The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 25 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

What Is Brown & Brown’s Investment Narrative?

To own Brown & Brown today, you have to believe in its ability to turn acquisitive scale into durable, cash‑generating brokerage earnings while keeping integration and balance sheet risks in check. The latest results largely support that story: revenue and net income rose to US$5.90 billion and US$1.05 billion, with higher adjusted earnings and a slightly higher dividend, even as the shares sold off on weaker organic growth and a small revenue miss. That reaction suggests the near term catalyst is less about dealmaking and more about convincing investors that underlying growth is intact once the largest‑ever Accession acquisition is fully absorbed. At the same time, the passing of the Chief Legal Officer introduces some governance and execution uncertainty, but the interim appointment and continued margin discipline suggest the immediate financial impact may be limited.

However, the market’s recent focus on organic growth trends is something investors should be watching closely.

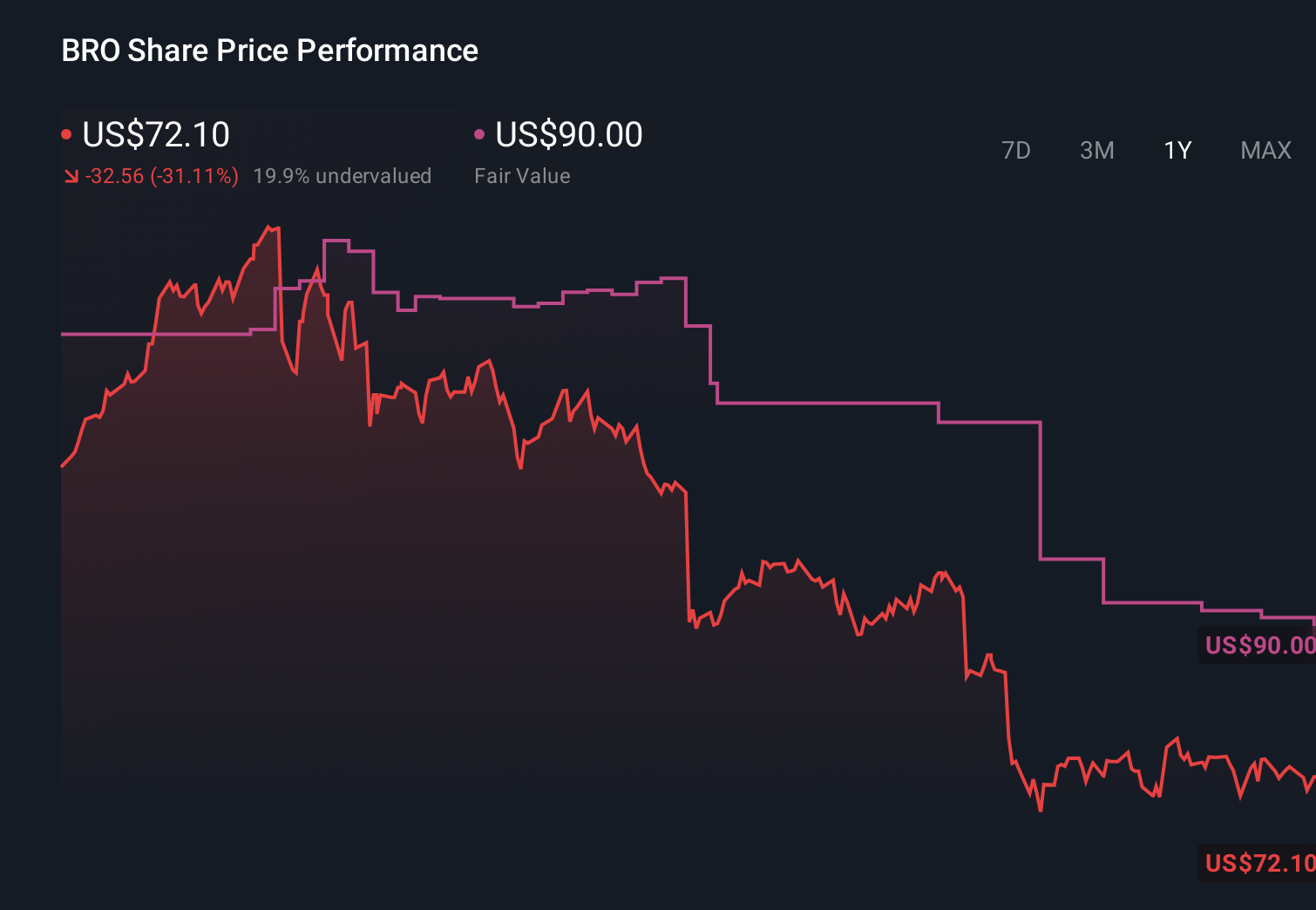

Despite retreating, Brown & Brown’s shares might still be trading 48% above their fair value. Discover the potential downside here.Exploring Other Perspectives BRO 1-Year Stock Price Chart Four Simply Wall St Community fair value views span roughly US$90 to US$138.72 per share, underscoring how differently investors read Brown & Brown’s prospects as organic growth concerns and integration risks move to the foreground.

BRO 1-Year Stock Price Chart Four Simply Wall St Community fair value views span roughly US$90 to US$138.72 per share, underscoring how differently investors read Brown & Brown’s prospects as organic growth concerns and integration risks move to the foreground.

Explore 4 other fair value estimates on Brown & Brown – why the stock might be worth as much as 92% more than the current price!

Build Your Own Brown & Brown Narrative

Disagree with this assessment? Create your own narrative in under 3 minutes – extraordinary investment returns rarely come from following the herd.

Looking For Alternative Opportunities?

Markets shift fast. These stocks won’t stay hidden for long. Get the list while it matters:

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Discover if Brown & Brown might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com