As the U.S. markets navigate a period of steady interest rates and mixed performance among major indices, small-cap stocks present intriguing opportunities amid broader economic conditions. With the S&P 600 reflecting these dynamics, investors are keenly observing insider actions as potential indicators of value in this segment. Identifying promising small-cap stocks often involves assessing factors such as market positioning and growth potential in light of current economic trends.

Top 10 Undervalued Small Caps With Insider Buying In The United StatesNamePEPSDiscount to Fair ValueValue RatingPeoples Bancorp10.4×2.6×45.13%★★★★★☆First United9.7×2.9×45.58%★★★★★☆Wolverine World Wide16.2×0.8×36.01%★★★★★☆Shore Bancshares10.8×2.9×42.68%★★★★☆☆MVB Financial10.7×2.0x19.12%★★★☆☆☆New Peoples Bankshares9.6×2.2×40.19%★★★☆☆☆Union Bankshares10.1×2.2×19.35%★★★☆☆☆Angel Oak Mortgage REIT12.8×6.5×36.79%★★★☆☆☆Farmland Partners7.1×8.8x-110.54%★★★☆☆☆VestisNA0.3x-3.44%★★★☆☆☆

Let’s explore several standout options from the results in the screener.

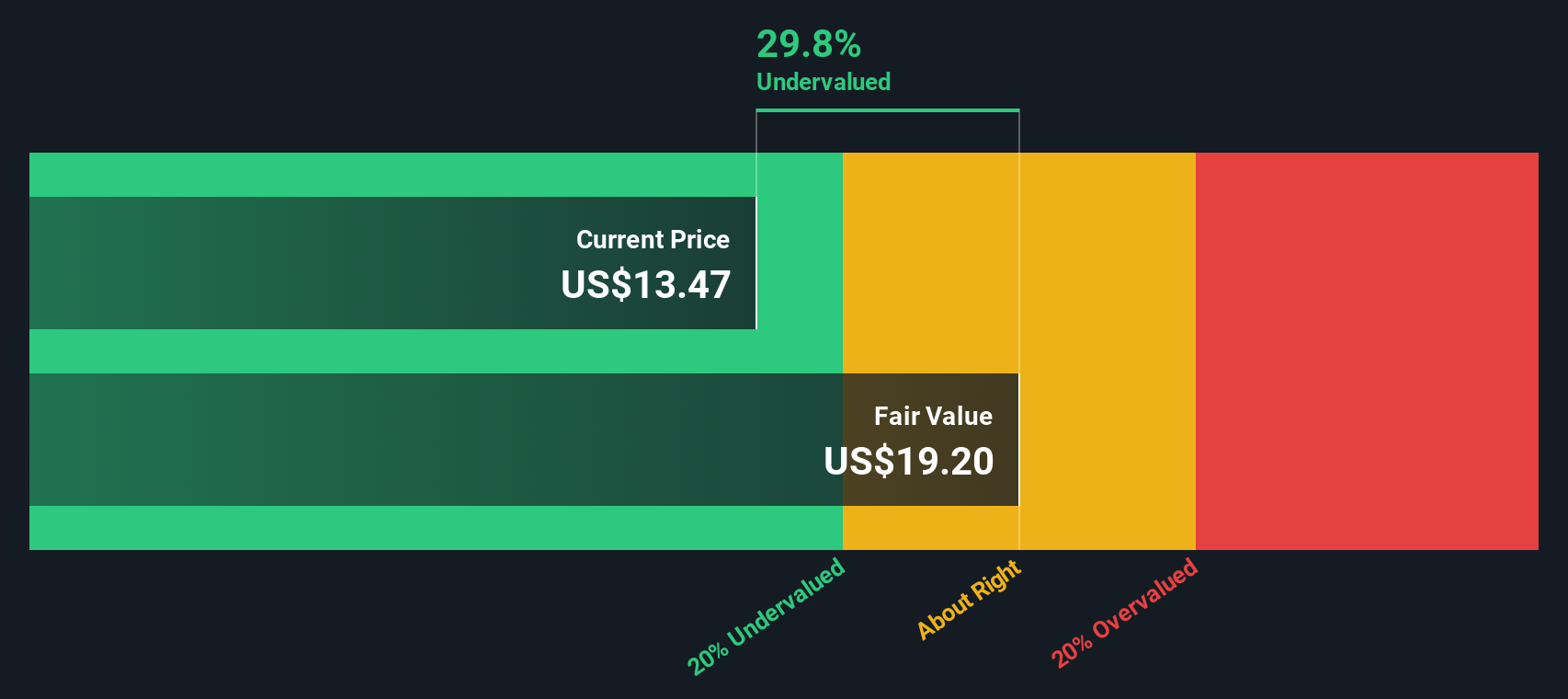

Simply Wall St Value Rating: ★★★☆☆☆

Overview: SNDL is a company engaged in liquor and cannabis retail, as well as cannabis operations, with a market capitalization of CA$1.09 billion.

Operations: The company generates revenue primarily from liquor and cannabis retail, alongside cannabis operations. The gross profit margin has shown an upward trend, reaching 27.13% in the latest period. Operating expenses are substantial, with general and administrative expenses being a significant component.

PE: -6.0x

SNDL, a smaller company in the cannabis industry, has been making strategic moves to potentially enhance its market position. Recently, they announced an acquisition of 32 cannabis retail stores for US$32.2 million in cash, structured over two stages due to regulatory requirements. Despite a volatile share price and reliance on external borrowing for funding, insider confidence is evident with significant share repurchases totaling CAD 26.09 million since November 2024. The company’s ongoing buyback program aims to return value to shareholders by purchasing up to 24.5 million shares by November 2026. While unprofitable currently and not expected to turn profitable soon, these steps could pave the way for future growth as they navigate industry challenges.

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Cross Country Healthcare is a workforce solutions and healthcare staffing company specializing in nurse, allied, and physician staffing services with a market cap of approximately $0.96 billion.

Operations: Cross Country Healthcare’s primary revenue streams come from its Nurse and Allied Staffing segment, generating $925.48 million, and its Physician Staffing segment, contributing $202 million. The company has seen fluctuations in gross profit margin, which was 20.19% as of September 30, 2025. Operating expenses have consistently been a significant part of the cost structure, with general and administrative expenses being a notable component.

PE: -19.0x

Cross Country Healthcare, a small company in the healthcare staffing industry, recently saw leadership changes with Kevin C. Clark returning as CEO. Despite reporting a net loss of US$4.77 million for Q3 2025 and a nine-month loss of US$11.92 million, the company’s strategic buyback completed 16% repurchase of shares worth US$118.12 million since August 2022, indicating insider confidence in its potential value recovery. The cancellation of Aya Healthcare’s acquisition plan adds uncertainty but also highlights market interest in Cross Country’s assets and future prospects under experienced leadership.

Simply Wall St Value Rating: ★★★★☆☆

Overview: Greenlight Capital Re is a reinsurance company that provides property and casualty reinsurance services, with a market capitalization of approximately $0.25 billion.

Operations: Open Market is the primary revenue stream, generating $590.39 million, followed by Innovations at $70.28 million. The company has experienced fluctuations in its gross profit margin, with a notable increase to 20.64% as of September 2023 from previous periods of lower margins. Operating expenses have varied over time but were recorded at $17.87 million in the latest period ending January 2026.

PE: -249.3x

Greenlight Capital Re, a small player in the insurance sector, recently caught attention with insider confidence as CEO Greg Richardson purchased 50,000 shares for US$637,300. Despite facing challenges like a net loss of US$4.41 million in Q3 2025 and reduced revenue of US$146.07 million compared to the previous year, the company shows commitment through share repurchases totaling 512,527 shares for US$7 million by November 2025. While reliant on higher-risk external funding sources, these strategic moves may signal potential value opportunities ahead.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com