AI data centers, stubborn energy costs, and heightened geopolitical risk are all pushing reliable, carbon free power to the forefront of investment thinking. Nuclear sits at the center of that discussion, with governments, utilities, and large corporates all searching for 24/7 electricity that does not depend on weather or imported fossil fuels. Our Nuclear Renaissance screener is built to help you focus on listed companies most closely aligned with this long term trend. In this article, you will see three of the strongest candidates from that universe and the reasons they stand out at the moment.

Overview: Cameco is a Saskatoon based nuclear fuel company that supplies uranium and related services to power utilities, spanning mining, fuel refining and conversion, and a 49% stake in Westinghouse, a major nuclear reactor technology and services provider. Its operations cover the full nuclear fuel cycle, from extracting uranium concentrate through to supporting the operation and maintenance of commercial reactors worldwide.

Operations: Cameco generates CA$2.9b from Uranium, CA$0.6b from Fuel Services and CA$3.5b from Westinghouse (with offsetting unallocated adjustments), with revenue concentrated in Canada at roughly CA$3.0b and meaningful sales to the United States at about CA$0.4b.

Market Cap: CA$68.2b

Cameco sits at the heart of nuclear fuel supply at a time when utilities are signing long term contracts, such as the recent nine year, 22 million pound uranium deal with India worth roughly CA$2.6b. It also holds a meaningful stake in Westinghouse, which is tied to future reactor builds across the US, Europe and Asia. Earnings growth has been very strong and margins are currently in the mid teens, yet the very high P/E and reliance on external borrowing mean investors are paying a premium for that growth profile. The key issue is whether Cameco’s contracting pipeline, asset base and governance quality justify that premium, or if the risks around project delays and funding are being underestimated.

Cameco’s premium P/E and expanding nuclear footprint raise a simple question: is the market fully pricing in its contracting pipeline or missing something in the details of its earnings quality and leverage? Get the full picture in the analysis report for Cameco

TSX:CCO P/E Ratio as at Apr 2026 NANO Nuclear Energy (NNE)

TSX:CCO P/E Ratio as at Apr 2026 NANO Nuclear Energy (NNE)

Overview: NANO Nuclear Energy is a New York based developer of compact microreactors and related fuel cycle services, working on several small reactor concepts, including the KRONOS and LOKI microreactors, as well as ZEUS and ODIN designs, alongside plans for a high assay low enriched uranium fuel facility, transport solutions and consultancy for nuclear projects.

Market Cap: US$1.11b

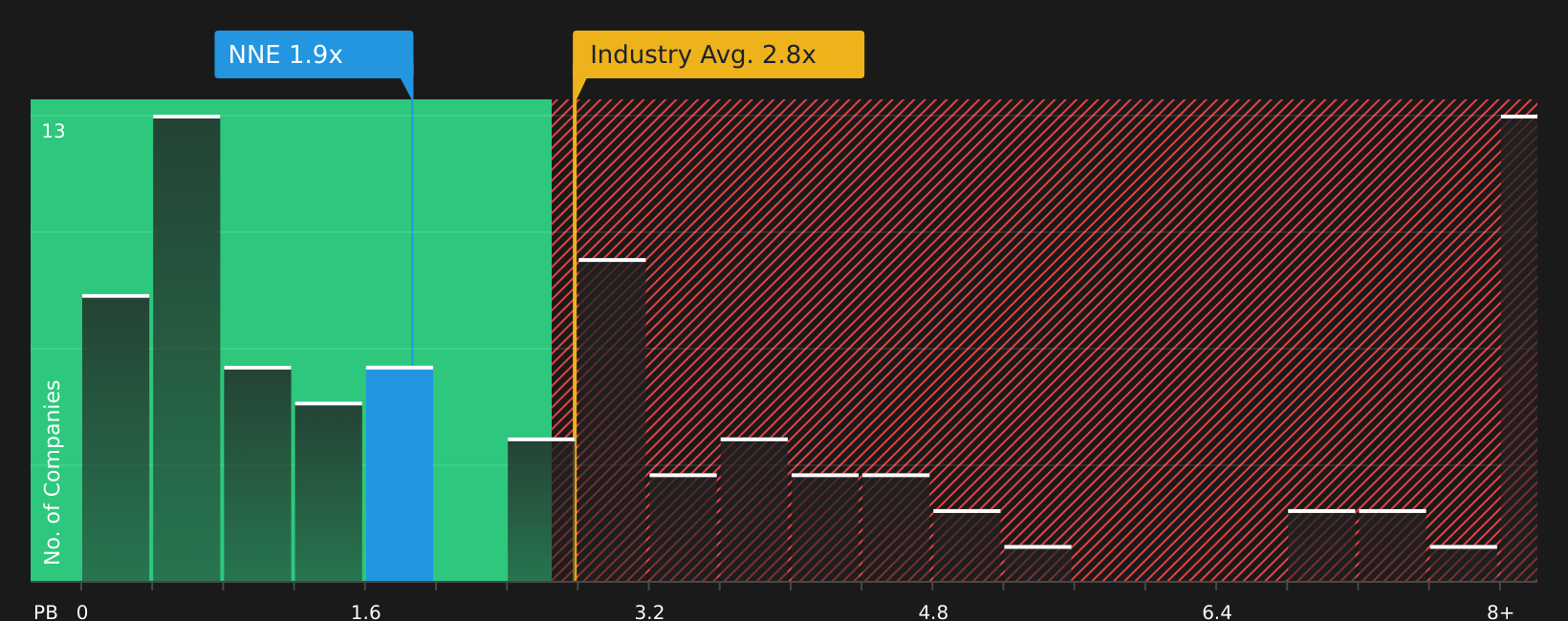

NANO Nuclear Energy brings together two themes that many investors are watching closely: AI driven power demand and the push to build a new nuclear supply chain. However, it is still pre revenue, loss making and heavily reliant on external funding and future share issuance. Recent milestones, such as submitting the construction permit application for the KRONOS microreactor with the University of Illinois and MOUs in the US, UAE and South Korea, indicate progress toward licensing and potential commercial projects. A sizeable cash position and a P/B ratio below peers provide some capacity to pursue those plans. On the other hand, long development timelines, high capital needs and ongoing losses mean execution risk is high and earnings visibility is limited, so this is a company where the details really matter.

Pre revenue microreactors, MOUs across three regions, and a sizable cash position are setting up a story that many may only be half seeing right now. To understand how those pieces fit together alongside the execution risks and funding needs that could change everything, read the analysis report for NANO Nuclear Energy

NasdaqCM:NNE P/B Ratio as at Apr 2026 GE Vernova (GEV)

NasdaqCM:NNE P/B Ratio as at Apr 2026 GE Vernova (GEV)

Overview: GE Vernova is a Cambridge, Massachusetts based energy company that provides equipment and services to generate, move, control, convert, and store electricity worldwide, spanning gas and nuclear power plants, wind turbines, and grid and software solutions that keep power systems stable and efficient.

Operations: GE Vernova generates about US$19.8b in revenue from Power, US$9.1b from Wind, and US$9.6b from Electrification, with small eliminations and other adjustments.

Market Cap: US$242.2b

GE Vernova sits at the intersection of electrification, decarbonization, and AI driven power demand, with a large installed base of gas and wind turbines feeding high margin service contracts and a growing grid and software business tied to a roughly US$150b backlog. Earnings and revenue growth have outpaced the wider market, but the shares trade on a rich P/E, and the Wind segment, tariff headwinds, and exposure to large, lumpy grid projects all introduce margin and execution risk. Combined with heavy use of external borrowing and some insider selling, this creates a complex mix of quality contracts, restructurings, and funding choices that may favor investors who focus closely on the underlying details rather than only the headlines.

GE Vernova’s mix of high margin service contracts, a roughly US$150b backlog, and a rich P/E suggests something in the story is decoupling from the headlines; the analysis report for GE Vernova hints at what could change that perception.

NYSE:GEV P/E Ratio as at Apr 2026

NYSE:GEV P/E Ratio as at Apr 2026

The three companies in this article are just a starting point, with the full Nuclear Renaissance screener surfacing 90 more nuclear infrastructure names that each come with their own potential catalysts and narratives around AI data centers and decarbonization. Use Simply Wall St to unlock, identify, and analyze the specific contract pipelines, balance sheet strength, and project milestones that matter to you so you can focus on the highest conviction ideas in this theme.

Take Control of Your Investment Journey

If NANO Nuclear Energy or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your top picks to a Watchlist to monitor the share price against the fair value for the ideal entry point.

Once you’ve made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates.

Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives.

By uncovering hidden catalysts and risks early, you’ll accelerate your decision-making and stay one step ahead of the market.

Seeking Alternatives Before The Crowd?

Fresh ideas do not stay under the radar for long, and momentum often shifts fast as breakouts form and stories get caught by the crowd. Consider acting before that happens.

Spot cash flow strength early by scanning the 8 high quality undervalued stocks before earnings surprise others and potential entry points start dropping out of reach. Ride powerful income streams by zeroing in on the 6 dividend fortresses while yields and fundamentals still line up for long term payout potential. Get ahead of the next automation wave by filtering the 33 robotics and automation stocks while these opportunities are still flying under wider market attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Discover if NANO Nuclear Energy might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com