in 2020 during COVID – is a major blow to Russia’s war economy. All else equal, this puts downward pressure on the current account surplus and thereby the Ruble, which puts upward pressure on inflation, forcing the central bank to keep interest rates higher than otherwise.

Maybe President Trump is sympathetic to Putin on some level, but the sharp drop in Urals oil price after recent US sanctions confounds that narrative. These sanctions are packing a serious punch and are hurting Russia.