Quick overview

Live DAX Chart

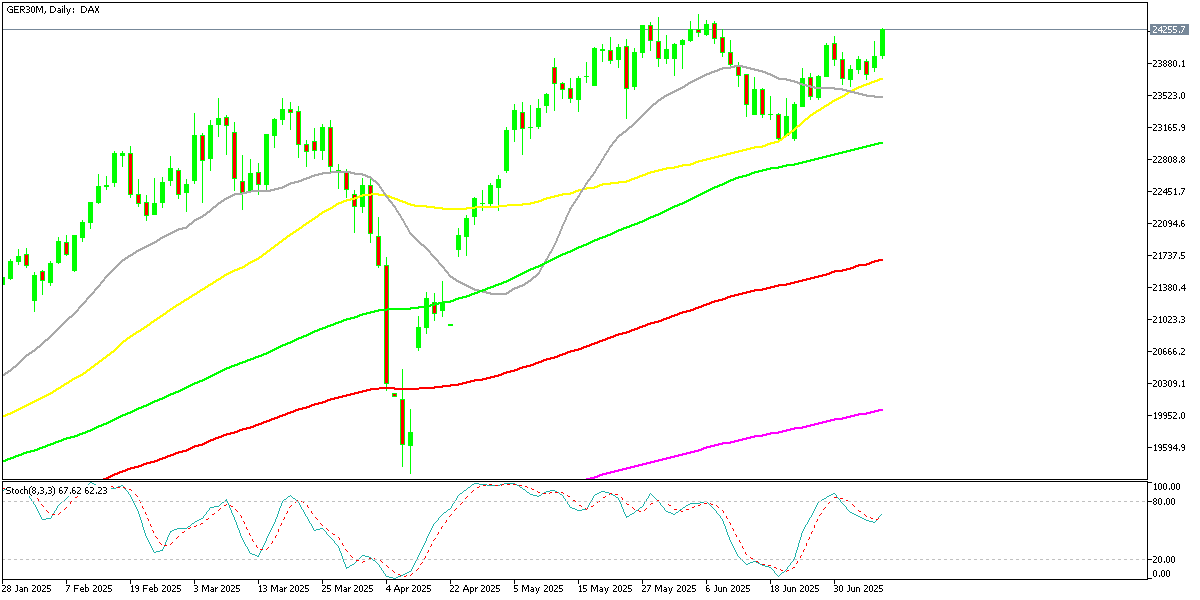

DAX

European stock markets ended the day broadly higher, with DAX approaching record highs, buoyed by signs of stabilizing economic conditions despite persistent trade and inflation risks.

Broad Gains Signal Renewed Optimism

European equity markets closed broadly higher, marking a cautiously optimistic start to the week. Investors seemed more at ease with the latest data suggesting that economic activity across the eurozone is stabilizing, even as inflation pressures and trade uncertainties continue to linger on the horizon.

The mood was helped by modestly improved growth forecasts and resilient purchasing manager survey results, hinting that the region may avoid a deeper slowdown over the summer. This shift in sentiment encouraged buyers back into equities after weeks of choppy trading.

Technical Support Holds for DAX

GermanyŌĆÖs DAX index closed comfortably above 24,200, delivering a technically encouraging signal that reinforced key support levels traders have been monitoring. This close suggests underlying buying interest remains strong enough to defend against sharper pullbacks for now.

Looking ahead, market participants will be closely watching upcoming corporate earnings reports and central bank commentary to gauge whether this rebound can build further momentum. Any dovish shifts or better-than-expected profit figures could act as catalysts for further gains.

Closing Levels for Main Euro Indices ŌĆō Detailed Recap

GermanyŌĆÖs DAX PERFORMANCE-INDEX

Closed at 24,206.91 points

Gained +133.24 points or +0.55% on the day

Extended its recovery from last weekŌĆÖs dip, supported by optimism over resilient manufacturing PMI figures and fading tariff fears.

FranceŌĆÖs CAC 40 Index

Settled at 7,766.71 points

Rose +43.24 points or +0.56%

Helped by banking and luxury shares rebounding as eurozone growth forecasts were modestly revised higher.

ItalyŌĆÖs FTSE MIB Total Return Index

Finished at 40,182.62 points

Jumped +268.37 points or +0.67%

Outperformed as investors welcomed calmer bond spreads and corporate earnings optimism in Milan-listed industrials.

SpainŌĆÖs IBEX 35 Index

Closed at 14,079.50 points

Edged up +4.70 points or +0.033%

The smallest move among majors, reflecting mixed bank sector performance and subdued energy names.

UKŌĆÖs FTSE UK Index

Ended at 548.09 points

Advanced +3.05 points or +0.56%

Continued its bounce despite lingering rate hike talk, as softer commodity prices helped sentiment.

Among major indices, ItalyŌĆÖs FTSE MIB led the charge higher, reflecting renewed confidence in local industrials and financials. FranceŌĆÖs CAC 40 and GermanyŌĆÖs DAX also posted solid gains, buoyed by easing fears of deeper economic contraction.

SpainŌĆÖs IBEX 35 finished little changed, weighed by mixed banking-sector performance, while the UKŌĆÖs FTSE advanced modestly as softer commodity prices helped temper rate-hike worries.

Crude oil prices continued to push higher despite the announcement of increased production from OPEC+. Futures settled up $0.40 at $68.40, supported by signs of ongoing supply tightness and resilient demand expectations.

In contrast, gold fell sharply, losing $40.84 or -1.22% to settle at $3,298.12, as investors rotated out of safe havens in favor of risk assets. Bitcoin was little changed on the day, trading near $108,200, maintaining its recent range despite ongoing volatility in crypto markets.

Outlook: Summer Rally or More Headwinds?

European indices appear poised for a potential summer rally if macroeconomic headwinds continue to ease and investors gain confidence in the regionŌĆÖs growth prospects.

However, geopolitical tensions, trade tariff developments, and persistent inflation pressures remain key swing factors that could limit upside potential or reignite volatility in the weeks ahead. Market watchers will need to balance optimism about stabilization with caution over lingering risks as the summer trading season unfolds.

DAX 40 Index Live Chart

Skerdian Meta

Lead Analyst

Skerdian Meta Lead Analyst.

Skerdian is a professional Forex trader and a market analyst. He has been actively engaged in market analysis for the past 11 years. Before becoming our head analyst, Skerdian served as a trader and market analyst in Saxo Bank’s local branch, Aksioner. Skerdian specialized in experimenting with developing models and hands-on trading. Skerdian has a masters degree in finance and investment.

Related Articles