The Middle East and Ukraine wars keep escalating and adding to the risks created by President Trump’s trade and tariff wars. We have written about this before, noting that:

“Wars are easy to start, and very difficult to end”.

One problem is that most people have no memory of the last time the world faced similar challenges. That was during the Cold War of 1947-1989 between the West and the Soviet Union. Since then, wars have been local affairs.

But now the risks are becoming regional in both Europe and the Middle East. In turn, the US is becoming more and more involved.

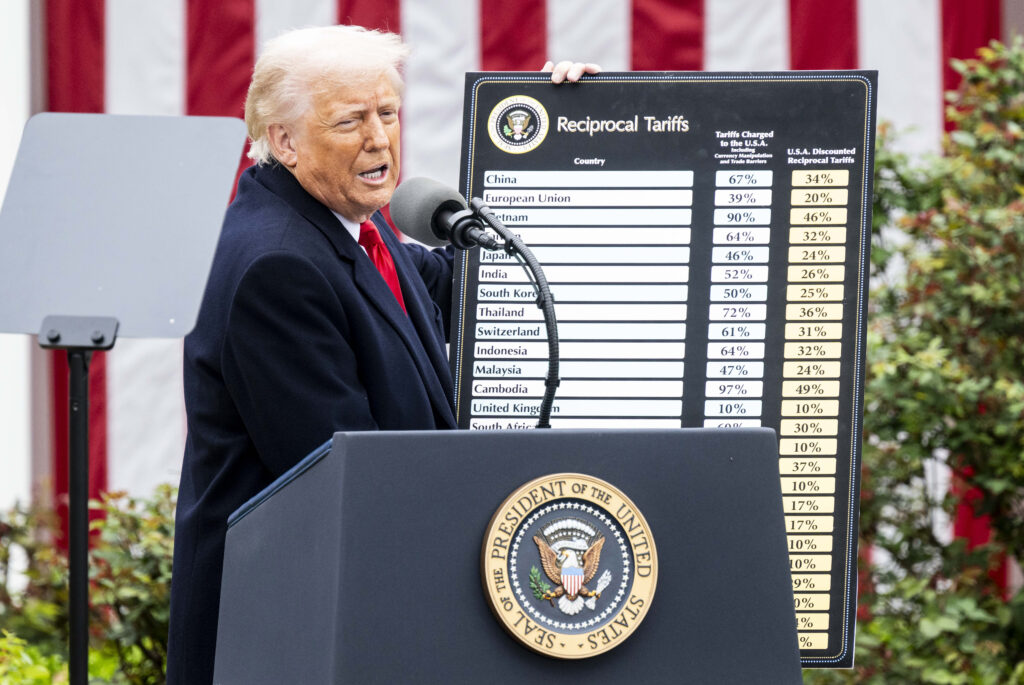

THE TRADE WAR IS SET TO INTENSIFY WITH NEW ‘RECIPROCAL TARIFFS’

Next month risks seeing a fairly rapid evolution of the tariff war into a full-blown trade war:

Some commentators argue that Trump is the ‘TACO’ president – ‘Trump Always Chickens Out’

But the evidence so far doesn’t support this argument

As Apollo notes, Trump increased average US tariffs to 3.7% in early February

These then peaked on Liberation Day, in early April, at 26.85%

But they are still at 13.45% today, and he is due to finalise additional ‘reciprocal tariffs’ by July 9

THE MILITARY WARS ARE CONTINUING TO ESCALATE

At the same time, the military wars are also escalating:

Trump originally promised to end the Ukraine war within 24 hours of taking office

But instead the war has continued to escalate, with Russia routinely attacking civilian targets

Similarly, Israel’s wars in Gaza and Lebanon have now evolved into a direct confrontation with Iran, rather than with Hamas in Gaza, and Hezbollah in Lebanon as its proxies:

In turn, Premier Netanyahu is returning to his long-held aim of regime change

And he is clearly hoping that Trump will intervene to bomb Iran’s nuclear sites

WHAT HAPPENS NEXT IS THE KEY QUESTION

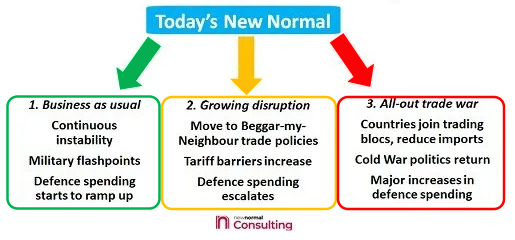

Companies and investors now have to review their plans for the summer, and H2. Essentially, they seem to have 3 choices:

They can hope for the best and hope that Trump might indeed be the TACO president

In this new ‘business as usual’ scenario, the key issue will be that levels of mistrust are growing

It will be a world of continuous instability, with new military flashpoints developing

The fact that this would have seemed a ‘worst case’ outlook at the beginning of the year, shows how much has changed:

Today’s world seems much more like the ‘Growing Disruption’ scenario

Trade barriers seem likely to continue increasing – mirroring the 1930s

And as in the 1930s, countries are starting to re-arm – and to expand their military

This scenario, as we have noted, means that defence spend is already reversing the post-1989 decline following the end of the Cold War:

As we look forward into H2, it would seem prudent to plan for further escalation

Countries will likely continue to join trading blocs to counter Trump’s tariff war

And defence spend will further increase as the Middle East/Ukraine wars escalate

WE DON’T KNOW IF TRUMP HAS A GRAND STRATEGIC PLAN

The world has grown used to US leadership in the post-Cold War period. When something went wrong, as in the 2008 subprime crisis, the US was expected to step forward.

As we have discussed here, the results in terms of stimulus policies, for example have not always been positive. But there was no-one else to act as the ‘global hegemon’.

President Trump seems to have now abandoned this role, as author Anne Applebaum told the BBC last week in this video:

“I think it’s really important to understand that Trump himself doesn’t think strategically. He doesn’t think about geopolitics. He doesn’t know what will happen in Iran.”

As Peggy Noonan, President Reagan’s adviser, noted on Friday:

“Congress should rush to rescue its rightful constitutional role, and take a stand in the war drama as it was elected to do.”