David Iben put it well when he said, ‘Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. Importantly, BH Co., Ltd. (KRX:090460) does carry debt. But the more important question is: how much risk is that debt creating?

What Risk Does Debt Bring?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we think about a company’s use of debt, we first look at cash and debt together.

What Is BH’s Debt?

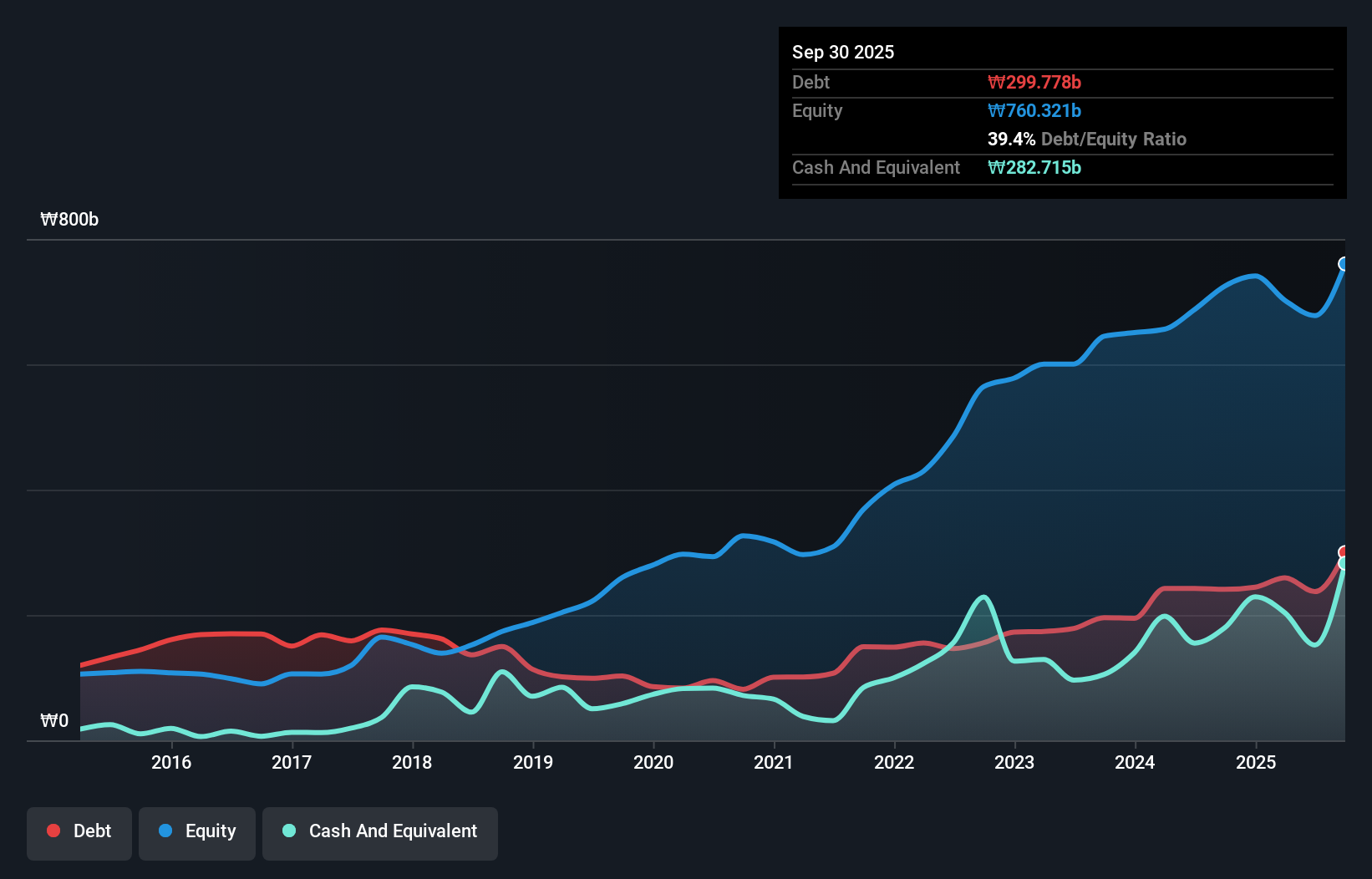

As you can see below, at the end of September 2025, BH had ₩299.8b of debt, up from ₩240.9b a year ago. Click the image for more detail. However, it also had ₩282.7b in cash, and so its net debt is ₩17.1b.

KOSE:A090460 Debt to Equity History January 28th 2026 How Healthy Is BH’s Balance Sheet?

KOSE:A090460 Debt to Equity History January 28th 2026 How Healthy Is BH’s Balance Sheet?

Zooming in on the latest balance sheet data, we can see that BH had liabilities of ₩512.3b due within 12 months and liabilities of ₩154.0b due beyond that. On the other hand, it had cash of ₩282.7b and ₩298.5b worth of receivables due within a year. So its liabilities total ₩85.1b more than the combination of its cash and short-term receivables.

Since publicly traded BH shares are worth a total of ₩579.1b, it seems unlikely that this level of liabilities would be a major threat. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward.

Check out our latest analysis for BH

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

While BH’s low debt to EBITDA ratio of 0.21 suggests only modest use of debt, the fact that EBIT only covered the interest expense by 2.5 times last year does give us pause. So we’d recommend keeping a close eye on the impact financing costs are having on the business. Importantly, BH’s EBIT fell a jaw-dropping 82% in the last twelve months. If that earnings trend continues then paying off its debt will be about as easy as herding cats on to a roller coaster. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine BH’s ability to maintain a healthy balance sheet going forward. So if you’re focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a business needs free cash flow to pay off debt; accounting profits just don’t cut it. So it’s worth checking how much of that EBIT is backed by free cash flow. In the last three years, BH created free cash flow amounting to 2.7% of its EBIT, an uninspiring performance. For us, cash conversion that low sparks a little paranoia about is ability to extinguish debt.

Our View

Mulling over BH’s attempt at (not) growing its EBIT, we’re certainly not enthusiastic. But on the bright side, its net debt to EBITDA is a good sign, and makes us more optimistic. Once we consider all the factors above, together, it seems to us that BH’s debt is making it a bit risky. Some people like that sort of risk, but we’re mindful of the potential pitfalls, so we’d probably prefer it carry less debt. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. For example, we’ve discovered 2 warning signs for BH that you should be aware of before investing here.

At the end of the day, it’s often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It’s free.

Discover if BH might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.