With gold maintaining substantial gains despite recent volatility, the convergence of structural demand drivers, operational excellence among leading developers, and tactical market dynamics presents a multifaceted investment thesis for sophisticated capital allocation.

Current gold market conditions reflect the complex interplay between robust economic data and uncertain monetary policy trajectories. Strong retail sales figures and persistently low jobless claims signal economic resilience that could delay aggressive Federal Reserve rate cuts, creating near-term headwinds for non-yielding assets. However, these same conditions underscore the persistent inflationary pressures that fundamentally support gold’s monetary role.

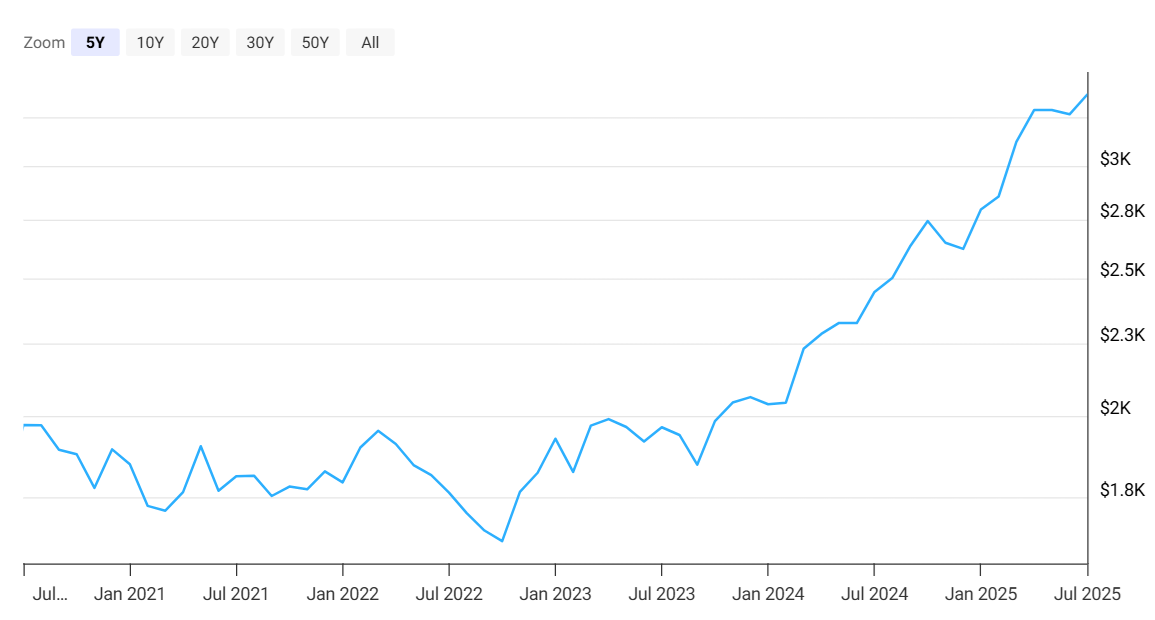

Despite tactical headwinds, gold’s 40% year-over-year performance demonstrates the underlying strength of structural demand drivers that transcend short-term policy considerations. The metal’s consolidation between $3,330-$3,400 per ounce reflects institutional repositioning rather than fundamental deterioration, creating strategic entry points for investors focused on longer-term value creation.

Gold at $3,372.83 as of July 2025, MacroTrends’ Gold Price Historal ChartStructural Demand & Central Bank Accumulation

Central bank gold accumulation represents one of the most significant structural shifts in precious metals markets, driven by geopolitical fragmentation and currency diversification imperatives. Recent data showing 24 tonnes of central bank purchases in February alone reflects sustained institutional demand that operates independently of retail investor sentiment or Federal Reserve policy cycles.

J.P. Morgan’s forecast of 900 tonnes in central bank purchases for 2025 underscores the scale of this demand transformation. This institutional accumulation occurs against a backdrop of supply constraints, with major producers facing declining grades and rising operational costs across traditional mining jurisdictions.

The de-dollarization trend accelerates these dynamics, as institutions seek alternatives to dollar-dominated reserve assets amid concerns over fiscal sustainability and geopolitical tensions. This structural shift provides fundamental support for gold prices independent of short-term economic data releases or monetary policy adjustments.

Operational Excellence Among Leading Gold Developers

The gold development landscape showcases exceptional operational achievements that demonstrate the sector’s evolution toward higher-quality, more efficient asset development. AngloGold Ashanti exemplifies this transformation, having delivered remarkable investor returns while building a globally diversified portfolio centered on premier jurisdictions.

Derek Macpherson of Olive Resource Capital, who has tracked AngloGold’s evolution, notes the company’s exceptional performance:

“This is a stock that is up 300% since we started buying it. Now that’s a couple years ago. So it’s holding period return is pretty high.”

This performance reflects not speculative trading but fundamental value creation through strategic asset optimization and operational excellence.

The company’s cash generation capability demonstrates the power of operational efficiency in the current high gold price environment. With gold trading above $3,300 per ounce, AngloGold generates approximately $8 million in daily free cash flow, providing substantial financial flexibility for funding growth initiatives without external dilution.

AngloGold’s strategic transformation from a South African-focused operation to a globally diversified miner illustrates the importance of jurisdictional optimization. Sam Pelaez explains the strategic rationale:

“They made a policy of relocating the headquarters to Denver and effectively that was a symbol of their plans to start growing in a safer – not to say that Africa is not safe but – a better received jurisdictions from an investor’s perspective.”Sam Pelaez & Derek Macpherson of Olive Resource Capital

High-Grade Asset Developments

The emergence of exceptional high-grade discoveries provides compelling investment opportunities through companies capable of extracting maximum value from superior ore bodies.

New Found Gold‘s exploration progress demonstrates similar scale potential across its extensive property position. Recent drilling results continue to expand known mineralization, with the company having completed over 610,000 meters of drilling across just five kilometers of a 110-kilometer property length, highlighting vast untapped potential. The company’s Queensway project in Newfoundland features a robust gold resource of 1.4 million ounces in the indicated category and 610,000 ounces in the inferred category, which enable highly selective mining approaches and exceptional economic returns.

Keith Boyle, CEO, emphasizes the operational advantages created by the project’s grade distribution:

“You end up with about 75% of the ounces in 25% of the tons. And it starts right at surface, and that’s a huge advantage in looking at how to start and develop this project.”

This grade concentration enables operational flexibility that becomes increasingly valuable during periods of market volatility. The Queensway project’s geological characteristics provide exceptional confidence levels rarely available in vein-type deposits. Boyle notes the strategic importance of surface exposure:

“One of the biggest risks in dealing with vein type deposits is advancing, especially in underground mines. Those are the ones that you’ll hear often, ‘they got to the veins and it was different than what was interpreted’. And so here we’re able to expose it right at surface, use that mapping, use that interpretation to then build the geological model.”

District-scale resource expansion opportunities provide leveraged exposure to exploration success while maintaining operational cash flow from initial development phases. This combination appeals to investors seeking both immediate catalyst exposure and longer-term growth potential.

Cabral Gold‘s scale potential enables significant resource growth beyond current estimates while benefiting from regional infrastructure and operational synergies.

“The strategy is we’ve got a ‘district scale play’. We’re right next door to G Mining’s Tocantinzinho project. We’ve already got 1.2 million ounces on the board here.” – Cabral Gold’s CEO Alan Carter

The convergence of tactical market conditions with fundamental structural drivers creates compelling entry points for strategic gold exposure through high-quality development companies. Current Federal Reserve policy uncertainty and elevated real yields provide temporary pressure on gold prices while underlying demand drivers remain intact. This environment favors companies with clear operational catalysts and near-term production potential.

West Wits Mining exemplifies this dynamic through its advanced South African project, where Executive Chairman Michael Quinert notes the strategic advantage:

“The other thing that debt does is to validate us, and also to hopefully to external investors the fact that the company’s been through a robust due diligence with bank standard diligence.”

The company’s updated feasibility study demonstrates the impact of current gold prices on project economics, with post-tax Net Present Value increasing from $246 million to $500 million USD. These improvements reflect both higher gold price assumptions and operational optimizations that extend mine life from 9 to 12 years at 70,000 ounces annually.

Interview with Michael Quinert, Chairman of West Witts Mining

Jurisdictional Advantages & Infrastructure Access

Tier-1 mining jurisdictions continue to attract disproportionate capital flows as investors prioritize regulatory certainty and operational predictability. Canada’s mining-friendly environment provides particular advantages, combining established legal frameworks with world-class infrastructure and skilled labor availability.

The strategic value of superior infrastructure becomes evident through projects like New Found Gold’s Queensway, which benefits from proximity to established communities and services. Boyle highlights these advantages:

“We’re close to infrastructure. The town of Gander, Newfoundland only 15 km away. We have hydro power that cuts through the site. The TransCanada Highway cuts through the site as well.”

European jurisdictions also demonstrate strategic value through projects that combine precious metals exposure with critical mineral components.

Mawson Finland‘s Rajapalot project illustrates this dynamic, where CEO Noora Ahola’s regulatory expertise provides unique advantages. She explains her background:

“Working for the authority was very important. To get that background is good for this job because it’s all about the permitting. It’s all about talking with the locals and having social acceptance here in the area.”

The company’s Rajapalot project contains 867,000 ounces of gold and 4,311 tons of cobalt, and is advancing through a two-year Environmental Impact Assessment (EIA) process alongside land use planning, positioning for mining license application with strong local community engagement.

Interview with Noora Ahola, CEO of Mawson Finland

Capital Efficiency and Project Economics

The current market environment rewards capital-efficient development strategies that minimize upfront investment requirements while maximizing early cash flow generation. Projects featuring heap-leach processing capabilities and phased construction approaches provide particular appeal during periods of elevated capital costs and supply chain constraints.

Cabral Gold‘s Cuiú Cuiú oxide starter project demonstrates these principles through exceptional economic metrics. CEO Alan Carter emphasizes the project’s financial positioning:

“The IRR on this project back in September we used an assumed gold price of $2,250 an ounce. That’s $1,000 below the current gold price, but the IRR on the project back in September was 47% post-tax.”

The project’s initial capital expenditure of US$37.4 million and all-in sustaining costs of US$1,003 per ounce reflect the capital efficiency that institutional investors prioritize during volatile market conditions. These metrics provide substantial margins above operating costs while maintaining expansion optionality for larger-scale development phases.

Structural Demand Foundation: Central bank accumulation of 900 tonnes projected for 2025, de-dollarization trends, and inflation persistence create fundamental support independent of short-term policy cycles – allocate 5-10% portfolio exposure to capture structural demand shiftOperational Excellence Premium: Target companies demonstrating 300%+ returns through strategic asset optimization and cash generation exceeding $8 million daily – focus on established producers with proven management teams and diversified geographical exposureHigh-Grade Asset Leverage: Prioritize projects featuring exceptional grade distribution (75% ounces in 25% tonnage) and surface-starting mineralization – provides operational flexibility and superior economics during volatile market conditionsJurisdictional Quality Focus: Concentrate investments in tier-1 jurisdictions (Canada, established European mining regions) with regulatory certainty, infrastructure access, and skilled labor availability – reduces execution risk and enhances long-term value potentialCapital Efficiency Strategy: Target projects with IRRs exceeding 40%, initial capex under $50 million, and heap-leach processing capabilities – enables rapid payback periods and reduced dilution risk during development phasesTactical Entry Timing: Utilize current Federal Reserve policy uncertainty and elevated real yields as strategic entry points – position ahead of expected policy pivots in late 2025/early 2026 development timelinesDistrict-Scale Expansion: Seek companies with multi-million ounce resource bases and extensive exploration potential – provides leveraged exposure to resource expansion beyond initial production scenariosNear-Term Catalyst Focus: Prioritize companies with clear operational milestones including feasibility study updates, permitting progress, and production timelines within 12-24 months – creates multiple value inflection points

The gold investment landscape presents compelling opportunities for investors who recognize the convergence of structural demand drivers with tactical market conditions. Central bank accumulation, de-dollarization trends, and persistent inflation concerns provide fundamental support that transcends short-term Federal Reserve policy uncertainty. Meanwhile, exceptional operational achievements among leading developers demonstrate the sector’s evolution toward higher-quality, more efficient asset development in premier jurisdictions. The combination of immediate development catalysts with longer-term strategic positioning enables balanced exposure to both tactical gold market movements and structural economic shifts that favor precious metals allocation.