This commentary represents the research and views of the authors. It does not necessarily represent the views of the Center on Global Energy Policy. The piece may be subject to further revision. The Center on Global Energy Policy would like to thank the Bernard & Anne Spitzer Charitable Trust for its grant to CGEP in support of research related to nuclear energy. More information is available at Our Partners.

In March, the European Commission proposed the Industrial Accelerator Act (IAA) to promote low-carbon manufacturing, diversify supply chains, and boost the competitiveness of EU industry.

The IAA would introduce local content and carbon intensity requirements in procurement, establish a pre-approval regime for foreign direct investment in strategic manufacturing, and streamline permitting for industrial decarbonization projects.

The proposal’s preference for European producers and selected EU trading partners reflects a broader defensive turn in EU economic engagement driven by dysfunction in the multilateral trade system and growing concerns about a surging trade deficit with China.

In early March 2026, the European Commission (EC) published a proposal for the Industrial Accelerator Act (IAA),[i] a wide-ranging regulation that would introduce local content and carbon intensity requirements in procurement and other public expenditures, establish a pre-approval regime for large foreign investments in strategic manufacturing sectors, and streamline permitting for industrial decarbonization projects across the European Union. If passed, the IAA would represent the EU’s most ambitious industrial policy since the European Green Deal, reflecting both a commitment to a low-carbon future and intensifying concerns about European competitiveness and supply chain resilience. The draft regulation’s preference for European producers and selected EU trading partners constitutes a softening of Brussels’ position on market neutrality—a shift that reflects a broader defensive turn in EU economic engagement driven by dysfunction in the multilateral trade system and concerns about a surging trade deficit with China.[ii]

This commentary unpacks the IAA’s core provisions, examines its implications for third countries, and identifies the open questions most likely to shape its final form and practical effect.

Background

Relative to other leading economies, the EU has made limited use of fiscal incentives to shape industrial outcomes and structure supply chains since the end of the Cold War. The EU’s state aid rules, World Trade Organization (WTO) commitments, and decentralized allocation of trade, tax, and procurement authority across institutional actors have constrained its ability to pursue broad industrial policies on the scale of the Inflation Reduction Act (IRA) or Made in China 2025.

These constraints have come under increasing pressure in recent years. Russia’s invasion of Ukraine in 2022 exposed Europe’s dependence on imported fossil fuels and sent electricity prices soaring. Concurrent with the energy crisis in Europe, the United States passed the IRA, which authorized immense subsidies to the US energy and transportation sectors, further widening the gap between European and American costs of production.[iii] The crisis also coincided with a dramatic erosion of multilateral trade norms, driven by the United States’ unapologetic use of tariffs.[iv]

This confluence of economic headwinds has fueled anxieties in Europe about the EU’s industrial vitality. In response, EC President Ursula von der Leyen commissioned a report on European competitiveness from former European Central Bank President Mario Draghi.[v] The report, released in 2024, characterized Europe’s stalling economic growth as an “existential challenge” and called for a new industrial strategy based on massive investment and a more strategic use of trade policy to build resilient supply chains, reduce dependencies, and accelerate technological progress. This assessment strengthened an emerging consensus in Brussels that interventionist policies were necessary to secure the continent’s economic future.

The IAA is the EC’s most comprehensive response yet to the Draghi Report. It seeks to leverage some of Brussels’ most powerful economic instruments—procurement, market access, and energy regulation—to direct investment toward strategic sectors and technologies and to ensure that Europe’s energy transition does not undermine its technological innovation and economic resilience.

What the IAA Proposal Would Do

The IAA’s overarching objective is to strengthen the EU manufacturing sector’s competitiveness and resilience in support of European climate objectives. Specifically, it sets a goal for European manufacturing to account for at least 20 percent of EU GDP by 2035, compared to 14 percent in 2024.[vi] The regulation pursues this goal through four main instruments: local content and greenhouse gas intensity requirements, investment conditionality, permitting reform, and the designation industrial zones.

Local content, emissions intensity, and national security requirements for net-zero technologies and industrial goods

The most commercially significant of these instruments is a set of local content and low-carbon requirements applicable to products containing steel, aluminum, concrete, and mortar intended for use in buildings, infrastructure, and motor vehicles. These requirements would apply to both public procurement (i.e., government purchases, leases, and rentals) of those products and buildings and infrastructure construction projects that receive state support.

To meet the requirements, a specified share of the covered products being procured or used in construction must be “low carbon”[vii] and of “Union origin.”[viii] The IAA defines “low carbon” as goods that meet standards set out in the Ecodesign for Sustainable Products Regulation (2024) and the Construction Products Regulation (2024). It defines “Union origin” to include both European-made goods and those made in countries with which the EU has an FTA or a customs union agreement. In procurement contexts, the category also includes goods from countries that are party to the WTO Agreement on Government Procurement (GPA). The requirements differ by material: steel is subject to a low-carbon threshold, but not to origin conditions; concrete and mortar must meet a 5 percent low-carbon content threshold and be of Union origin; and aluminum must meet a 25 percent Union-origin and low-carbon requirement.

Alongside these new rules for energy-intensive commodities, the IAA includes Union-origin requirements and supply chain deconcentration measures for net-zero technologies. Most notably, the regulation would require that public procurement of electric vehicles (EVs) and consumer subsidies for EVs be limited to Union-origin vehicles. It would also impose Union-origin requirements on procurement of solar, wind, hydrogen, and battery energy storage systems products.

Finally, the IAA would build on the Net-Zero Industrial Act of 2024 (NZIA), which mandates the use of non-price criteria in public procurement and auctions relating to net-zero technologies. These criteria include sustainability and supply chain resilience, with the latter defined to encompass situations where a non-EU country accounts for more than 50 percent of a given technology in the European market. The IAA would further require that at least 40 percent of a member state’s auctions of such technologies meet the NZIA’s resilience and sustainability requirements.

These requirements are not unconditional. Authorities can set them aside where no compliant product is available, where meeting them would cause significant delays, or where the cheapest compliant option is more than 25 percent more expensive than the alternative in procurement or adds more than 30 percent to product costs in support schemes.[ix] Such opt-out thresholds are significant given current market conditions: Chinese producers enjoy structural advantages in sectors such as solar and batteries and the cost differential between Chinese and domestic alternatives is likely to fall within the opt-out band for many covered products.

In addition to these Union-origin and low-carbon provisions, the IAA would introduce a restrictive cybersecurity requirement applicable to certain technologies. For auctions and procurement involving net-zero technologies with control, supervisory control and data acquisition (SCADA), or remote access systems, suppliers identified as “high risk” under the EU’s forthcoming revised Cybersecurity Act are fully excluded.[x] That exclusion applies to 100 percent of relevant auction volume, not just the 40 percent or 8 gigawatt floor that governs the Union-origin requirements.[xi] Unlike the regulation’s Union-origin and low-carbon requirements, there is no cost opt-out available.

The application of these requirements to third-country suppliers depends on both the type of public intervention and the EU’s trade relationship with the supplier’s home country. In public procurement, the GPA[xii] provides a route to equivalence: suppliers from GPA member countries are treated as equivalent to EU producers. However, in renewable energy auctions and support schemes, equivalence is limited to countries that have free trade agreements (FTAs) with the EU.[xiii] This creates a two-tier system: GPA membership provides market access for procurement but not auctions, which account for nearly 60 percent of expected global utility-scale renewable capacity growth through 2030, according to the IEA.[xiv] Additionally, companies manufacturing in an EU-friendly country can still be excluded if they are ultimately owned by entities based in countries without a qualifying agreement.

Investment screening tools

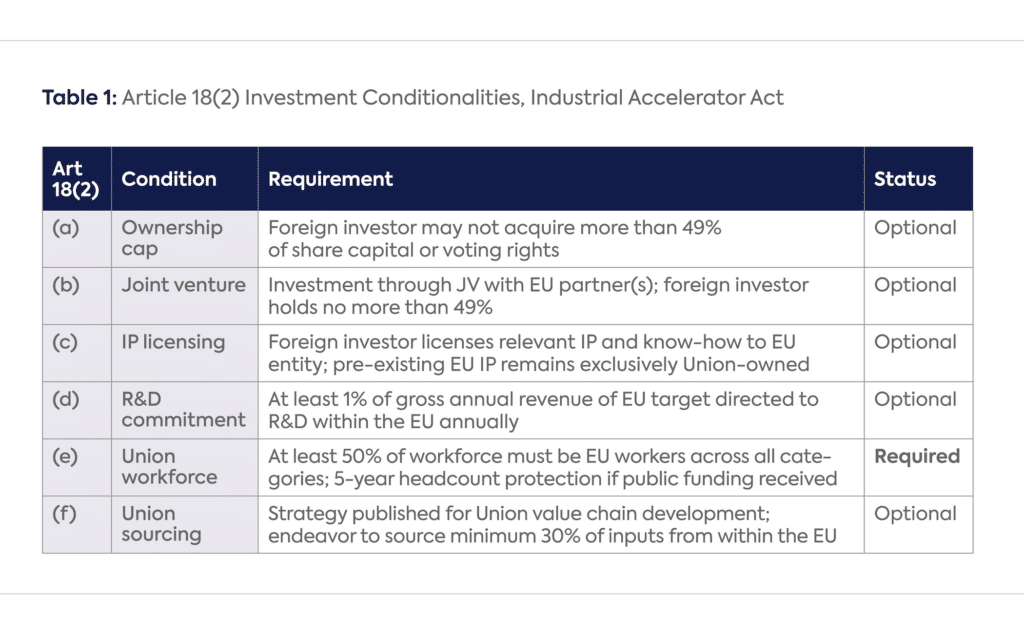

The IAA also introduces a new pre-approval requirement for foreign investments above 100 million euros in sectors where the investor’s home country holds more than 40 percent of global manufacturing capacity.[xv] The proposal identifies four strategic manufacturing sectors: batteries and energy storage systems; electric vehicles; solar technologies; and critical minerals. To gain approval, investors must satisfy at least four of six conditions laid out in Table 1. The framework is designed to ensure that qualifying investments generate meaningful positive spillovers within the EU, rather than maintaining operational and technological capacity with a foreign parent.

Lastly, the regulation addresses two structural constraints on industrial investment that operate before any such commercial conditions arise. A reformed permitting regime, building on procedures originally established under the NZIA, would streamline approvals for a broad range of industrial decarbonization projects, reducing the administrative burden associated with creating and updating national facilities. Member states would also be required to designate an industrial acceleration area within twelve months of the regulation entering into force, with projects inside those zones benefiting from area-level environmental assessments and coordinated infrastructure planning.

The Elephant in the Room

The IAA’s investment conditionality regime is framed neutrally and without reference to individual countries. However, the trigger, a 40 percent global manufacturing capacity threshold, currently applies only to China across all four covered sectors.[xvi] Combined with the equivalence architecture described above, China’s position vis-à-vis the IAA is singular: it is neither a GPA party nor an EU FTA partner. As a result, Chinese suppliers face full Union-origin requirements across all intervention types, and Chinese investors face the conditionality regime without any exemptions.

Chinese producers could likewise be adversely affected by the IAA’s proposed amendments to the NZIA’s framework for evaluating tenders in public procurement and auctions. China dominates many of the technologies that would fall within the NZIA’s amended scope. As a result, bidders in European auctions and procurement tenders could face harsher scoring criteria or even disqualification if they propose to sell or deploy covered Chinese technologies.

Unsurprisingly, Chinese officials have voiced strong opposition to these and other aspects of the IAA. China’s Ministry of Commerce (MOFCOM) expressed “serious concerns” and warned it would pursue “countermeasures” if Brussels moves forward with the regulation.[xvii] MOFCOM identified the regulation’s mandatory technology transfers, local content requirements, and equity limits for third-country investors as potentially violating WTO commitments and destabilizing global supply chains, warning that the regulation creates “serious investment barriers and systemic discrimination.”[xviii] In response, EU Trade Commissioner Maroš Šefčovič pledged to “fight tooth and nail for every European job, for every European company, for every open sector.”[xix]

What to Watch

In order to become law, EC proposals must be reviewed and approved by the European Parliament and Council of the European Union, a process that usually results in substantial revisions to draft texts. As the IAA moves through this process, several areas are likely to be the focus of negotiations.

First, the inclusion of FTA and customs union partners and GPA parties in the preference schemes under the IAA may raise concerns that the regulation is insufficiently attuned to the needs and challenges of European industry. The EU has trade agreements with approximately 70 countries covering many of its major trading partners and is actively pursuing FTA negotiations with other large economies. This vast and expanding network may limit the IAA’s effectiveness as a tool to strengthen European competitiveness.

Second, the IAA’s investment conditionality rules may be viewed as too permissive by some European industrial and labor interests. Investor flexibility in meeting three of the five non-mandatory requirements under the regulation could result in an expanded foreign investment footprint in Europe’s industrial sector without substantial technology transfer or supply chain localization—particularly with respect to upstream inputs.

Third, the regulation’s expectation that foreign producers comply with EU standards and reporting requirements to qualify as “low carbon” may aggravate tensions about compliance costs precipitated by other trade and industrial policies such as the Carbon Border Adjustment Mechanism (CBAM) and Regulation on Deforestation-free products (EUDR). Many EU trading partners, particularly developing countries, have criticized the CBAM and EUDR as de facto protectionist, arguing that they condition access to the European market on onerous sustainability standards that are not well aligned with the economic realities of non-European economic and regulatory systems.[xx] For similar reasons, the IAA could be perceived as privileging EU-based firms and those of other advanced economies at the expense of the Global South.

Fourth, the regulation will undoubtedly raise concerns about inflation given current energy prices. Local content and emissions intensity requirements can increase input costs. Although the IAA includes opt-out provisions for situations where Union-origin products would be more expensive, those are set at thresholds that some producers may view as too high. A 20 percent increase in the cost of steel, for example, would not justify the opt-out provisions but could nonetheless significantly raise production costs.

Finally, the regulation’s consistency with multilateral trade norms is likely to face scrutiny. Local content requirements are generally disallowed under WTO rules, including in renewable energy contexts. A key question will be whether auctions to deploy net-zero technologies fall within the scope of the GPA or under exceptions in the Global Agreement on Tariffs and Trade and other WTO agreements. Existing trade jurisprudence does not provide clear guidance on this, and without further clarification the IAA is likely to be contested by one of Brussels’ non-FTA trading partners at the WTO.

Conclusion

The IAA reflects an emerging consensus in Brussels that carbon pricing and emissions standards, which have long been EU officials’ preferred decarbonization tools, may be insufficient to secure European industrial interests in a world where major competitors aggressively deploy fiscal and trade measures. As the IAA moves through the EU legislative process, European leaders will need to decide how much they are willing to intervene in the common market to safeguard the continent’s economic future.

About the Authors

Trevor Sutton, a Senior Research Associate at CGEP, focuses on the intersection of trade, climate, and industrial policy and leads the center’s Program on Trade and the Clean Energy Transition. Trevor previously served as Research Director of the Remaking Global Trade for a Sustainable Future Project and was a co-author of a seminar report on trade system reform, the Villars Framework for a Sustainable Trade System. He has also served in various roles at the Center for American Progress, most recently as a Senior Fellow for Energy and Environment, and the United Nations. Prior to these positions, Trevor served as a judicial clerk on the U.S. Court of Appeals for the District of Columbia Circuit. Trevor has a BA from Stanford University, a JD from Yale Law School, and an MPhil from Oxford University, where he was a Marshall Scholar.

Evelyne Williams is a Research Associate at Center on Global Energy Policy at Columbia University SIPA, where she focuses on the intersection of international trade, energy, and decarbonization. She most recently served as a Foreign Affairs Officer in the U.S. Department of State’s Office of Global Change, where she was the deputy lead negotiator on carbon pricing at the International Maritime Organization (IMO) and represented the United States in international climate negotiations under the UN Framework Convention on Climate Change (UNFCCC) and the Organisation for Economic Co-operation and Development (OECD).

A recipient of the State Department’s Colin Powell Leadership Program fellowship for emerging policy leaders, Evelyne also held roles at the U.S. Mission to the United Nations in New York, the Office of the Geographer and Global Issues, and the Humanitarian Information Unit, where she contributed to socio-economic and climate-related policy initiatives.

Raised in Puerto Rico and the U.S. Virgin Islands, Evelyne has a longstanding interest in island economies, economic policy, and climate resilience. As a student at Columbia, she led a property tax reform and infrastructure resilience initiative in Puerto Rico and collaborated on the development of a graduate course on international monetary policy with Professor Richard Clarida. Earlier in her career, she interned at the U.S. Department of Commerce’s International Trade Administration, supporting export strategies for U.S. firms.

Evelyne holds a Bachelor of Arts in Economics with Distinction from Barnard College, Columbia University, and has pursued a Master of International Affairs at Columbia’s School of International and Public Affairs.

Swad Sathe is a Research Associate at the Center on Global Energy Policy at Columbia University SIPA, where he focuses on researching the nexus between trade and energy. He also provides operational support, including project management and strategic communications, for the Trade and Clean Energy Transition Initiative. He most recently was a Climate Intern at the Niskanen Center in Washington D.C., where he conducted research and wrote articles on permitting reform, transmission expansion, and geothermal energy.

A master’s graduate in International Affairs from the George Washington University, Swad specialized in energy and environmental policy, which culminated in a capstone project on incorporating critical minerals into the USMCA. While in D.C., he also had internships with Observer Research Foundation America, a think tank specializing in U.S. – India relations, and the Climate Leadership Council, a think tank focused on market-based solutions to reduce global emissions.

Swad has a background in fintech, having worked at Sezzle, an alternate payments platform, for over four years. He led Strategic Partnerships at the Minneapolis-based startup, where he forged relationships with over 100 technology and platform partners, expanding the company’s presence in the eCommerce space. He also led CSR efforts, including Sezzle’s B Corp recertification process.

Swad also holds a Bachelor of Science in Economics from the University of Minnesota – Twin-Cities.

[i] European Commission, “Proposal for a Regulation of the European Parliament and of the Council on Establishing a Framework of Measures for Accelerating Industrial Capacity and Decarbonisation in Strategic Sectors (Industrial Accelerator Act),” COM(2026) 100 final, 2026/0068 (COD) (Brussels, March 4, 2026).

[ii] Carlo Martsucelli, “Europe-China Trade Deficit Widens,” Politico Europe, February 13, 2026, https://www.politico.eu/article/europe-china-trade-deficit-widens/;

DRM News, “Macron Warns China Is ‘Destroying European Industry’ without Strong EU Protection,” YouTube video, April 24, 2026, https://www.youtube.com/watch?v=zKTj5999BvY.

[iii] Inflation Reduction Act of 2022, Pub. L. 117-169, 117th Cong., 2nd sess. (August 16, 2022), https://www.congress.gov/bill/117th-congress/house-bill/5376/text; International Energy Agency, Energy Technology Perspectives 2024 (Paris: IEA, 2024), https://www.iea.org/reports/energy-technology-perspectives-2024.

[iv] Casey Crownhart, “China’s Energy Dominance in Three Charts,” MIT Technology Review, July 10, 2025, https://www.technologyreview.com/2025/07/10/1119941/china-energy-dominance-three-charts/; International Energy Agency, Energy Technology Perspectives 2024, chap. 6, https://www.iea.org/reports/energy-technology-perspectives-2024.

[v] Mario Draghi, The Future of European Competitiveness (Brussels: European Commission, September 2024), https://commission.europa.eu/topics/competitiveness/draghi-report_en.

[vi] World Bank, “Manufacturing, Value Added (% of GDP) — European Union,” World Development Indicators, accessed April 2026, https://data.worldbank.org/indicator/NV.IND.MANF.ZS?locations=EU.

[vii] Steel products are subject only to a low-carbon content requirement. The other covered goods are subject to both a low-carbon content and a Union-origin content requirement.

[viii] “Union origin” is a legal term relating to the national source of a product as determined under applicable EU regulations and trade agreements. Somewhat confusingly, it can be defined to include goods that are produced outside the European Union, as is the case under the IAA.

[ix] European Commission, “Proposal for a Regulation of the European Parliament and of the Council on Establishing a Framework of Measures for Accelerating Industrial Capacity and Decarbonisation in Strategic Sectors,” Article 11(3); Ibid., Article 12(3).

[x] Ibid., amended Article 26(1)(a)(iv) and Article 28b of the NZIA.

[xi] Ibid., amended Article 26(7) of the NZIA.

[xii] Office of the United States Trade Representative, “WTO Government Procurement Agreement,” accessed March 2026, https://ustr.gov/issue-areas/government-procurement/wto-government-procurement-agreement.

[xiii] European Commission, “Negotiations and Agreements,” accessed March 27, 2026, https://policy.trade.ec.europa.eu/eu-trade-relationships-country-and-region/negotiations-and-agreements_en.

[xiv] International Energy Agency, Renewables 2025: Executive Summary (Paris: International Energy Agency, 2025), https://www.iea.org/reports/renewables-2025/executive-summary.

[xv] European Commission, “Proposal for a Regulation of the European Parliament and of the Council on Establishing a Framework of Measures for Accelerating Industrial Capacity and Decarbonisation in Strategic Sectors,” Article 17(1).

[xvi] Ibid., Article 17.

[xvii] France24, “China Warns EU over ‘Made in Europe’ Plan, Vows Countermeasures,” April 27, 2026, https://www.france24.com/en/europe/20260427-china-warns-eu-made-in-europe-plan-countermeasures.

[xviii] Huan Zhu, “Beijing Labels EU Industrial Accelerator Act ‘Systemic Discrimination,’” China Trade Monitor, March 10, 2026, https://www.chinatrademonitor.com/beijing-labels-eu-industrial-accelerator-act-systemic-discrimination/.

[xix] Euronews, “EU Vows to Fight ‘Tooth and Nail’ for European Industry as China Threatens Retaliation,” April 30, 2024, https://www.euronews.com/my-europe/2026/04/30/eu-vows-to-fight-tooth-and-nail-for-european-jobs-as-china-threatens-retaliation.

[xx] Olivia Rumble and Andrew Gilder, “SA Calls CBAM ‘Policy Coercive’ and LDCs Call Them ‘Beggar Thy Neighbour’ Instruments,” African Climate Wire, July 24, 2023, https://africanclimatewire.org/2023/07/sa-calls-cbam-policy-coercive-and-ldcs-call-them-beggar-thy-neighbour-instruments/.