If the current state of the world economy is marked by stark cognitive dissonance, if what is not sustainable cannot be sustained, then what comes next?

One answer was given at the weekend in a piece in the FT by Gita Gopinath who recently returned to Harvard after stints as first deputy managing director and chief economist of the IMF:

Policymakers would do well to use this period in which stock markets seem disconnected from heightened risk to craft a new playbook for crisis support that is both fiscally sustainable and supportive of long-term growth. The experiences of the pandemic and Ukraine war provide a valuable lesson in what that should look like: support targeted to the vulnerable; bailouts only to companies that are liquidity constrained but otherwise viable ŌĆö and whose failure poses systemic risks; and co-ordinated fiscal and monetary policy so they do not work at cross-purposes. If a new course is not charted, governments constrained by fiscal space may rely on heterodox measures, including broad-based price controls, financial repression, nationalisations, and pressure on central banks to absorb fiscal risk. None of this would be good for the economy with synchronised sell-offs across stocks and bonds as markets realise that the backstop they were counting on is no longer there.

Yesterday I read Gopinath in terms of the pervasive cognitive dissonance of our current moment. Today I want to draw attention to GopinathŌĆÖs terse denouement. To repeat:

If a new course is not charted, governments constrained by fiscal space may rely on heterodox measures, including broad-based price controls, financial repression, nationalisations, and pressure on central banks to absorb fiscal risk.

What Gopinath sees as being at risk are the last guard rails of what used to be called the ŌĆ£Washington consensusŌĆØ. But should we be anathematizing these options, or embracing them?

I am encouraged to return to GopinathŌĆÖs op ed by this tweet by macrofinance comrade Daniela Gabor. Daniela, too, highlights GopinathŌĆÖs final warning.

As Daniela asks: against the backdrop of our current disorder, what is the alternative What is the scenario?

Say we are in a new age of ŌĆ£polycrisisŌĆØ or ŌĆ£permanent crisisŌĆØ (Meadway), or ŌĆ£overlapping emergenciesŌĆØ (Weber et al) compounded by the disintegration of US hegemony. In other words it is not by accident that we face shock after shock – COVID, Ukraine, Straits of Hormuz etc etc.

Say that, in the face of such crises, centrist politicians are driven, against their will, to the realization that such shocks can only be managed by large-scale and coordinated monetary and fiscal policy of the kind argued for by ŌĆ£heterodoxŌĆØ left-Keynesians (the argument of my book, Shutdown). It is not by accident, therefore, that debts are rising in stepwise shocks.

Say that centrist politicians believe they have no alternative to such experimentation, not because they actually embrace the radical political potential of such policies, but because they are threatened by the rise of right-wing populism and feel they need to ŌĆ£do somethingŌĆØ.

But assume also, that they lack any real agenda of progressive politics. At the first whiff of trouble they retreat to ŌĆ£fiscal rulesŌĆØ and subservience to conservative central bankers. Then, in political terms, we will be caught in the nasty charade of reformism that is epitomized by the UKŌĆÖs government under PM Keir Starmer.

To make matters worse, as Gopinath argues, the financial markets will likely begin to anticipate such policy reactions and the markets will consequently become increasingly blind to mounting systemic risks. An additional measure of financial risk will then be overlayed on top of the emergencies of the polycrisis and the blowback from the meltdown of US hegemony.

This sequence of crisis & crisis-management – emergency intervention & recovery – recovery & half-hearted retrenchment can continue for a while. But, increasingly, governments when facing the next shock and the next round of rescue measures will face fiscal constraints. This at least is what Gopinath imagines. Alarmists may argued that the UK is rapidly approaching that point. The ŌĆ£moron premiumŌĆØ doesnŌĆÖt help.

So what now? A retreat to inaction is not an option. History wonŌĆÖt allow it. You might imagine, therefore, that anyone thinking constructively would begin to consider other forms of crisis-management that do not involved loading up the public balance sheet with more liabilities.

The main options are precisely those that Gopinath lists:

Price controls to prevent opportunistic profit-taking and gouging.

Nationalization to ensure investment and capital discipline.

Coordinated action by central banks and treasuries to ensure that expanded borrowing can be met without bond market panic.

Financial repression – negative real interest rates – to ensure that the financial legacy burden is distributed in a socially acceptable way.

But that, of course, is not GopinathŌĆÖs point. She is worried. Her last line is somewhat ambiguous. ŌĆ£None of this would be good for the economy ŌĆ” ŌĆ£. Why it would be bad news, she never spells out. In fact, of course, it depends. It depends on the setting and how the specific policies are implemented.

But what Gopinath actually focuses on is the question of expectations:

None of this would be good for the economy with synchronised sell-offs across stocks and bonds as markets realise that the backstop they were counting on is no longer there.

So the most urgent problem as far as Gopinath is concerned is the one that she started with: cognitive dissonance. Financial markets are priced for the continuation of a generous and ad hoc crisis-management regime. If you follow GopinathŌĆÖs argument and the urgings of those of us in the progressive camp, this regime cannot long continue. The risk is that when the penny drops, we are in for a nasty financial-market shock. Simultaneous selling of stocks and bonds, the unhinging of the marketŌĆÖs own balancing system, would be bad news.

The answer from the left is presumably ŌĆ£prepare, prepare, prepareŌĆØ. The crisis management and the political constraints under which it must be conducted are not of our own choosing. It is a matter of realism to acknowledge the challenges ahead and to consider all the possible policy options. One cannot expect financial markets to welcome such a horizon. But nor would they actually want governments that simply ignored emergencies and let crises unfold. And it is unclear whether they would actually welcome a serious effort at fiscal consolidation. Did the eurozone prosper in the 2010s? Hardly! If anyone has a better idea for redressing the current fiscal imbalances than a sustained dose of financial repression (with inflation settling at 3 percent or more and financial regulations in place to prevent avoidance), let them make the case. In a world of second- and third-bests, you have to be willing to consider every option.

Perhaps this is a moment to return to the discussion five or six years ago to which Gopinath herself was a contributor, in which analysts associated with the IMF and the BIS attempted to lay out a new integrated framework for monetary, exchange rate, and financial stability policy. What the IMF and the BIS were then trying to come to terms with was the ramifying impact of the 2008 crisis and its aftermath. The shock to financial stability from the US and Europe and the ensuing wave of central bank intervention (QE) had left major emerging markets facing volatile capital flows. hey had responded creatively and effectively by stretching the boundaries of the Washington consensus. They adopted previously anathematized heterodox policy measures to respond both to immediate shocks and persistent structural features of the dollar system. And the response of the IMF and the BIS was, somewhat surprisingly, to embrace this reality and to seek to rationalize it.

As Claudio Borio put it in June 2019 for the BIS:

Emerging market economies (EMEs) have adopted inflation targeting but combined it with FX intervention rather than free floating – in contrast to what standard textbooks would prescribe. Practice has moved ahead of theory. Moreover, EMEs have complemented such monetary frameworks with macroprudential measures. The choice reflects EMEs’ high sensitivity to capital flows and exchange rate fluctuations. This gives rise to potential policy trade-offs: it can make it harder to stabilise output and inflation at the same time and to reconcile macroeconomic stability today with macroeconomic stability tomorrow. FX intervention and macroprudential measures can improve these trade-offs. The frameworks have served EMEs well, although more work is needed to put the frameworks on a stronger analytical basis and to develop their implementation. The direction of travel is clear. And theory needs to catch up.

In 2020, Gopinath and her co-authors doubled down:

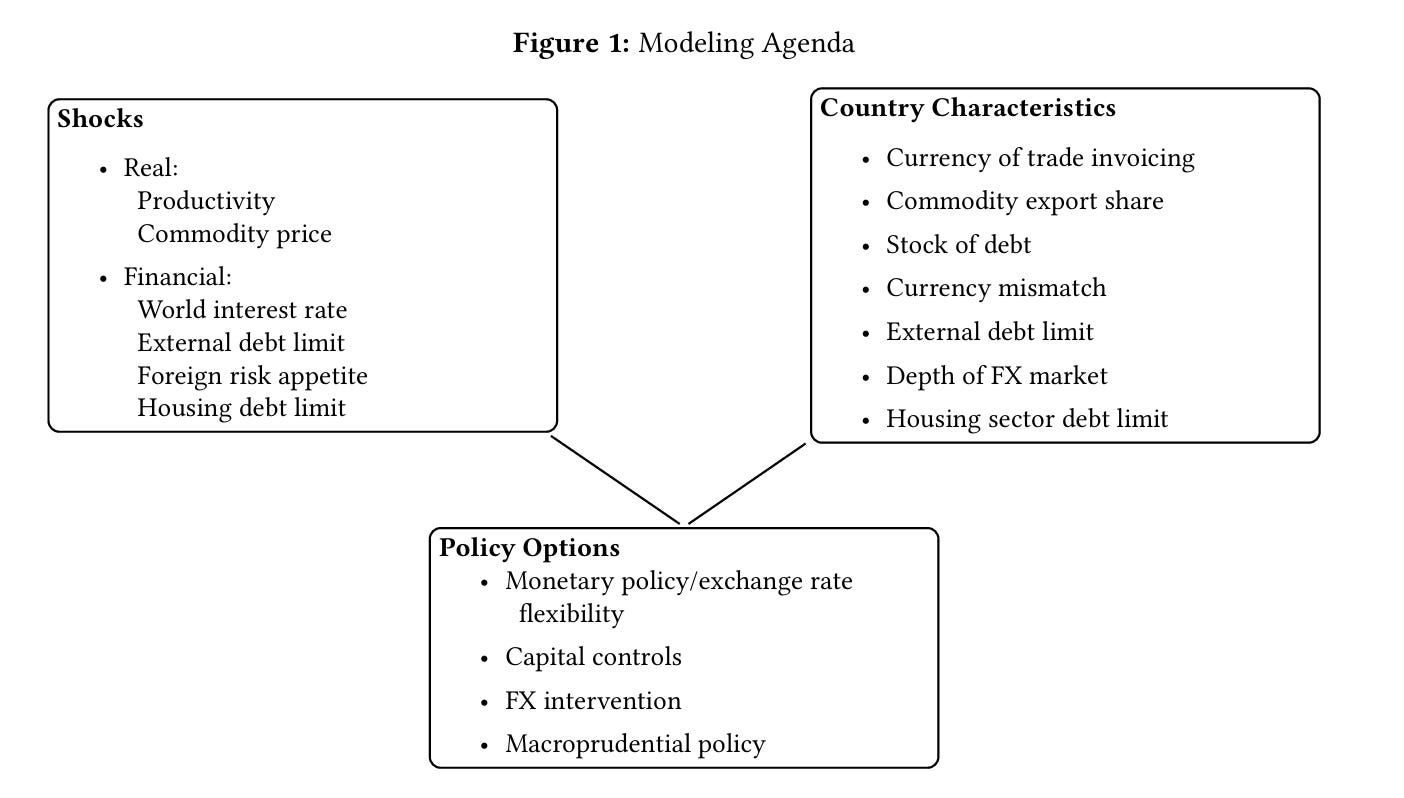

Our work is motivated by two observations. First, the empirical evidence is inconsistent with some of the assumptions underlying the Mundell-Fleming framework regarding both trade and finance. Many emerging markets have dollar invoicing shares above 80 percent. This empirical fact implies that we need to consider a dominant currency pricing paradigm where export prices are sticky in a dominant currency, which is most often the dollar and in some cases the euro. Similarly, on the financial side, a vast literature establishes an array of imperfections in international and domestic capital markets. Foreign currency borrowing is prevalent, and generates a link between the exchange rate and the macroeconomy through currency mismatches and external borrowing constraints. Financial intermediaries operating in foreign exchange markets generally have limited appetite for taking on emerging marketsŌĆÖ currency exposure and hence, the uncovered interest parity condition breaks down. Those countries which intervene heavily in foreign exchange markets during depreciation episodes tend to be the countries where balance sheet concerns prevail, and where financial markets are not deep enough to provide hedging opportunities. In addition, imperfections in domestic financial markets, particularly in the housing sector, are well-established for both emerging and advanced markets. The second observation is that many small open economies adopt more eclectic approaches than standard interest rate seŌĆ╣ing and ŲÆloating exchange rates to cope with shocks. For example, during the ongoing COVID-19 epidemic, many emerging markets faced capital outŲÆlow pressures and used multiple tools to achieve macroeconomic stabilization, with some variation across countries. While most countries lowered policy rates and eased macroprudential regulation, some complemented it with sales of foreign exchange reserves to lean against the depreciation. At the same time, a few countries relaxed their restrictions on capital inŲÆlows. Given their frequent and often heterogeneous use, one of the objectives of this paper is to better understand these alternative tools: what they do, how they interact, the trade-offs involved, and the characterization of policy counterfactuals. In other words, this paper aims to establish under what conditions the standard prescription of ŲÆlexible exchange rates still holds, and when it may instead be optimal to rely on other tools. Doing so requires going beyond the Mundell-Fleming framework. the novelty of our analysis is that we develop an integrated model that jointly considers the role of monetary policy, capital controls, foreign exchange intervention, and macroprudential regulation in small open economies.1 We characterize the use of these policy instruments as a function of shocks and both real and nominal frictions. ŌĆ” the objective of our analysis is then to map the combinations of shocks and country characteristics to the optimal policy mix, listed in the box at the boŌĆ╣om of the diagram.

Or as Gopinath and her co-authors put it in an accompanying blog post:

ŌĆ£Our analysis suggests that there is no ŌĆ£one-size-fits-allŌĆØ response to capital flow volatility, nor is it a case of ŌĆ£anything goesŌĆØ or that all policies are equally effective.ŌĆØ

This is the pragmatic spirit with which we should also approach our current moment.

Personally, I am hesitant about price controls. I can see a role for targeted nationalization, or at least the thresat of such measures. I see no good alternative to both financial repression and increased central bank-treasury coordination. Others may disagree. In any case, this is not a moment to give preemptive obedience to the diktat of financial markets or to anathematize the ŌĆ£Four Horsemen of HeterodoxyŌĆØ. This is a moment for constructive and empirical analysis to figure out what combination of policies offers the best chance of conducting progressive and democratic economic policy in the face of huge shocks repeatedly impacting the world economy.

I love writing the newsletter. If you enjoy it too and fancy buying me a coffee once a month, you know what to do. Click below!