The board of Hibiscus Petroleum Berhad (KLSE:HIBISCS) has announced that it will pay a dividend on the 23rd of October, with investors receiving MYR0.005 per share. This payment means that the dividend yield will be 5.4%, which is around the industry average.

Hibiscus Petroleum Berhad’s Payment Could Potentially Have Solid Earnings Coverage

Unless the payments are sustainable, the dividend yield doesn’t mean too much. Prior to this announcement, Hibiscus Petroleum Berhad’s dividend was comfortably covered by both cash flow and earnings. This indicates that a lot of the earnings are being reinvested into the business, with the aim of fueling growth.

The next year is set to see EPS grow by 65.1%. If the dividend continues along recent trends, we estimate the payout ratio will be 45%, which is in the range that makes us comfortable with the sustainability of the dividend.

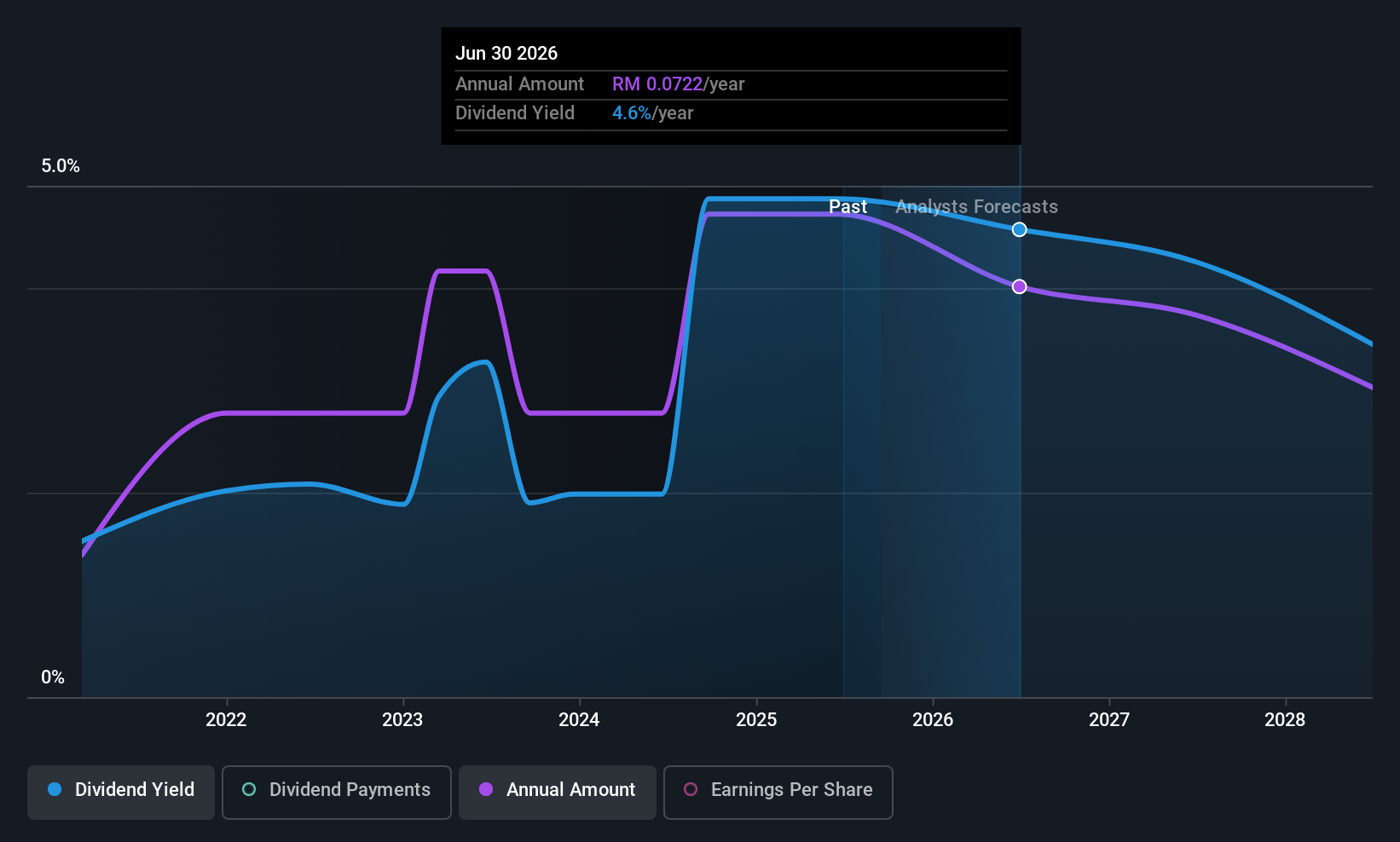

KLSE:HIBISCS Historic Dividend September 17th 2025

KLSE:HIBISCS Historic Dividend September 17th 2025

View our latest analysis for Hibiscus Petroleum Berhad

Hibiscus Petroleum Berhad’s Dividend Has Lacked Consistency

It’s comforting to see that Hibiscus Petroleum Berhad has been paying a dividend for a number of years now, however it has been cut at least once in that time. This makes us cautious about the consistency of the dividend over a full economic cycle. Since 2020, the dividend has gone from MYR0.025 total annually to MYR0.085. This implies that the company grew its distributions at a yearly rate of about 28% over that duration. Despite the rapid growth in the dividend over the past number of years, we have seen the payments go down the past as well, so that makes us cautious.

The Dividend Looks Likely To Grow

With a relatively unstable dividend, it’s even more important to evaluate if earnings per share is growing, which could point to a growing dividend in the future. Hibiscus Petroleum Berhad has impressed us by growing EPS at 23% per year over the past five years. The company’s earnings per share has grown rapidly in recent years, and it has a good balance between reinvesting and paying dividends to shareholders, so we think that Hibiscus Petroleum Berhad could prove to be a strong dividend payer.

We Really Like Hibiscus Petroleum Berhad’s Dividend

Overall, we think that this is a great income investment, and we think that maintaining the dividend this year may have been a conservative choice. Distributions are quite easily covered by earnings, which are also being converted to cash flows. Taking this all into consideration, this looks like it could be a good dividend opportunity.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. Taking the debate a bit further, we’ve identified 2 warning signs for Hibiscus Petroleum Berhad that investors need to be conscious of moving forward. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

Discover if Hibiscus Petroleum Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.