Amid renewed trade and geopolitical uncertainty, European markets have seen a downturn, with the pan-European STOXX Europe 600 Index ending 0.98% lower. Despite this challenging environment, business activity in the eurozone remains positive, buoyed by increased new orders and heightened optimism in the business outlook. In such a fluctuating market landscape, identifying promising small-cap stocks often involves looking for companies with solid fundamentals and potential for growth that may be overlooked due to broader market conditions.

Top 10 Undervalued Small Caps With Insider Buying In EuropeNamePEPSDiscount to Fair ValueValue RatingGamma Communications12.5×1.3×46.88%★★★★★★Speedy HireNA0.3×41.05%★★★★★☆Norcros16.4×0.9×30.54%★★★★☆☆Eurocell16.8×0.3×33.56%★★★★☆☆M&C Saatchi22.6×0.4×47.53%★★★★☆☆Eastnine12.7×8.0x47.11%★★★★☆☆Hargreaves Services16.6×0.9×20.82%★★★☆☆☆Young’s Brewery45.6×1.0x33.65%★★★☆☆☆CVS Group48.8×1.4×21.74%★★★☆☆☆Senior32.5×1.0x12.48%★★★☆☆☆

Underneath we present a selection of stocks filtered out by our screen.

Simply Wall St Value Rating: ★★★☆☆☆

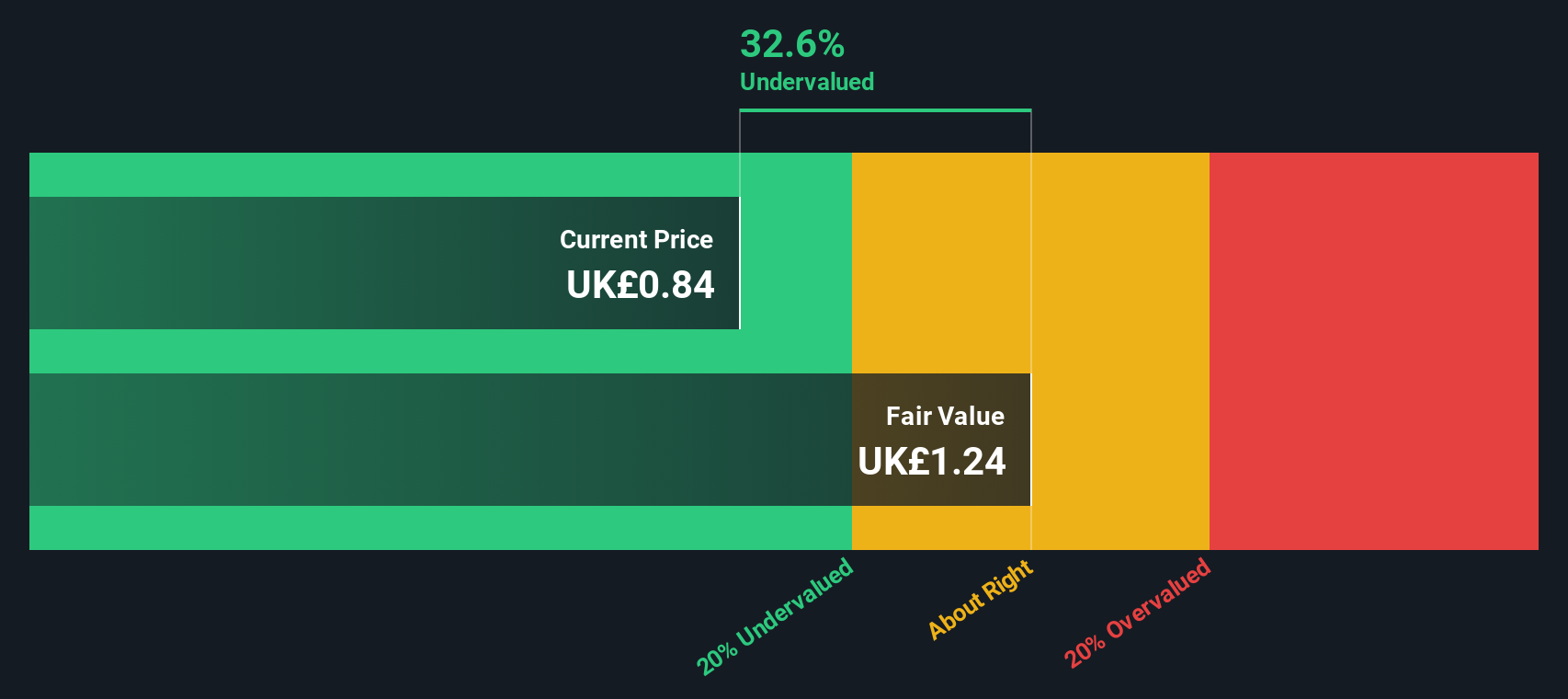

Overview: Grainger is a UK-based residential property company focusing on the Private Rented Sector and reversionary business, with a market capitalization of approximately £2.10 billion.

Operations: The company’s revenue primarily comes from the Private Rented Sector (£162 million) and Reversionary segments (£98.7 million). Over time, it has experienced fluctuations in its net income margin, with a notable peak at 77.12% and a recent decline to 4.56%. Operating expenses have shown variability, impacting overall profitability alongside non-operating expenses that have occasionally been negative, contributing positively to net income.

PE: 7.1x

Grainger, a European property company, is navigating funding challenges with its reliance on external borrowing. Despite forecasts of a 2.1% annual earnings decline over the next three years, Grainger’s strategic investments in Build to Rent (BTR) projects, like the £75 million Guildford Station scheme and the £68.4 million Chiswick Reach development, highlight growth potential through well-connected housing initiatives. Insider confidence is evident from recent share purchases by executives in January 2026, signaling belief in future prospects despite current financial pressures.

Simply Wall St Value Rating: ★★★★☆☆

Overview: International Personal Finance provides consumer credit services through its digital and home credit divisions, with a market cap of approximately £0.24 billion.

Operations: The company’s revenue streams are primarily derived from IPF Digital, Mexico Home Credit, and European Home Credit. Over the years, there has been a notable trend in gross profit margin, peaking at 89.76% in December 2021 before experiencing fluctuations and settling at 84.41% by June 2025. Operating expenses consistently represent a significant portion of the cost structure, with general and administrative expenses being a substantial component.

PE: 7.2x

International Personal Finance, a smaller player in the European market, has recently issued SEK 1 billion in senior unsecured floating rate notes due 2028, priced at par. This move highlights their reliance on external borrowing for funding. Despite this riskier financial structure, insider confidence is evident with recent share purchases by company insiders. Earnings are projected to grow modestly at 3.54% annually, suggesting potential for gradual improvement despite current challenges with interest coverage from earnings.

Simply Wall St Value Rating: ★★★★☆☆

Overview: Supermarket Income REIT focuses on investing in supermarket property assets, with a market cap of £1.28 billion.

Operations: The company’s revenue primarily comes from investments in supermarket property assets, generating £114.77 million in the latest period. It consistently reports a gross profit margin of 100%, indicating no cost of goods sold is recorded against its revenue. Operating expenses have varied over time, with the most recent figure at £28.17 million, impacting net income which has shown fluctuations due to significant non-operating expenses.

PE: 17.0x

Supermarket Income REIT, a company focused on grocery real estate, has been making strategic moves to enhance its portfolio and financial standing. Recent acquisitions of UK supermarkets for £97.6 million at an average yield of 5.5% align with their growth strategy, boosting earnings potential. Insider confidence is evident as the Independent Non-Executive Chairman purchased 70,000 shares for approximately £54,600 in December 2025. Despite relying solely on external borrowing for funding, the company anticipates a 17% annual earnings growth rate and continues to pay dividends without offering a scrip alternative.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com