Crude oil prices settled marginally higher last week, reversing the decline recorded the previous week, as supply disruption fears outweighed fading optimism over a Russia-Ukraine peace deal and fresh attacks on each other’s energy facilities. These developments escalated geopolitical tensions in the Middle East, drawing in countries across the world either directly or indirectly. Additionally, the United States imposed a 25 percent penalty on India, raising total tariffs to 50 percent, in response to India’s continued crude oil imports from Russia, which Washington believes support Moscow’s war in Ukraine.

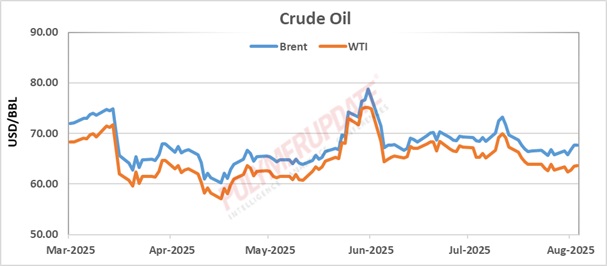

According to Polymerupdate Research, benchmark Brent crude opened the week on a bullish note, with the near-month delivery contract on the InterContinental Exchange (ICE) closing at US$66.60 a barrel on Monday, up from US$ 65.85 a barrel the previous week. Amid volatility, futures slipped to US$ 65.79 a barrel on Tuesday but quickly rebounded to end at US$ 66.84 a barrel on Wednesday. The uptrend continued on short covering, with Brent futures closing at US$ 67.67 a barrel on Thursday and marginally higher at US$ 67.73 a barrel on Friday. Against the previous week’s drop of 1.11 percent, or US$ 0.74 a barrel, Brent futures ended last week with an overall gain of 2.85 percent, or US$ 1.88 a barrel.

According to Polymerupdate Research, benchmark Brent crude opened the week on a bullish note, with the near-month delivery contract on the InterContinental Exchange (ICE) closing at US$66.60 a barrel on Monday, up from US$ 65.85 a barrel the previous week. Amid volatility, futures slipped to US$ 65.79 a barrel on Tuesday but quickly rebounded to end at US$ 66.84 a barrel on Wednesday. The uptrend continued on short covering, with Brent futures closing at US$ 67.67 a barrel on Thursday and marginally higher at US$ 67.73 a barrel on Friday. Against the previous week’s drop of 1.11 percent, or US$ 0.74 a barrel, Brent futures ended last week with an overall gain of 2.85 percent, or US$ 1.88 a barrel.

Similarly, West Texas Intermediate (WTI) Cushing futures for near-month delivery on the New York Mercantile Exchange (Nymex) opened the week firmer, closing at US$ 63.42 a barrel on Monday compared with US$ 62.80 a barrel at the end of the prior week. However, gains proved short-lived as opportunistic profit-booking pushed the contract down to US$ 62.35 a barrel on Tuesday. Prices rebounded thereafter, rising to US$ 62.71 a barrel on Wednesday and US$ 63.52 a barrel on Thursday. WTI Cushing futures closed the week at US$ 63.66 a barrel, marking a weekly gain of 1.37 percent, or US$ 0.86 a barrel—narrower than the previous week’s decline of 1.69 percent, or US$ 1.08 a barrel.

An analyst at Kedia Stocks and Commodities Research noted, “Escalating geopolitical tensions and shifting supply-demand signals drove crude oil prices higher last week. Hopes for a near-term peace deal between Russia and Ukraine faded after reports of intensified strikes on both sides, raising concerns about supply disruptions. At the same time, U.S. pressure on India heightened, with Washington imposing an additional 25 percent tariff on Indian goods effective August 27—a move that complicates India’s crude imports, given oil accounts for nearly 35 percent of its import basket.”

Russia-Ukraine bombardments

In the heaviest bombardment in recent weeks, Russia launched 574 drones and 40 missiles on Ukraine late last week, causing severe damage to Ukrainian infrastructure. The attacks coincided with U.S. President Donald Trump’s efforts to initiate a peace deal between the two warring neighbours, whose conflict began more than three and a half years ago. The heavy shelling further derailed peace talks, with both sides reasserting their positions. Meanwhile, Ukrainian President Volodymyr Zelenskyy said he was ready to meet Russian President Vladimir Putin at a neutral venue in Europe—possibly Switzerland, Austria, or even Istanbul.

However, the U.S.-initiated Russia-Ukraine peace talks were once again pushed to the backburner, as President Putin reportedly pressed for new demands to end the war. According to reports, Putin has demanded that Ukraine cede the entire eastern Donbas region, abandon its ambitions to join the North Atlantic Treaty Organization (NATO)—a military alliance founded on the principle of collective defense, where an attack on one member is considered an attack on all—and bar Western troops from entering the country.

Both Russian and Ukrainian forces have intensified strikes on each other’s energy facilities, including production centers, storage tanks, and transport infrastructure. Each side believes these assets are being used to fuel military operations and generate revenue for the Kremlin’s war effort. Ukrainian drones have targeted multiple refineries, including Rosneft’s plants in Novokuybyshevsk and Saratov, as well as the Volgograd refinery—the largest in southern Russia and among the top ten nationwide. Recently, Ukrainian forces also struck the Russian port of Olya in Astrakhan Oblast, a hub for Iranian-made Shahed drones, along with refineries in Volgograd, Saratov, and Syzran.

Russia has responded with its own attacks. On Monday, Russian drones struck an oil depot owned by Azerbaijan’s state oil company SOCAR in Ukraine’s southern Odesa region—for the second time in two weeks. Experts noted that it remains difficult to assess the full extent of the damage to Ukraine’s economy and energy sector. Monday’s strikes followed an August 8 Russian drone attack on another SOCAR oil depot, which injured at least four people and damaged energy infrastructure.

Kpler’s slow demand growth forecasts

Energy research and analytics firm Kpler has forecast that global crude oil demand will remain subdued in 2025 and 2026, weighed down by the proliferation of electric vehicles worldwide and weak economic growth. Kpler expects global fuel demand to rise by about 840,000 barrels per day (bpd) in 2025, accelerating only modestly to 880,000 bpd in 2026 amid weak consumer confidence. Kpler analyst Esteban Moreno sees no demand growth in the Asia-Pacific region, citing China’s petrochemical overcapacity, slower economic expansion, aging populations, and continued improvements in fuel efficiency as key factors behind the stagnation.

Kpler’s outlook aligns with the downbeat projection of the International Energy Agency (IEA). The Paris-based intergovernmental body highlights lackluster consumption across major economies and warns that, with consumer confidence still muted, a sharp rebound is unlikely. Consumption in emerging and developing economies has also fallen short of expectations, with downward revisions for China, Brazil, Egypt, and India. On the supply side, the agency revised its global oil supply growth forecast upward by 370,000 bpd to 2.5 million bpd for this year, and by 620,000 bpd to 1.9 million bpd in 2026.

US inventories fall

According to the U.S. Energy Information Administration (EIA), commercial crude oil inventories (excluding the Strategic Petroleum Reserve) fell by 6 million barrels for the week ending August 15, compared with the previous week. The drawdown was steeper than analysts’ expectations of a 1.8 million-barrel decline. At 420.7 million barrels, U.S. crude oil inventories are about 6 percent below the five-year average for this time of year.

Total motor gasoline inventories decreased by 2.7 million barrels from the prior week and now stand 1 percent below the five-year seasonal average. The drop in gasoline stocks defied market expectations for a 915,000-barrel decline, reflecting steady driving demand during the summer travel season. A similar trend was evident in the four-week average of jet fuel consumption, which climbed to its highest level since 2019.

Outlook

Crude oil has been caught in the crosshairs of rapidly shifting market dynamics, with fundamentals on both sides signalling strong moves. While oversupply from additional output by the Organization of the Petroleum Exporting Countries and its allies (OPEC+), along with restored production in Venezuela, points to a potential supply glut, fresh U.S. sanctions on Russia and restrictions on Iranian crude supply may help balance the market.

DILIP KUMAR JHA

Editor

dilip.jha@polymerupdate.com