The Australian dollar (AUD) remains one of the stronger currencies following higher-than-expected inflation data. The latest CPI reading surprised to the upside in both headline and core inflation, reinforcing the view that price pressures remain too elevated for the Reserve Bank of Australia (RBA) to adopt a dovish — or even neutral — stance anytime soon.

Headline inflation accelerated to 3.8% y/y in December, while core inflation (trimmed mean) rose to around 3.4% y/y, clearly above the RBA’s 2–3% target and confirming that the disinflation process has stalled rather than progressed steadily. On a quarterly basis, core inflation came in at 0.9% q/q, which also does not support a smooth return to target.

Key inflation data

Headline CPI: 3.8% y/y (from 3.4%)

CPI trimmed mean: ~3.4% y/y, above expectations

Core inflation: 0.9% q/q, maintaining strong momentum

Services inflation accelerated to 4.1% y/y

Housing costs remain the biggest driver: +5.5% y/y

The inflation mix is particularly uncomfortable for the RBA. Services inflation has re-accelerated, reflecting strong domestic demand, a tight labour market, and persistent pressure from rents and travel costs. At the same time, goods inflation has picked up again, partly due to a sharp rise in electricity prices. Combined with unemployment around 4% and solid economic growth, the data suggest inflation pressures are becoming increasingly entrenched across key sectors of the economy rather than driven by temporary or imported factors.

Main sources of price pressure

Strong services inflation (rents, travel, market services)

High housing costs weighing on households

Rising energy prices boosting goods inflation

Tight labour market sustaining wage pressures

In response to the data, Australia’s largest banks — including Westpac and ANZ — have begun to expect a 25 bp rate hike from the RBA at the 2–3 February meeting, arguing that inflation has effectively cast the “decisive vote” for tighter policy. Markets are now pricing in over a 70% probability of such a move. While most see it as a one-off hike rather than the start of a full tightening cycle, the RBA is expected to maintain a conditionally hawkish stance, with future decisions tied closely to incoming inflation data. The central bank has also made it clear that inflation above 3% remains “too high,” effectively ruling out near-term rate cuts.

RBA outlook after CPI

February hike increasingly viewed as the base case

Cash rate could rise to around 3.85%

Possible pause thereafter, but with a hawkish bias

Further tightening possible if inflation remains persistent

Market reaction

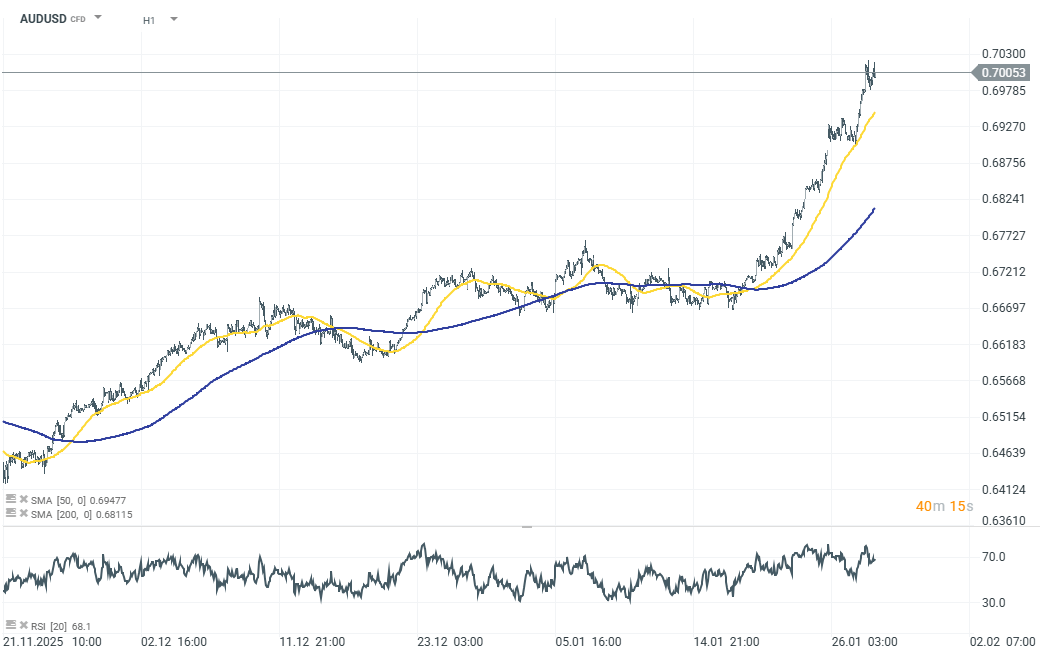

The Australian dollar surged sharply after the release — AUD reached its highest level since early 2023, and AUDUSD broke above 0.70, extending a strong start to the year. Investors have begun positioning for a more hawkish RBA relative to other major central banks. Recent gains in AUDUSD have also been supported by broad weakness in the US dollar.