Plains GP Holdings (PAGP) just reported its 2025 results, with Q4 adjusted EBITDA of $738 million and full year EBITDA of $2.833 billion, while outlining a shift toward a focused crude oil midstream business.

See our latest analysis for Plains GP Holdings.

The latest results and portfolio reshaping come after a strong run in the units, with a 30 day share price return of 8.05% and a 90 day share price return of 21.57%. The 5 year total shareholder return of 230.28% points to momentum that has built over a longer period.

If this update has you thinking about where else to put fresh capital to work, now could be a good time to look at 23 power grid technology and infrastructure stocks as a potential hunting ground for related infrastructure ideas.

With the units already up 21.57% over 90 days and trading around $22.54, the question now is whether Plains GP is still trading at a discount or if the market is already pricing in future growth.

Most Popular Narrative: 8.1% Overvalued

The most followed valuation work puts Plains GP Holdings’ fair value at $20.85 versus a last close of $22.54, so the units are trading above that narrative line in the sand.

The analysts have a consensus price target of $21.458 for Plains GP Holdings based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $26.0, and the most bearish reporting a price target of just $17.5.

Want to understand why a midstream operator with current losses still gets a premium valuation tag? The narrative leans heavily on future margin rebuild and a richer earnings multiple. Curious which revenue and earnings path needs to play out to make that math work?

Result: Fair Value of $20.85 (OVERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, the pivot to a pure crude oil focus and heavy Permian exposure could be detrimental if crude volumes soften or if contract renewals pressure margins and cash flow.

Find out about the key risks to this Plains GP Holdings narrative.

Another Take: Multiples Point the Other Way

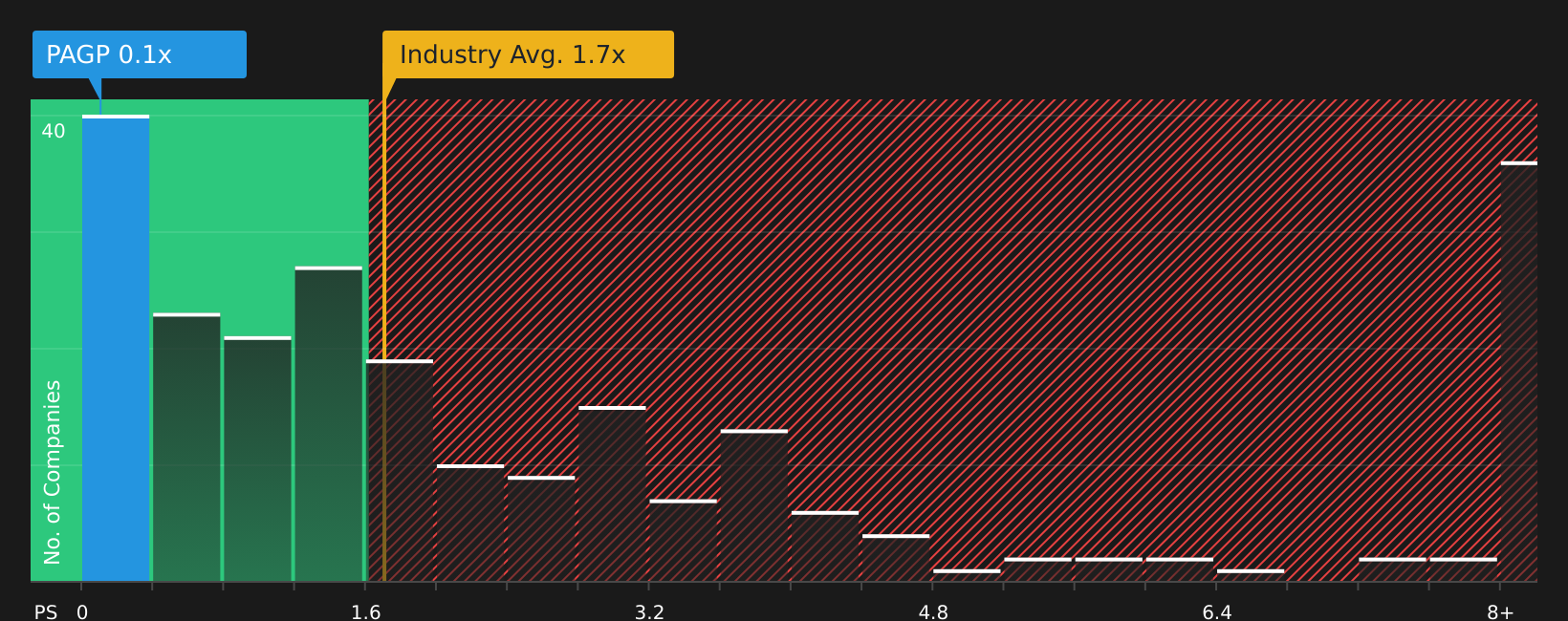

Those fair value models suggest Plains GP is about 8.1% overvalued at $22.54, but its P/S of 0.1x looks very low next to the US Oil and Gas industry at 1.7x, the peer average at 5.8x, and even a fair ratio of 0.6x. This hints at very different pricing risk and raises the question of where you land when the narratives disagree.

See what the numbers say about this price — find out in our valuation breakdown.

If the mixed signals here leave you on the fence, do not wait for consensus. Instead, weigh the data yourself and check the 3 key rewards and 2 important warning signs to round out your view.

Looking for more investment ideas?

If you stop here, you only see one corner of the market. Use the Simply Wall St Screener to quickly surface fresh ideas that match how you like to invest.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com