The emergence of Kevin Warsh as a new Federal Reserve Chair has revived an economic debate we closely examine from a nonpartisan perspective: whether monetarism remains relevant. Warsh has often expressed admiration for the intellectual legacy of Nobel Prize-winning economist Milton Friedman, whose 1976 Nobel Memorial Prize in Economic Sciences recognized his contributions to consumption analysis, monetary history, and stabilization policy. Friedman’s influence on modern macroeconomics is difficult to overstate. Along with Anna Schwartz, he co-authored the landmark 1963 book “A Monetary History of the United States, 1867-1960,” which profoundly shaped central banking for decades and became one of the twentieth century’s most influential economic books.

For many economists who studied in the 1970s and 1980s, Friedman’s arguments were intellectually irresistible. During my early years as a graduate student pursuing a Ph.D. in Economics, I, too, was deeply influenced by Friedman’s persuasive arguments and his confidence that inflation could ultimately be traced to changes in the U.S. money supply. Friedman’s famous declaration that “inflation is always and everywhere a monetary phenomenon” became almost a foundational principle for generations of economists and policymakers.

At the center of Friedman’s monetarist framework stood the “Quantity Theory of Money,”

summarized by the equation MV = PY, where M is the money supply, V is the velocity of money, P is the price level, and Y is real output. The equation is an accounting identity and therefore always holds mathematically. The real issue is not whether the equation balances, but whether velocity remains sufficiently stable for changes in the money supply to reliably predict changes in nominal economic activity and inflation.

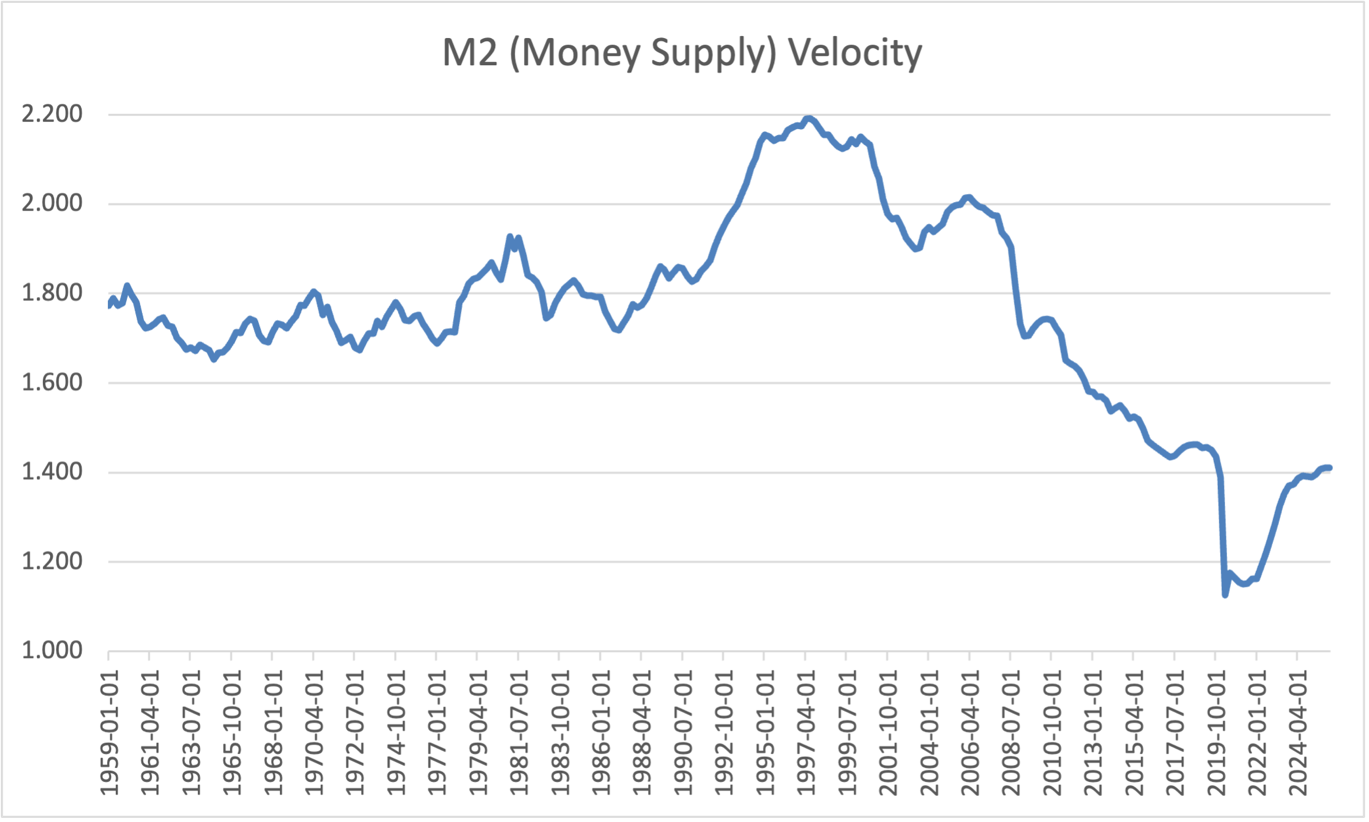

This assumption of a relatively stable velocity of money was central to the monetarist framework. If velocity remains predictable over time, excessive growth in the money supply should eventually translate into excessive growth in prices. From roughly 1959 through 1991, the data appeared to support Friedman’s argument reasonably well. M2 velocity fluctuated within a relatively narrow range, giving policymakers confidence that monetary aggregates could serve as a useful guide to inflation forecasting.

However, the historical record since 1991 has become far more complicated and far less supportive of strict monetarism. M2 velocity surged in the 1990s, then collapsed over the next several decades. The stability of M2 velocity that monetarism relied on gradually disappeared. This instability significantly weakened the predictive relationship between money supply growth and inflation.

Source: Board of Governors of the Federal Reserve System

The shift was not merely statistical noise. It reflected structural changes in the financial system. Financial deregulation, the growth of money market accounts, the rise of online banking, changes in payment technologies, globalization, declining interest rates, and evolving definitions of money all contributed to a dramatic shift in how money circulated through the economy. Consumers and businesses increasingly shifted funds among accounts and financial instruments, making traditional monetary aggregates less reliable as policy guides.

Understanding why this matters requires recognizing that monetarism is most effective when velocity is predictable. Before 1990, M2 velocity was relatively stable, but in the early 1990s, it increased, suggesting each dollar of the money supply supported more nominal economic activity. After peaking in the late 1990s, velocity declined steadily through the Global Financial Crisis and into the post-pandemic era.

This collapse in velocity posed significant challenges for monetarist theory. During the post-2008 Quantitative Easing era, the Federal Reserve dramatically expanded its balance sheet and the monetary base. Many monetarists initially warned that such rapid monetary expansion would inevitably produce runaway inflation. Yet inflation remained subdued for years because velocity collapsed. Banks accumulated excess reserves while households and businesses remained cautious in the aftermath of the financial crisis.

The experience led many economists and central bankers to reassess the reliability of monetary aggregates as forecasting tools. Former Federal Reserve Chair Jerome Powell even remarked in 2021 that M2 growth no longer seemed to have significant implications for the economic outlook. That statement would have been almost unthinkable during the height of monetarism’s influence in the late 1970s and early 1980s.

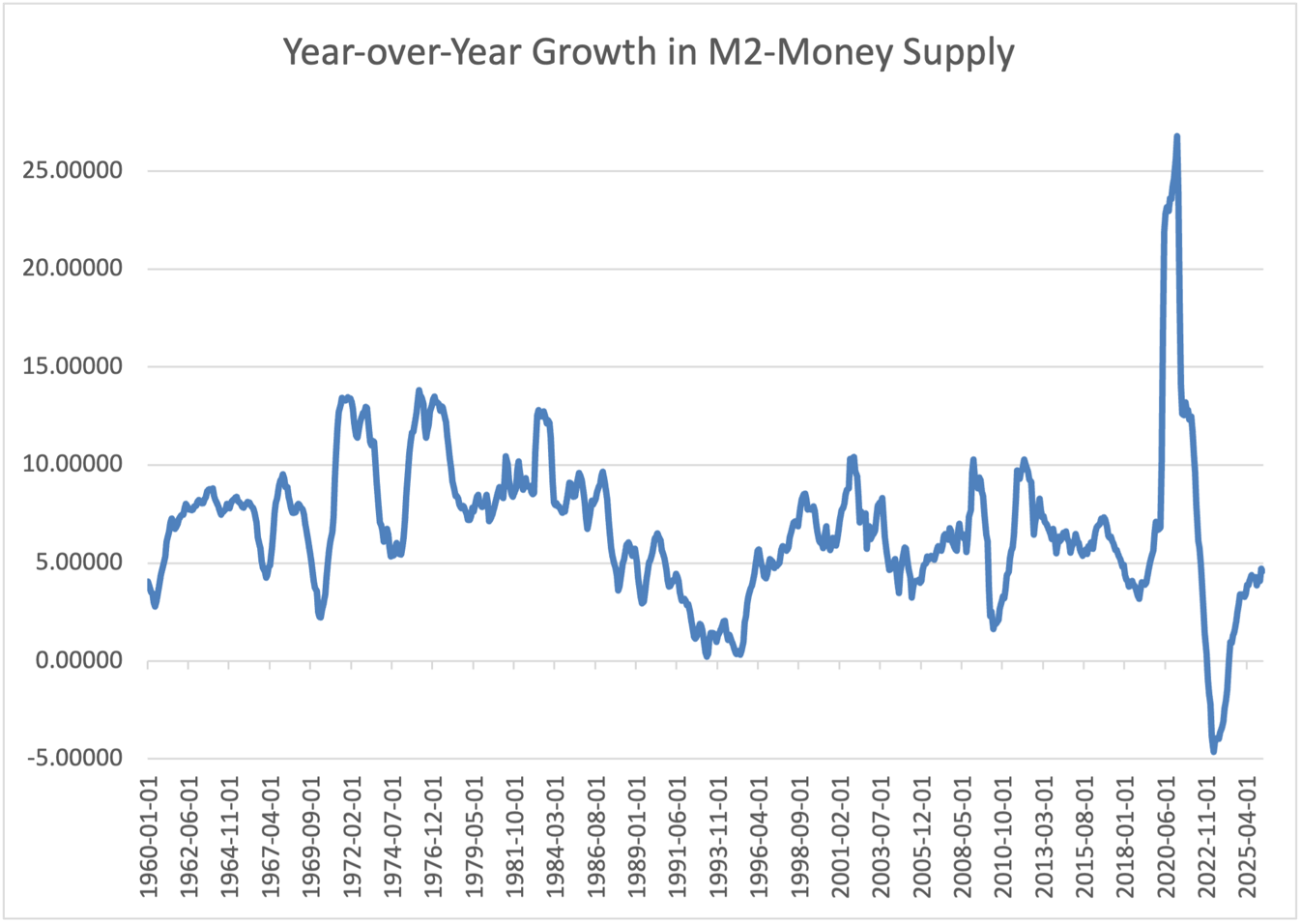

Yet the inflation surge that followed the pandemic has reopened the debate. In February 2021, annual M2 growth surged to +26.8%, an extraordinary increase rarely seen in modern American economic history. Supporters of monetarism, including Kevin Warsh, have cited this episode as vindication of Friedman’s core argument. Massive fiscal stimulus, combined with aggressive monetary accommodation, flooded the economy with liquidity just as supply chains were constrained.

Source: Board of Governors of the Federal Reserve System

There is certainly merit to the argument that such extraordinary monetary growth contributed to the subsequent inflationary surge. It would be difficult to deny that injecting such an unprecedented quantity of money into the economy created upward pressure on prices. However, the more difficult question is whether this proves that monetarism remains broadly reliable as a long-term framework for guiding monetary policy.

An analogy may help clarify the distinction. Observing that someone who smokes six packs of cigarettes per day faces severe health risks does not necessarily prove that someone who smokes one or two cigarettes daily will experience the same outcome. Extreme cases often support general principles without necessarily confirming the precision of the broader theory under normal conditions. Likewise, a 26.8% surge in money supply growth is an extreme monetary event. The fact that inflation follows does not automatically restore confidence that moderate changes in M2 can consistently predict inflation in a modern financial system with an unstable velocity.

Empirical evidence since 1991 suggests caution. One of the best ways to evaluate the quantity theory of money is to examine rolling long-term averages of money growth and inflation rather than relying on year-to-year fluctuations, which are heavily influenced by business cycles and temporary shocks. If monetarism were consistently reliable, long-run M2 growth should show a strong linear relationship with inflation.

Such tests tend to show that the relationship was reasonably strong in earlier decades, particularly during the Great Inflation era and the Volcker disinflation period. Paul Volcker’s Federal Reserve briefly adopted explicit targeting of monetary aggregates between 1979 and 1982 to crush inflation expectations. During that period, monetarism appeared highly effective because inflation and money growth were closely linked.

But after the early 1980s, the relationship weakened substantially. The years between 1982 and 1990 were a transitional period during which the Federal Reserve gradually abandoned strict money supply targeting. Financial innovation and deregulation increasingly distorted the meaning of traditional monetary aggregates. By the early 1990s, the Fed was shifting toward a modern framework centered on interest-rate targeting rather than money supply targeting.

By 1993, Federal Reserve Chair Alan Greenspan effectively acknowledged to Congress that M2 had become far less useful as an inflation predictor. The central bank subsequently relied more heavily on interest rates, labor market conditions, financial conditions, and inflation expectations rather than on monetary aggregates.

This evolution does not necessarily mean Friedman was entirely wrong. In many respects, Friedman correctly identified the dangers of excessive monetary expansion when velocity remains relatively stable. Moreover, his criticism of discretionary policymaking helped central bankers appreciate the importance of credibility, expectations, and controlling inflation.

Nevertheless, it is difficult to ignore that monetarism has struggled to explain on-the-ground economic facts since 1991. The instability of velocity has undermined the theory’s predictive consistency. Massive expansions in the monetary base after 2008 failed to produce immediate consumer inflation, while relatively modest changes in money growth during other periods occasionally coincided with significant inflationary movements driven by supply shocks, energy prices, globalization, or labor market disruptions.

This is where the comparison to John Maynard Keynes, who was famously known for his treatise: “The General Theory of Employment, Interest and Money,” becomes interesting. Keynes himself was often pragmatic and willing to adapt his views when economic conditions changed. Although the famous quote “When the facts change, I change my mind” may not have been his exact words, the spirit of intellectual flexibility was clearly reflected in his writings and policy evolution.

Economics is not physics and has sometimes been called the “inexact science,” as John Stuart Mill noted in 1844. Relationships that appear stable for decades can unravel as institutions, technologies, regulations, or human behavior evolve. No fixed law of nature governs the velocity of money. Confidence, financial innovation, demographics, interest rates, global capital flows, and countless other variables influence it.

For that reason, many modern economists argue that monetary policy should remain flexible rather than be rigidly tied to monetary aggregates. The Federal Reserve today operates in a vastly different financial environment than the one Milton Friedman analyzed in the mid-twentieth century. Electronic payments, derivatives markets, shadow banking systems, cryptocurrency ecosystems, and globally integrated capital markets have transformed how liquidity moves through the economy.

Still, Kevin Warsh’s apparent embrace of monetarist principles may not be as surprising as it first seems. His defense of Friedman is less about returning to rigid M2 targeting and more about restoring what he sees as monetary discipline and institutional accountability. Warsh has argued that central banks have grown too comfortable with prolonged market interventions, massive balance sheet expansions, and emergency measures that persist long after crises subside.

Summary and Concluding Thoughts

Today, monetarism serves more as a philosophical anchor than as a precise operating manual. Warsh appears to view the post-pandemic inflation episode as evidence that central banks ignored monetary excesses for too long and focused too narrowly on transitory supply disruptions. By reviving aspects of Friedman’s framework, he may be signaling a preference for a more rules-based, far less interventionist Federal Reserve.

Critics argue that an excessive focus on monetary aggregates risks oversimplifying a highly complex modern economy. In our modern world, inflation can stem as much from geopolitical shocks, trade fragmentation, labor shortages, demographic changes, and supply chain disruptions as from changes in the M2 money supply.

However, the inflation surge in 2021 and 2022 showed that central banks cannot entirely dismiss the role of money supply growth. The post-pandemic experience reminded policymakers that extreme monetary accommodation, combined with aggressive fiscal expansion, can still generate substantial inflationary pressures.

Ultimately, the modern debate over monetarism may not be about choosing between Friedman and modern-day monetary policy. Instead, it may involve recognizing that both frameworks contain important truths and important limitations. Friedman correctly emphasized the long-run dangers of unchecked monetary expansion, while others emphasize the complexity of economic behavior and the need to adapt policy to changing global economic conditions.

The historical behavior of M2 velocity strongly suggests that monetarism was more effective in an earlier financial era marked by relatively stable institutional structures and predictable money demand. Since 1991, however, the relationship between money growth and inflation has become far less stable.

That reality does not require economists to completely “unlearn” monetarism, as former Fed Chair Powell has suggested. But it does require acknowledging that the theory no longer explains the modern economy as consistently as it once appeared to. The world that Milton Friedman analyzed was not the world of quantitative easing, instant digital transactions, globalized capital markets, and algorithmic finance.

In the end, the renewed debate over monetarism is valuable because it forces economists and policymakers to confront a difficult truth: no economic theory remains permanently immune to changes in our economic landscape. As the economy and institutions evolve, the theories once held in high esteem must evolve as well. Milton Friedman’s insights still matter enormously, but the instability of M2 velocity since 1991 suggests that monetarism, while influential and historically important, may no longer serve as the reliable inflation compass it once was.