Despite an already strong run, LyondellBasell Industries N.V. (NYSE:LYB) shares have been powering on, with a gain of 25% in the last thirty days. Unfortunately, the gains of the last month did little to right the losses of the last year with the stock still down 26% over that time.

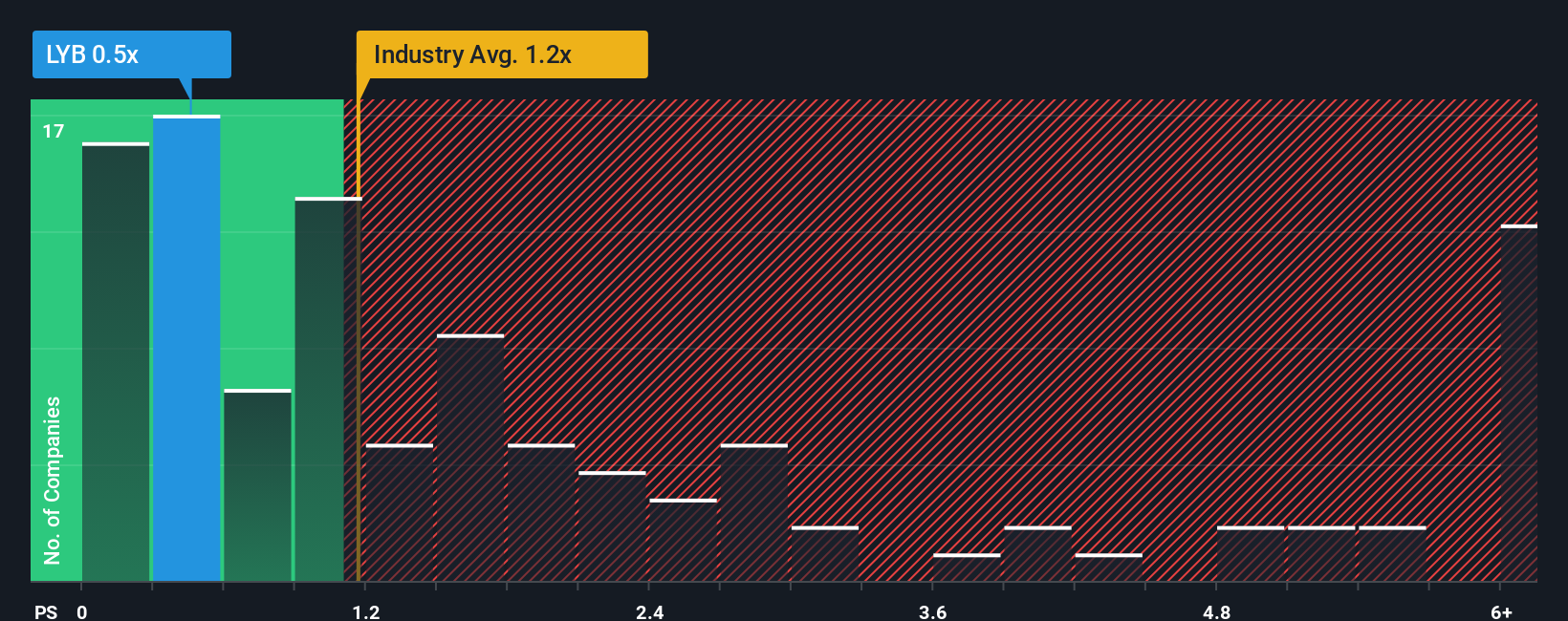

Although its price has surged higher, when close to half the companies operating in the United States’ Chemicals industry have price-to-sales ratios (or “P/S”) above 1.2x, you may still consider LyondellBasell Industries as an enticing stock to check out with its 0.5x P/S ratio. Nonetheless, we’d need to dig a little deeper to determine if there is a rational basis for the reduced P/S.

See our latest analysis for LyondellBasell Industries

NYSE:LYB Price to Sales Ratio vs Industry February 5th 2026 What Does LyondellBasell Industries’ P/S Mean For Shareholders?

NYSE:LYB Price to Sales Ratio vs Industry February 5th 2026 What Does LyondellBasell Industries’ P/S Mean For Shareholders?

With revenue growth that’s superior to most other companies of late, LyondellBasell Industries has been doing relatively well. One possibility is that the P/S ratio is low because investors think this strong revenue performance might be less impressive moving forward. If you like the company, you’d be hoping this isn’t the case so that you could potentially pick up some stock while it’s out of favour.

If you’d like to see what analysts are forecasting going forward, you should check out our free report on LyondellBasell Industries. What Are Revenue Growth Metrics Telling Us About The Low P/S?

There’s an inherent assumption that a company should underperform the industry for P/S ratios like LyondellBasell Industries’ to be considered reasonable.

Retrospectively, the last year delivered a decent 6.4% gain to the company’s revenues. Ultimately though, it couldn’t turn around the poor performance of the prior period, with revenue shrinking 29% in total over the last three years. Therefore, it’s fair to say the revenue growth recently has been undesirable for the company.

Looking ahead now, revenue is anticipated to slump, contracting by 7.2% per annum during the coming three years according to the analysts following the company. Meanwhile, the broader industry is forecast to expand by 8.7% per year, which paints a poor picture.

In light of this, it’s understandable that LyondellBasell Industries’ P/S would sit below the majority of other companies. However, shrinking revenues are unlikely to lead to a stable P/S over the longer term. Even just maintaining these prices could be difficult to achieve as the weak outlook is weighing down the shares.

What Does LyondellBasell Industries’ P/S Mean For Investors?

LyondellBasell Industries’ stock price has surged recently, but its but its P/S still remains modest. Typically, we’d caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

It’s clear to see that LyondellBasell Industries maintains its low P/S on the weakness of its forecast for sliding revenue, as expected. Right now shareholders are accepting the low P/S as they concede future revenue probably won’t provide any pleasant surprises. Unless these conditions improve, they will continue to form a barrier for the share price around these levels.

We don’t want to rain on the parade too much, but we did also find 2 warning signs for LyondellBasell Industries (1 is a bit concerning!) that you need to be mindful of.

If strong companies turning a profit tickle your fancy, then you’ll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.