A regulatory announcement has suddenly cooled the recent fervor surrounding cryptocurrency stocks. Recently, Nasdaq has indicated that it will strengthen its scrutiny of publicly listed companies holding cryptocurrencies, which has subsequently pressured the stock price of DAT (Digital Asset Trust). Many companies with a premium rate over their net asset value (mNAV) have fallen ‘underwater’ amid this reversal of sentiment, potentially slowing the previously rapidly spinning financial wheel.

Nasdaq’s intervention puts pressure on the stock price and premium rates of DAT in the U.S. market.

On September 4, The Information reported, citing informed sources, that Nasdaq is intensifying its scrutiny of listed companies, particularly those that inflate their stock prices by raising funds to purchase and hoard cryptocurrencies.

As the exchange responsible for the majority of cryptocurrency stock trading, Nasdaq believes such practices may mislead investors, prompting it to enhance regulatory measures. Specific actions have not yet been disclosed, but it is expected that affected companies will be required to disclose their investment scale, strategies, and potential risks, with special scrutiny on those frequently trading in cryptocurrency assets. If companies fail to comply with the regulations, the exchange may take measures such as suspending trading or delisting.

In fact, U.S.-listed companies dominate the DAT market. According to data from consulting firm Architect Partners, since January this year, at least 154 publicly listed companies in the U.S. have participated in purchasing cryptocurrencies. Meanwhile, data from Bitcointreasuries tracking Bitcoin-financial publicly listed companies shows that there are 61 such companies in the U.S., while markets in Canada, the UK, and Japan lag significantly behind. Should Nasdaq intervene, the overall market development of DAT is likely to face substantial impact.

In fact, U.S.-listed companies dominate the DAT market. According to data from consulting firm Architect Partners, since January this year, at least 154 publicly listed companies in the U.S. have participated in purchasing cryptocurrencies. Meanwhile, data from Bitcointreasuries tracking Bitcoin-financial publicly listed companies shows that there are 61 such companies in the U.S., while markets in Canada, the UK, and Japan lag significantly behind. Should Nasdaq intervene, the overall market development of DAT is likely to face substantial impact.

With the news of increased regulation from Nasdaq, market confidence has been impacted. The stock prices of DAT companies in the U.S. have generally come under pressure.

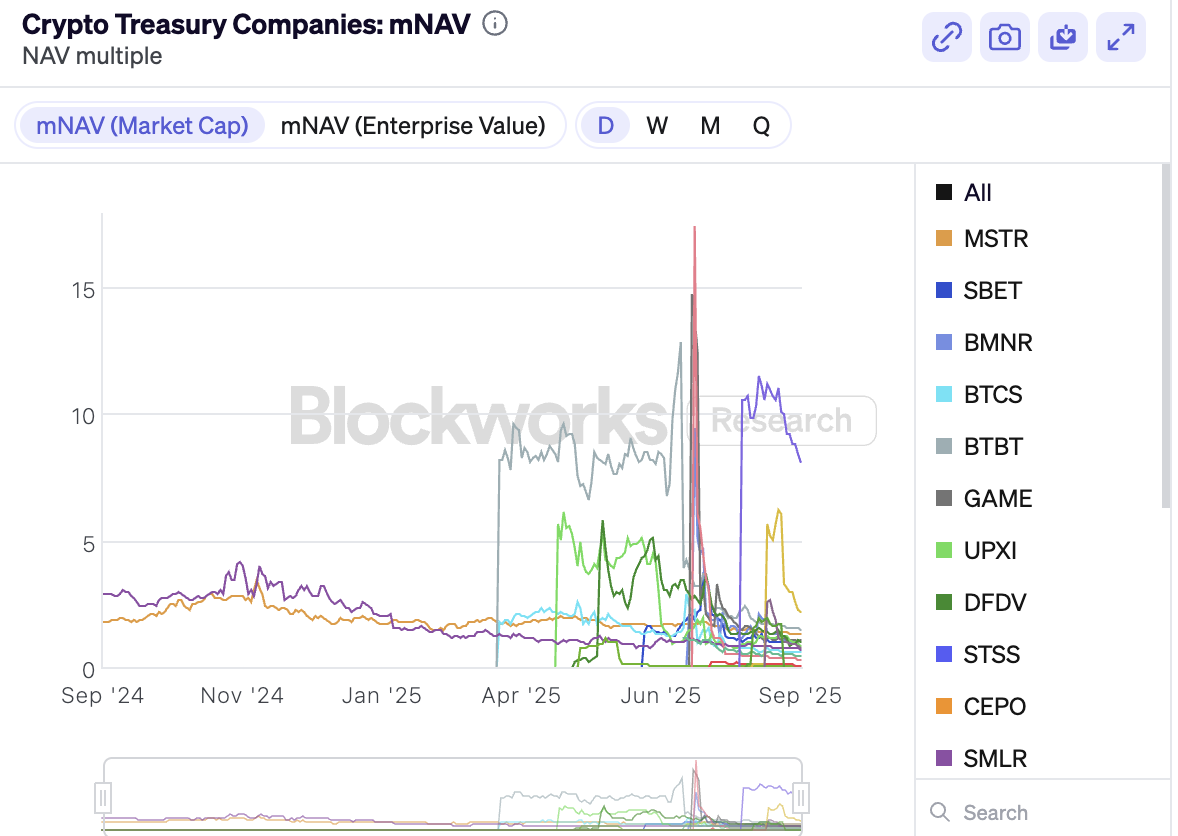

Meanwhile, the mNAV (market value to net asset value ratio) has also generally declined. According to Blockworks data, as of September 4, for example, $Strategy (MSTR.US)$ The mNAV has fallen to 1.3 times, SBET to 0.82 times, and BMNR to 0.88 times. Notably, only six DAT companies have an mNAV above 1, while the remaining companies continue to experience negative premiums, indicating a further weakening of the previously relied upon reservoir effect of appreciating crypto assets.

Tighter regulation may exacerbate market differentiation.

With the impending regulatory pressure, the landscape of the DAT market may witness new changes.

On one hand, strengthened regulation encourages DAT companies to adopt more transparent and cautious investment strategies in crypto assets, which helps to mitigate risks associated with potential market manipulation and insider trading. According to Fortune, several publicly listed cryptocurrency treasury companies have experienced unusual stock price fluctuations. For example, $SharpLink Gaming (SBET.US)$ the stock price hovered below $3 in April and early May, but after announcing plans to increase its Ethereum reserve assets by $425 million on May 27, the stock price surged to nearly $36. In the three trading days prior to the announcement, SharpLink’s stock price had doubled from $3 to $6, although the company did not submit relevant documents to the SEC or issue a press release. Similar situations have also occurred with companies such as Mill City Ventures, MEI Pharma, Kindly MD, Empery Digital, Fundamental Global, and 180 Life Sciences Corp.

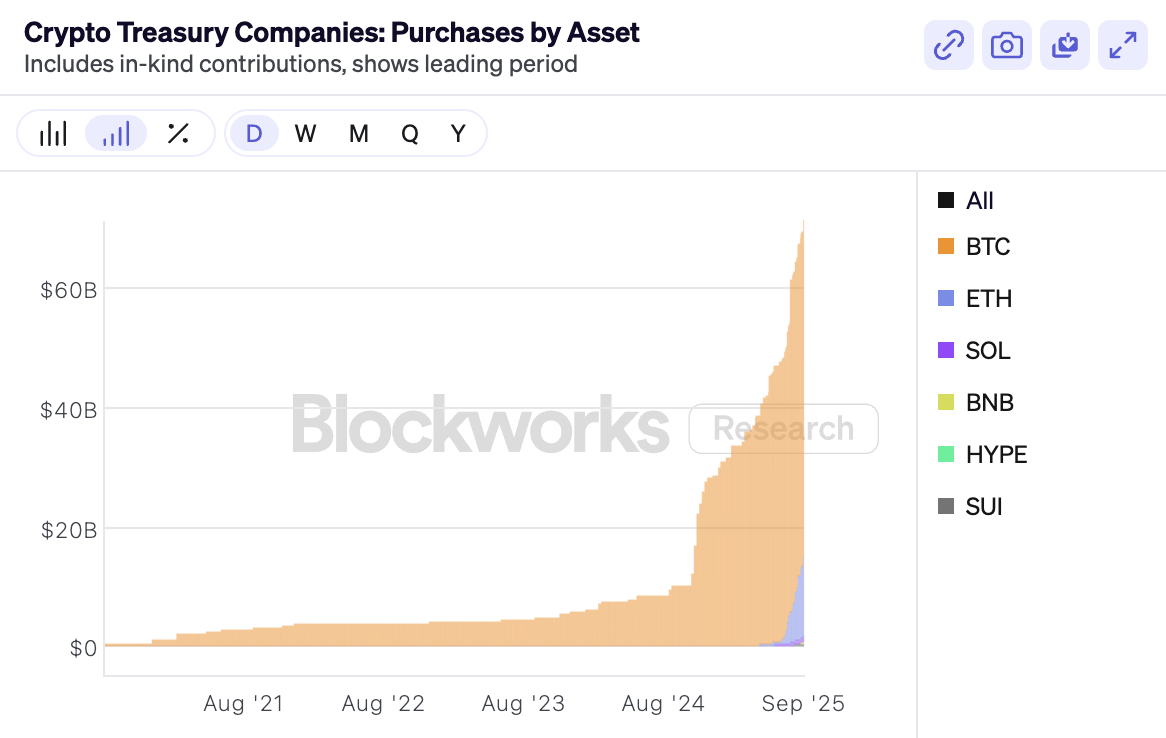

On the other hand, the head effect in the DAT market will become more pronounced. Although cryptocurrency treasury strategies are becoming increasingly popular in the market, covering… $Bitcoin (BTC.CC)$ 、 $Ethereum (ETH.CC)$ 、 $Solana (SOL.CC)$ 、 $TRON (TRX.CC)$ 、 $Binance Coin (BNB.CC)$Among various assets, Blockworks data shows that as of September 4, the total value of cryptocurrencies held by DAT Company has exceeded $69.5 billion, primarily concentrated in Bitcoin and Ethereum, amounting to $68.1 billion. Among these asset types, only Bitcoin’s mNAV reached 1.17, while the rest of the assets were below 1, reflecting investors’ insufficient recognition of other crypto assets.

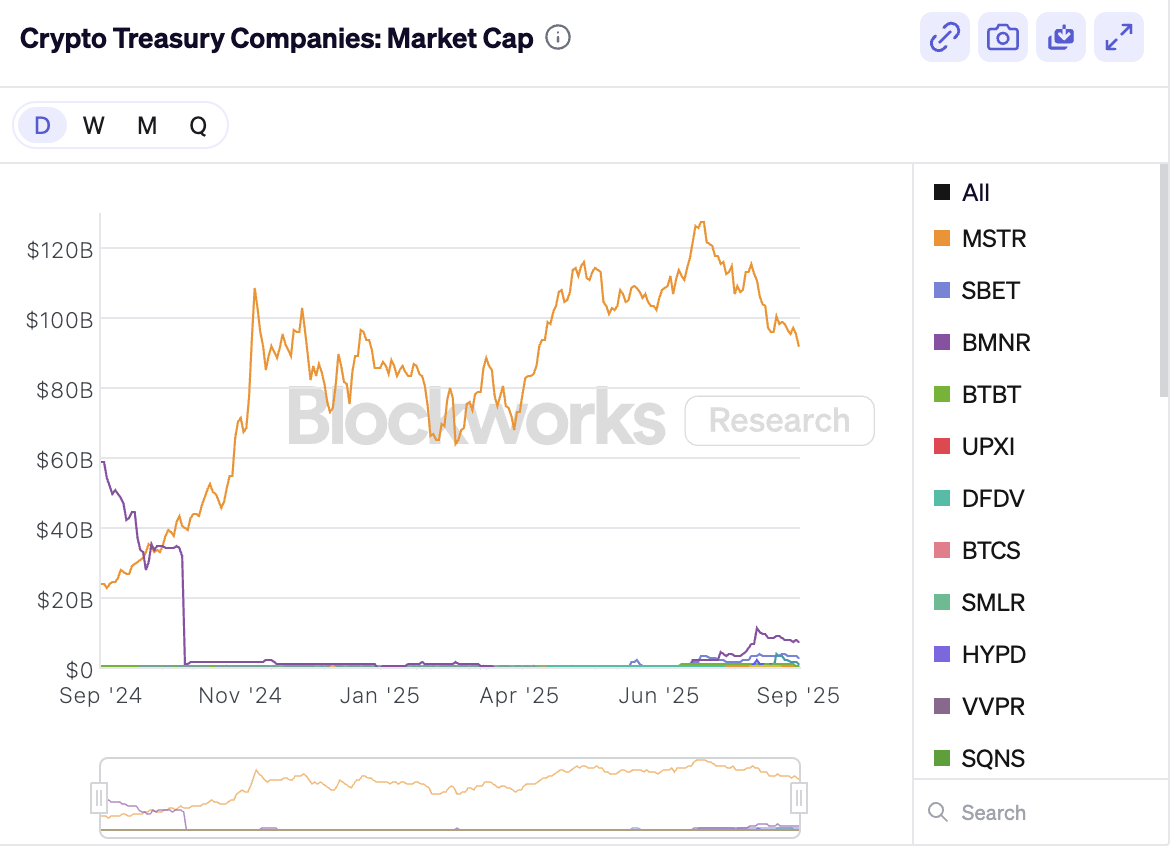

Moreover, leading companies also occupy the vast majority of market share. According to Blockworks data, as of September 4, the total market capitalization of crypto treasury companies exceeded $108.48 billion, with Bitcoin and Ethereum being the leaders in reserves.$Strategy (MSTR.US)$ and $Bitmine Immersion Technologies (BMNR.US)$Contributed over 91.4% of the market share. This means that in the future market, the advantages of leading companies and mainstream assets may be further strengthened, while marginal assets will face survival pressure.

Furthermore, regulatory tightening may slow the expansion of the entire DAT market. If the financing costs and difficulties for DAT-listed companies increase, it will directly affect the pace of investment, namely the scale and speed of currency accumulation. At the same time, the shrinking arbitrage space and market opportunities will also diminish the attractiveness of the DAT model, especially for companies with limited financial strength or those focused on a single small cryptocurrency.

“The DAT company that the market is preparing for must fully acquire (100% acquisition) the stocks of the U.S. shell company before it can first announce the transition to the DAT micro-strategy model, and it must hold a shareholders’ meeting to vote. This actually increases the operational costs and cycles of the new DAT treasury company; listed companies that have already transitioned to the DAT treasury model must also hold a shareholders’ meeting to vote before issuing additional stocks. Issuing bonds or convertible bonds does not fall under the issuance of new stocks and should not be included in this regulation.”

Analysis from cryptocurrency KOLs indicates that Nasdaq’s official move is aimed at cooling down the DAT model, making it more difficult for shell companies to transform, and increasing the process for newly transformed companies to issue additional shares. In the short term, this should dampen the market, making it increasingly challenging for many DAT treasury companies of altcoins. Furthermore, those companies that have already transformed into DAT treasuries will need to secure shareholder approval and obtain a majority vote at shareholder meetings without resorting to capital manipulation tactics (such as directly exchanging tokens for shares or purchasing discounted tokens).

The sustainability of DAT has sparked controversy.

Regarding the escalating trend of DAT, the market has exhibited polarized reactions.

Supporters view it as the best bridge for transferring crypto assets on and off-chain, believing that this new model may rewrite the liquidity landscape of the crypto financial market.

For instance, Xiao Feng, Chairman and CEO of HashKey Group, believes that DAT may be the best way for transferring crypto assets from on-chain to off-chain and elaborated on the four core advantages of DAT compared to ETFs: better liquidity. ETF subscriptions and redemptions require considerable time, whereas DAT facilitates a more convenient and efficient asset transfer for investors; higher price elasticity. DAT’s market value is highly volatile and possesses risk isolation attributes, providing institutions with more arbitrage tools; more rational leverage design. DAT companies offer leveraged financing structures that can yield higher premiums for investors compared to the growth of cryptocurrency prices; built-in downside protection mechanism. When the stock price falls below the net asset value of the company, investors are provided with the opportunity to purchase Bitcoin or ETFs at a discount. Such occurrences where the stock price falls below the net asset value will quickly be smoothed out by the market.

Moreover, several crypto venture capital firms are increasing their investments in DAT. For example, Pantera Capital disclosed for the first time that it has invested over $300 million in DAT companies; DWF Labs’ Executive Partner Andrei Grachev also stated recently that he is willing to provide 10% to 20% of financing for projects aimed at establishing token treasuries for U.S. listed companies.

However, many voices have raised doubts about the sustainability of DAT. According to Adam Reeds, co-founder and CEO of Ledn, digital asset treasury companies that are keen on accumulating coins are facing a turning point. Bitcoin treasury companies were once a revolutionary innovation in the industry, but now such extraordinary returns are hard to replicate. What is genuinely fading is the ability to create unique value propositions. Most DAT company CEOs claim that their sole objective is to enhance the per-share cryptocurrency holdings, but it remains unclear whether they possess a unique management team and outstanding capital operation capabilities.

Similarly, James Check, Chief Analyst at Glassnode, believes that the Bitcoin treasury strategy is much shorter-lived than most expect and may already have ended for many new entrants. This is not a “measuring contest”; the key lies in the sustainability of a company’s products and strategies within the long-term Bitcoin market. Furthermore, as investors favor early adopters, newly established Bitcoin treasury companies are facing a tough battle.

Further doubts arise from the assessment of the nature of DAT finance. Nate Geraci, President of The ETF Store, stated that if investors truly have a positive outlook on Bitcoin and Ethereum, they can directly purchase spot assets or ETFs instead of relying on DAT as a derivative alternative. He emphasized that the prosperity of such companies largely depends on regulatory arbitrage, and as regulatory barriers are gradually dismantled, the market demand for them will naturally diminish.

Analysts at Franklin Templeton warned that if the market capitalization of DAT falls below its net asset value, new stock issuances will create a dilution effect, hindering capital formation. If this is compounded by a decline in cryptocurrency prices, companies may be forced to sell assets to maintain stock prices, further depressing the market and confidence, thus creating a self-reinforcing downward spiral. Former Goldman Sachs analyst Josip Rupena even compared DAT to CDOs (Collateralized Debt Obligations) from the 2007–2008 financial crisis, pointing out that although crypto treasury companies ostensibly hold untraded, counterparty risk-free bearer assets, they actually introduce multiple risks, including management capacity, cybersecurity, and insufficient capital generation capacity, which may amplify into systemic risk.

Overall, the development prospects of DAT hinge on whether it can move beyond a reliance solely on regulatory arbitrage and leverage amplification logic, achieve sustainable development by maintaining market capitalization above net assets, continuously create value-added transactions, and establish an effective risk management framework.

Editor/joryn