GeneDx Holdings Corp. (NASDAQ:WGS) shares have had a horrible month, losing 29% after a relatively good period beforehand. Still, a bad month hasn’t completely ruined the past year with the stock gaining 34%, which is great even in a bull market.

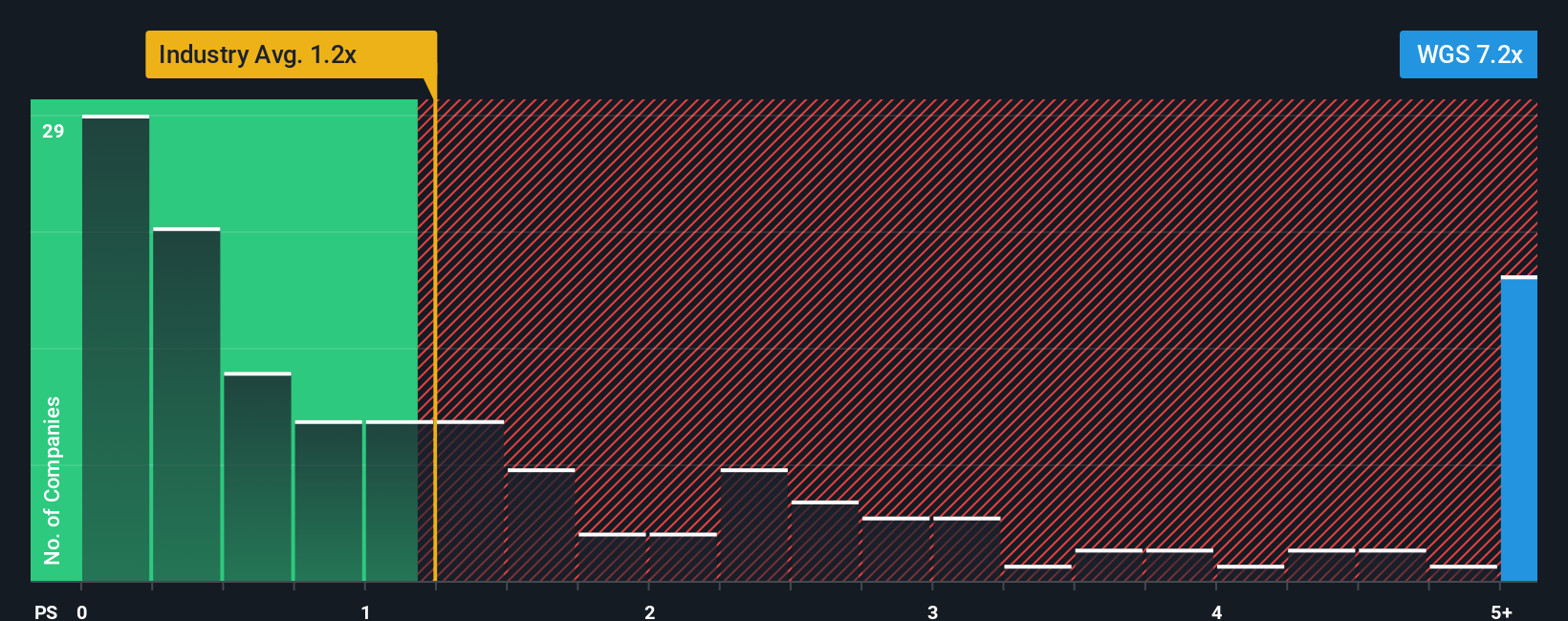

Although its price has dipped substantially, you could still be forgiven for thinking GeneDx Holdings is a stock to steer clear of with a price-to-sales ratios (or “P/S”) of 7.2x, considering almost half the companies in the United States’ Healthcare industry have P/S ratios below 1.3x. Nonetheless, we’d need to dig a little deeper to determine if there is a rational basis for the highly elevated P/S.

Check out our latest analysis for GeneDx Holdings

NasdaqGS:WGS Price to Sales Ratio vs Industry January 21st 2026 How GeneDx Holdings Has Been Performing

NasdaqGS:WGS Price to Sales Ratio vs Industry January 21st 2026 How GeneDx Holdings Has Been Performing

GeneDx Holdings certainly has been doing a good job lately as it’s been growing revenue more than most other companies. The P/S is probably high because investors think this strong revenue performance will continue. However, if this isn’t the case, investors might get caught out paying too much for the stock.

If you’d like to see what analysts are forecasting going forward, you should check out our free report on GeneDx Holdings. What Are Revenue Growth Metrics Telling Us About The High P/S?

GeneDx Holdings’ P/S ratio would be typical for a company that’s expected to deliver very strong growth, and importantly, perform much better than the industry.

Taking a look back first, we see that the company grew revenue by an impressive 51% last year. The latest three year period has also seen an excellent 74% overall rise in revenue, aided by its short-term performance. So we can start by confirming that the company has done a great job of growing revenue over that time.

Shifting to the future, estimates from the seven analysts covering the company suggest revenue should grow by 22% per annum over the next three years. With the industry only predicted to deliver 6.1% per year, the company is positioned for a stronger revenue result.

With this in mind, it’s not hard to understand why GeneDx Holdings’ P/S is high relative to its industry peers. Apparently shareholders aren’t keen to offload something that is potentially eyeing a more prosperous future.

The Key Takeaway

GeneDx Holdings’ shares may have suffered, but its P/S remains high. We’d say the price-to-sales ratio’s power isn’t primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

We’ve established that GeneDx Holdings maintains its high P/S on the strength of its forecasted revenue growth being higher than the the rest of the Healthcare industry, as expected. It appears that shareholders are confident in the company’s future revenues, which is propping up the P/S. Unless the analysts have really missed the mark, these strong revenue forecasts should keep the share price buoyant.

We don’t want to rain on the parade too much, but we did also find 2 warning signs for GeneDx Holdings that you need to be mindful of.

It’s important to make sure you look for a great company, not just the first idea you come across. So if growing profitability aligns with your idea of a great company, take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.