The guest commentary below was written by written by Daniel Lacalle. This piece does not necessarily reflect the opinions of Hedgeye.

In 2025, the mainstream Keynesian narrative that the United States would inevitably experience a recession and stagflation has proven to be utterly incorrect. The American economy is performing much better than its comparable nations, is showing broad-based strength, and even has indications of accelerating growth, giving investors and consumers plenty of reason to feel more optimistic, despite the consensus estimates from earlier in the year.

The consensus was wrong.

The United States economy is outperforming the economies of the UK, Germany, France, Italy, Japan, and the entire euro area, showing estimates of economic growth that exceed those of the best-performing developed nations, along with significantly lower unemployment rates and solid real wage growth.

Due to exaggerated expectations of the impact of factors like new tariffs, global uncertainty, and the potential for persistently high inflation, most mainstream analysts and market commentators projected a stagnant or recessionary environment for the US in 2025, while hailing the euro area as the place to invest. We have seen the opposite.

US bond yields are falling, while euro area sovereign yields are rising despite ECB rate cuts. Additionally, GDP growth estimates for the euro area are weak, and US economic growth is stronger than the European Union’s “engines of growth,” whereas Japan and the UK remain stagnant. Inflation is under control, real wage growth is strong, and the private sector is improving.

The mainstream consensus predictions were biased and incorrect. Rather, the US economy has reported strong real GDP growth: following a short contraction in Q1, growth in the second quarter bounced back to 3–3.3% annually, and the Atlanta Fed’s GDPNow model currently projects Q3 growth at a stable 3% pace. In addition to consumer spending and imports, business investment also contributed to this GDP strength, and, more importantly, it came with government spending under control.

The most recent CPI and PPI data dispel concerns that the tariff regime is causing inflation. CPI and core measures in August came in close to or below expectations, indicating that headline monthly inflation and producer price increases are still under control. Prices for durable and nondurable goods are still stable, and, despite negative forecasts, tariffs have not generated a significant increase in the cost of living for Americans; instead, energy and important imports have either decreased or stabilized.

Despite recent revisions, the private-sector labor market maintained momentum from January through August. The significant negative revisions occurred during the January-December 2024 period, indicating that the Biden administration’s job creation was only half of what was reported and required a two million downward adjustment to the job figures from 2023 to 2024. What the Bureau of Labour Statistics has shown clearly is that the United States was in a private sector recession in 2024, which justified the negative sentiment from citizens.

Private payrolls have reported consistent net gains, particularly in the important service and construction segments, despite slight revisions to previous months. Even more encouraging is the fact that real wage growth is accelerating rather than merely keeping up with inflation. Real average hourly earnings increased by 1.2%, and real weekly earnings increased by 1.4% between July 2024 and July 2025. Increased purchasing power is boosting middle-class disposable income and driving retail demand because wage gains are outpacing price growth.

Retail sales also remain resilient in the face of market volatility and trade uncertainty. Bloomberg predicts that headline retail sales will increase by 0.2% in August, while the core control group will increase by 0.3%. This increase is significantly better than what April estimates showed, particularly since consumer sentiment is still cautious but generally stable. Throughout the third quarter, household consumption is increasing due to strong private labor markets and healthy wage growth.

The growing agreement that inflation risks are under control represents the most significant development for financial markets, paving the way for the Federal Reserve to finally recognize reality and cut interest rates in the coming months. Markets are beginning to anticipate that the Fed will soon lower interest rates, which could further boost borrowing, investment, and the economy’s momentum for the rest of 2025.

Despite the pessimistic predictions of recession and stagflation, they have proven to be undeniably wrong. The US economy is in a period of true private sector expansion, thanks to strong job and wage growth, favorable taxation, and deregulation, whereas tariffs are having no real impact on inflation. Now the Fed needs to be truly data dependent. Putting aside the pessimism of the previous year, the data currently indicates an improving outlook and a recovery from the private sector recession and fiscal mess inherited in 2024.

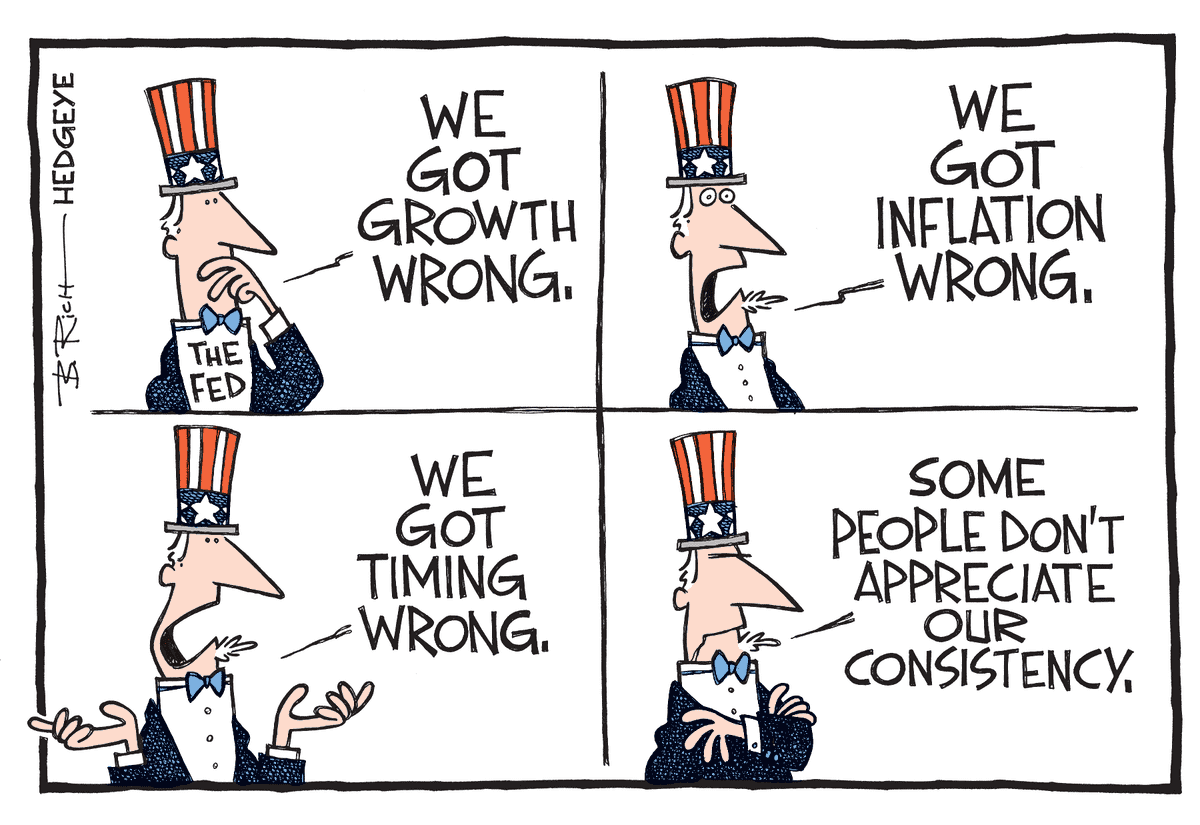

The Fed models were wrong about inflation and used labor market figures that were hugely inflated. The Fed should have read its own Beige Book, which alerted of a marked slowdown in job creation in March and April, instead of succumbing to the biased consensus narrative.

ABOUT DANIEL LACALLE

This is a Hedgeye guest contributor piece written by Daniel Lacalle and reposted from his website. Daniel Lacalle (Madrid, 1967). PhD Economist and Fund Manager. Author of bestsellers “Life In The Financial Markets” and “The Energy World Is Flat” as well as “Escape From the Central Bank Trap.” Daniel Lacalle (Madrid, 1967). PhD Economist and Fund Manager. Frequent collaborator with CNBC, Bloomberg, CNN, Hedgeye, Epoch Times, Mises Institute, BBN Times, Wall Street Journal, El Español, A3 Media and 13TV. Holds the CIIA (Certified International Investment Analyst) and masters in Economic Investigation and IESE. View all posts by Lacalle on his website.

Twitter handle: @dlacalle_IA

LinkedIn: Daniel Lacalle