This survey asks employers about the cost of single coverage and coverage for a family of four for up to two of their largest plans.

Health Insurance Premiums

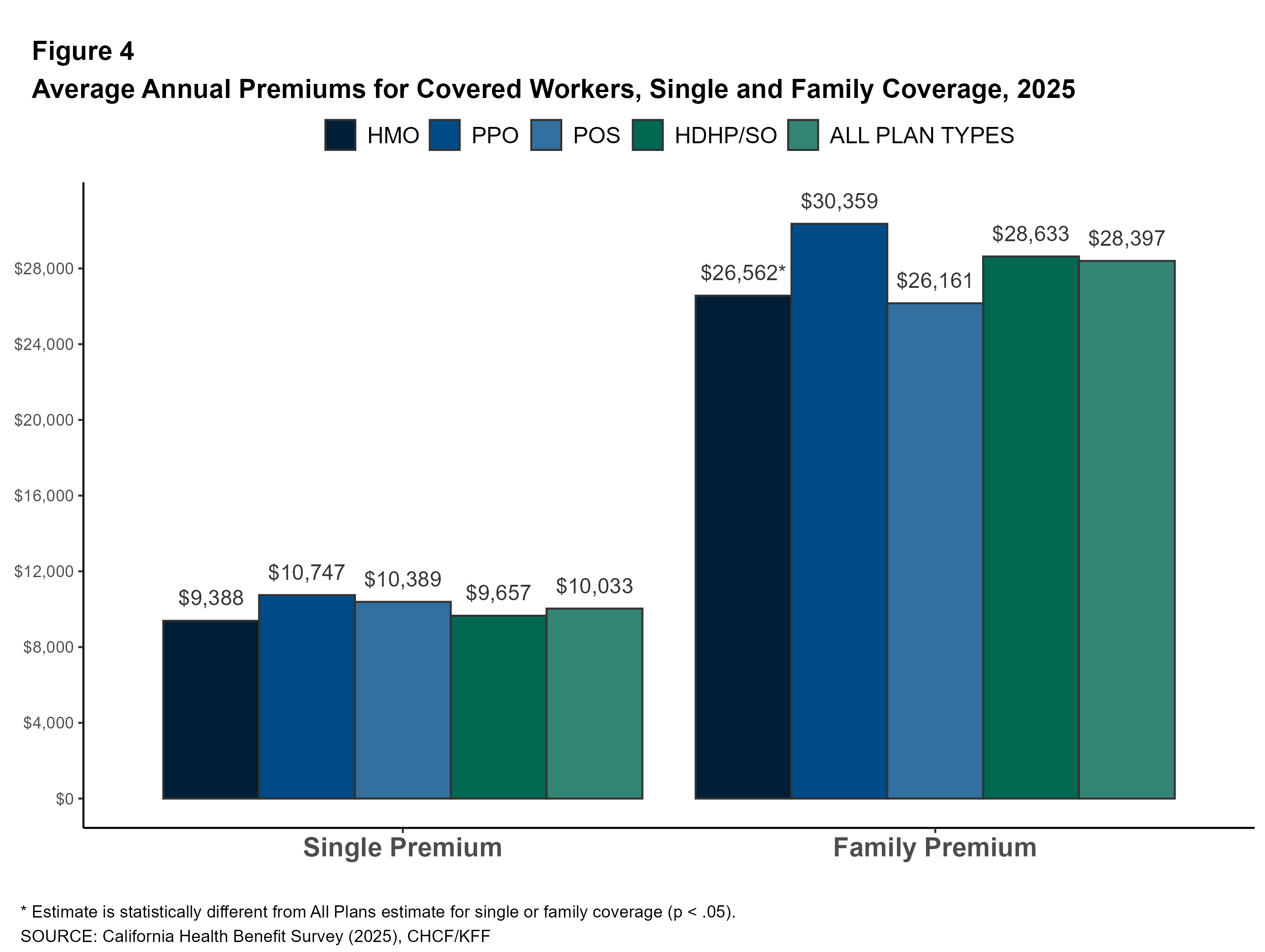

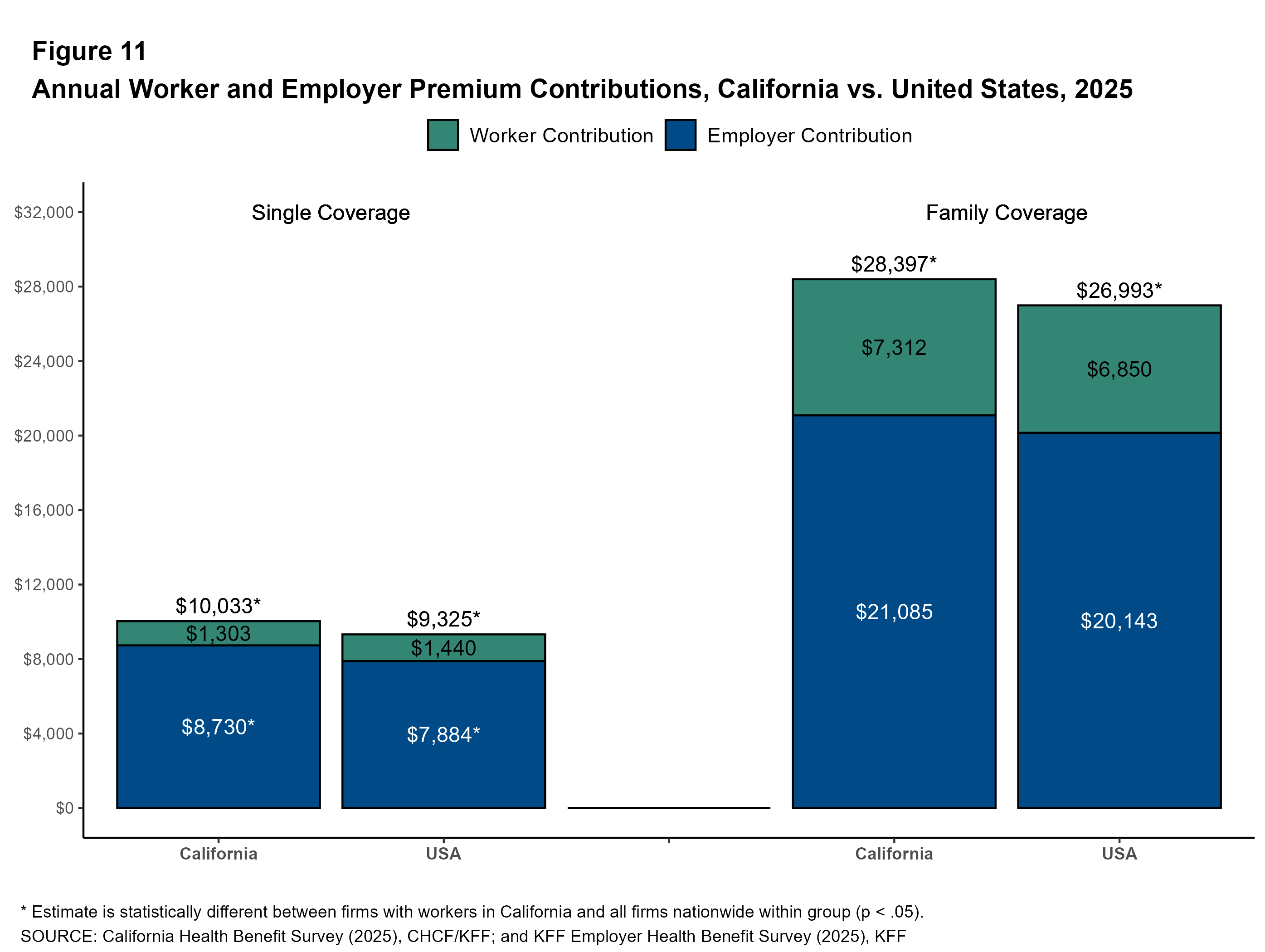

In 2025, the average premiums for covered workers in California are $10,033 for single coverage and $28,397 for family coverage. Premiums for covered workers in California are higher than for covered workers nationally for both single coverage ($10,033 vs. $9,325) and family coverage ($28,397 vs. $26,993).

Plan Type: Premiums vary by plan type. The average annual family premium for covered workers in HMOs is lower than the overall average ($26,562 vs. $28,397). Average premiums for covered workers in HDHP/SOs, including HSA-qualified plans, are similar to the overall average for both single and family coverage.

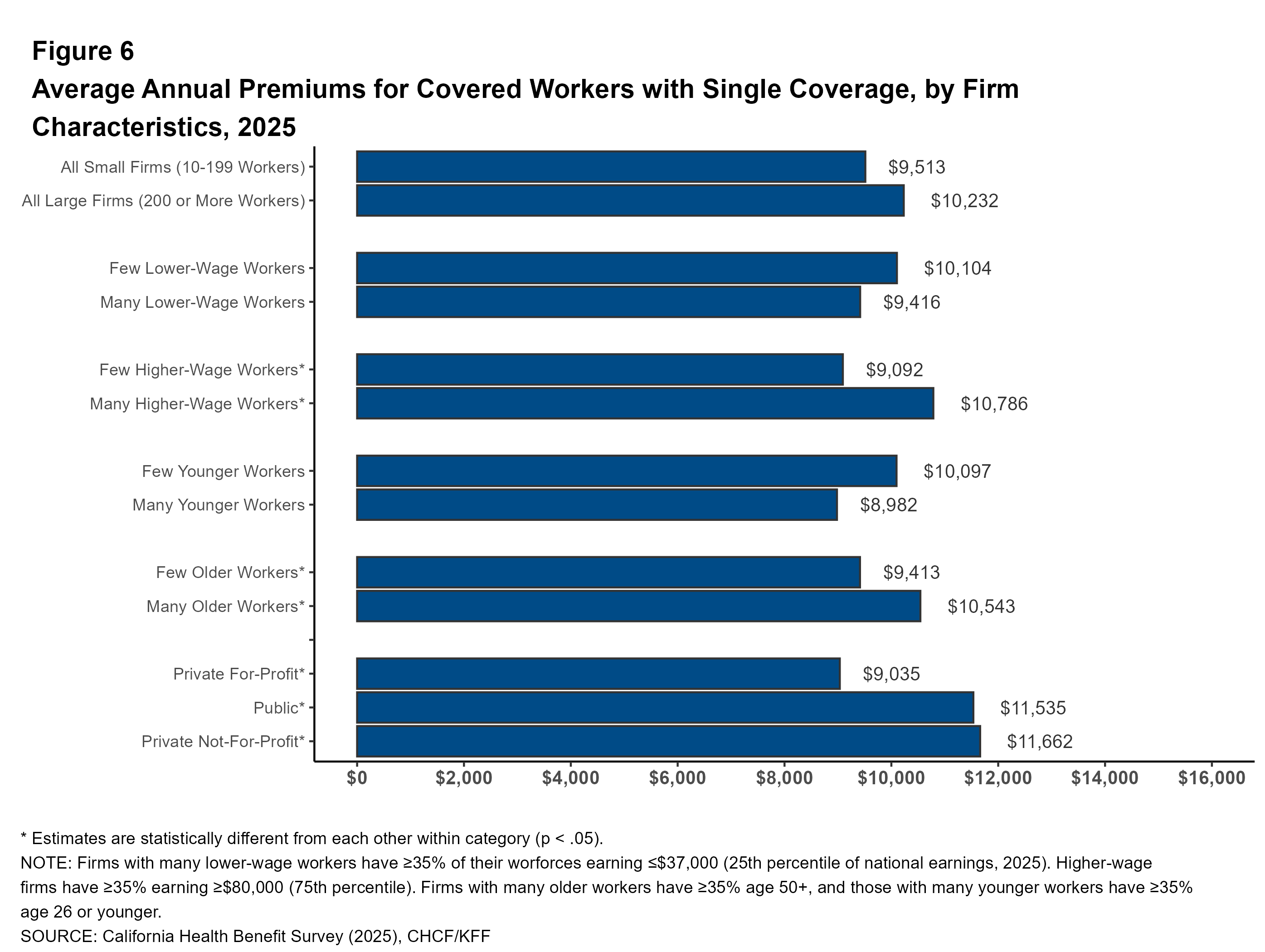

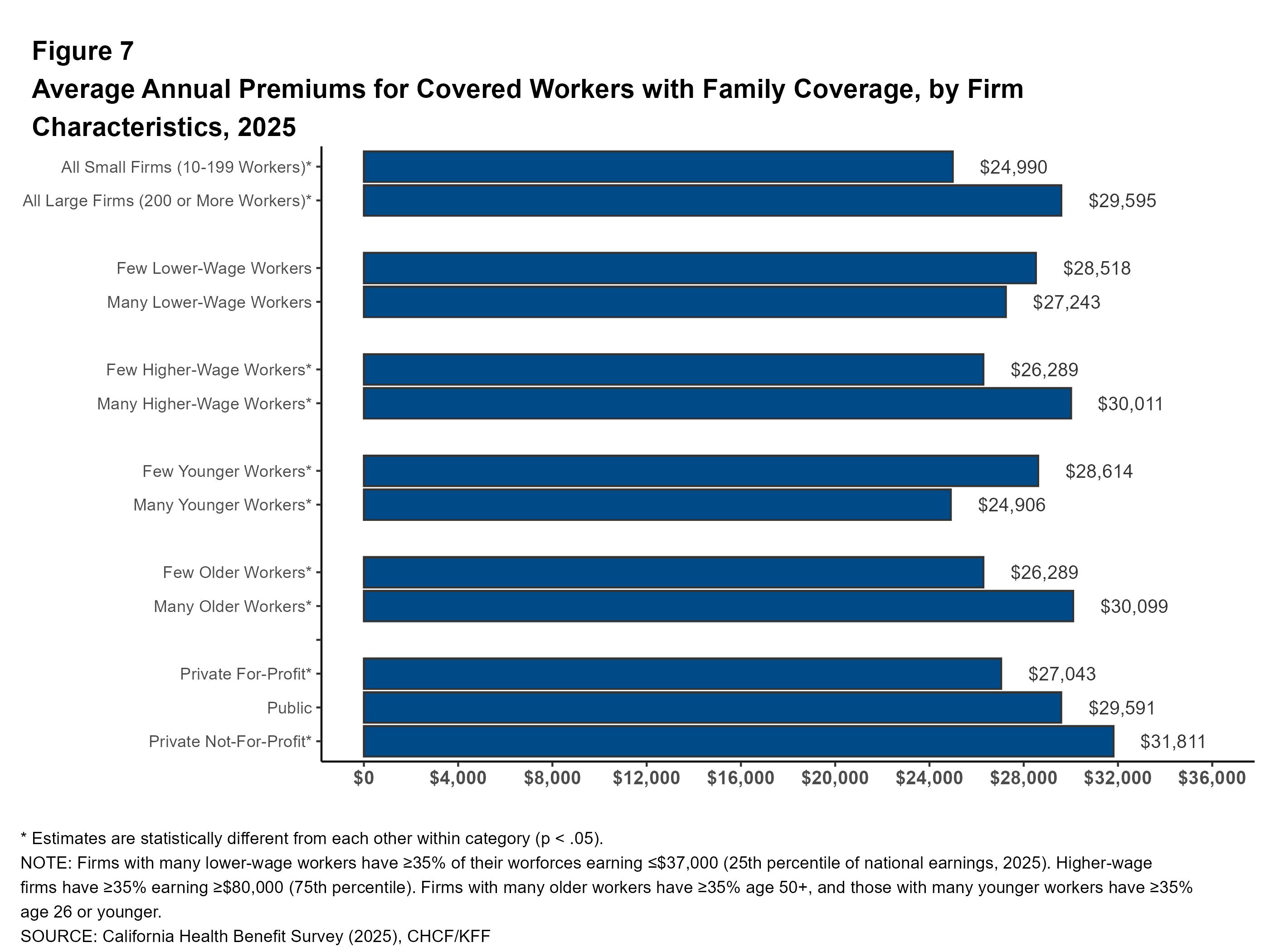

Firm Size: The average annual premium for family coverage is lower for covered workers at firms with 10 to 199 workers than for covered workers at larger firms ($24,990 vs. $29,595).

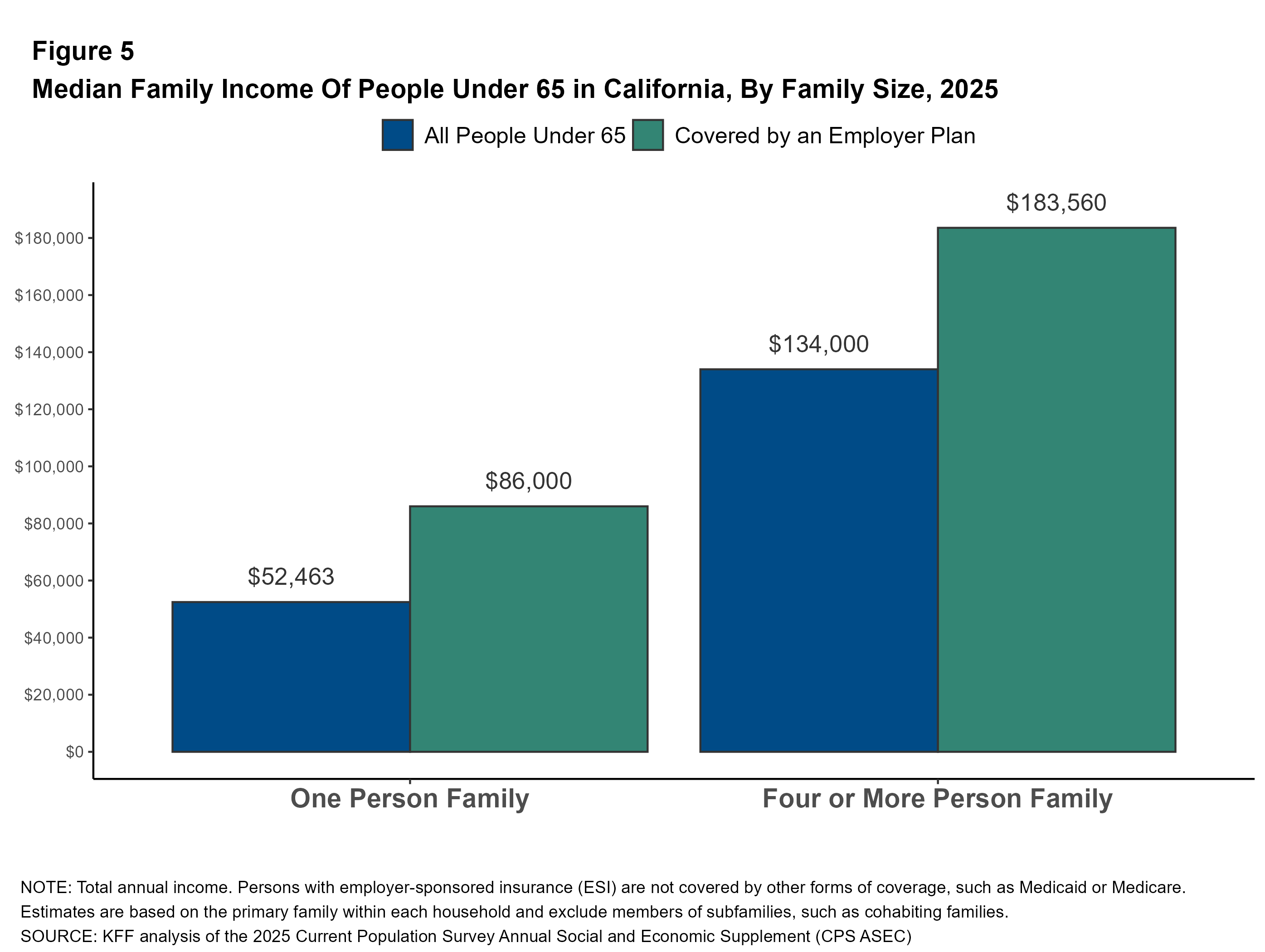

These premium amounts can be compared to the income of people with job-based coverage. In California, non-elderly individuals with employer-sponsored insurance who live alone have a median income of $86,000. Among families of four with employer-sponsored insurance, the median income is $183,560. Among all families of four, including those not enrolled in an employer plan, the median family income is $134,000.

Firm Characteristics: Premiums vary by the age of the firm’s workforce.

In California, the average premiums for covered workers at firms with large shares of younger workers (firms where at least 35% of the workers are age 26 or younger) are lower than the average premiums for covered workers at firms with smaller shares of younger workers for family coverage ($24,906 vs. $28,614).

In California, the average premiums for covered workers at firms with large shares of older workers (firms where at least 35% of the workers are age 50 or older) are higher than the average premiums for covered workers at firms with smaller shares of older workers for both single coverage ($10,543 vs. $9,413) and family coverage ($30,099 vs. $26,289).

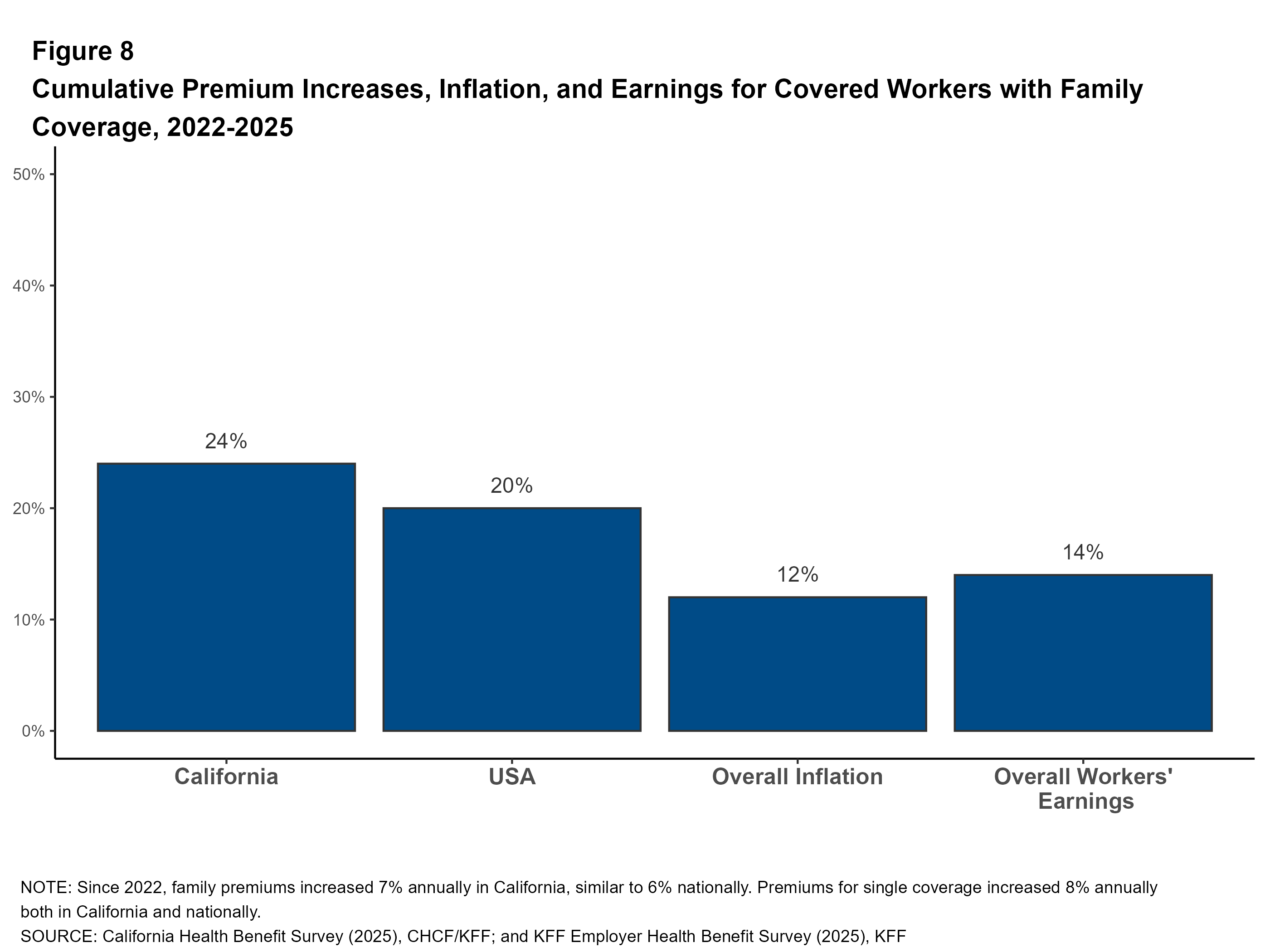

Premium Growth: Since 2022, family premiums have increased 7% annually in California, similar to the national overall increase of 6%. Premiums for single coverage increased 8% annually in California and 6% nationally. For comparison, the annual inflation rate over the period was 4% on average, and workers’ wages increased 5%. In the last year, there was an increase of 4% in workers’ wages, and inflation was 2.7%.

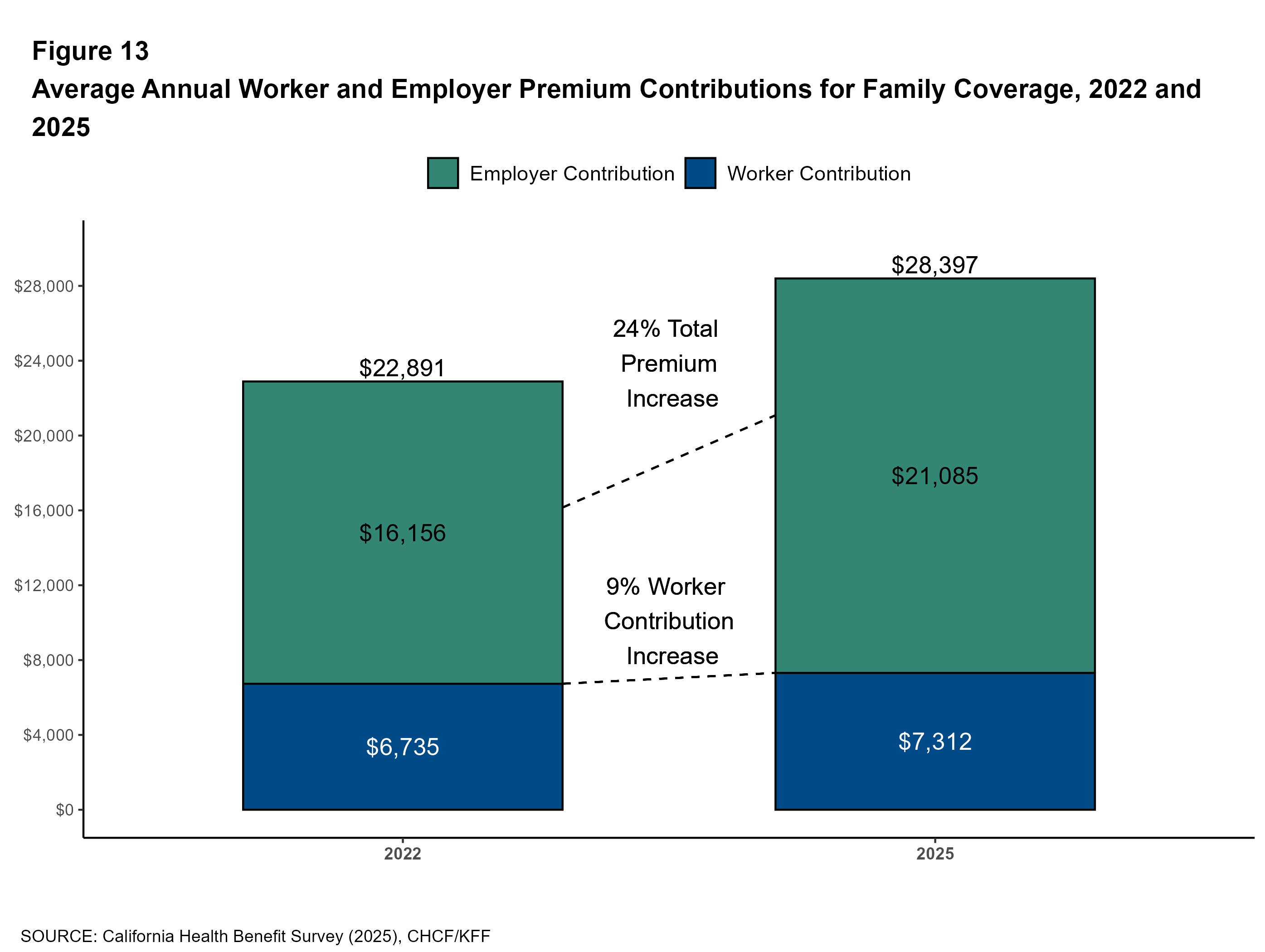

Since 2022, the average premium for family coverage has risen from $22,891 to $28,397, an increase of 24%, compared to inflation (12.2%) and wage growth (14.4%). In the years before the 2022 CHBS was fielded, the economy had experienced high general inflation. Since 2020, inflation has risen by 24%, much faster than the 10% increase between 2015 and 2020, or the 8% increase between 2010 and 2015.

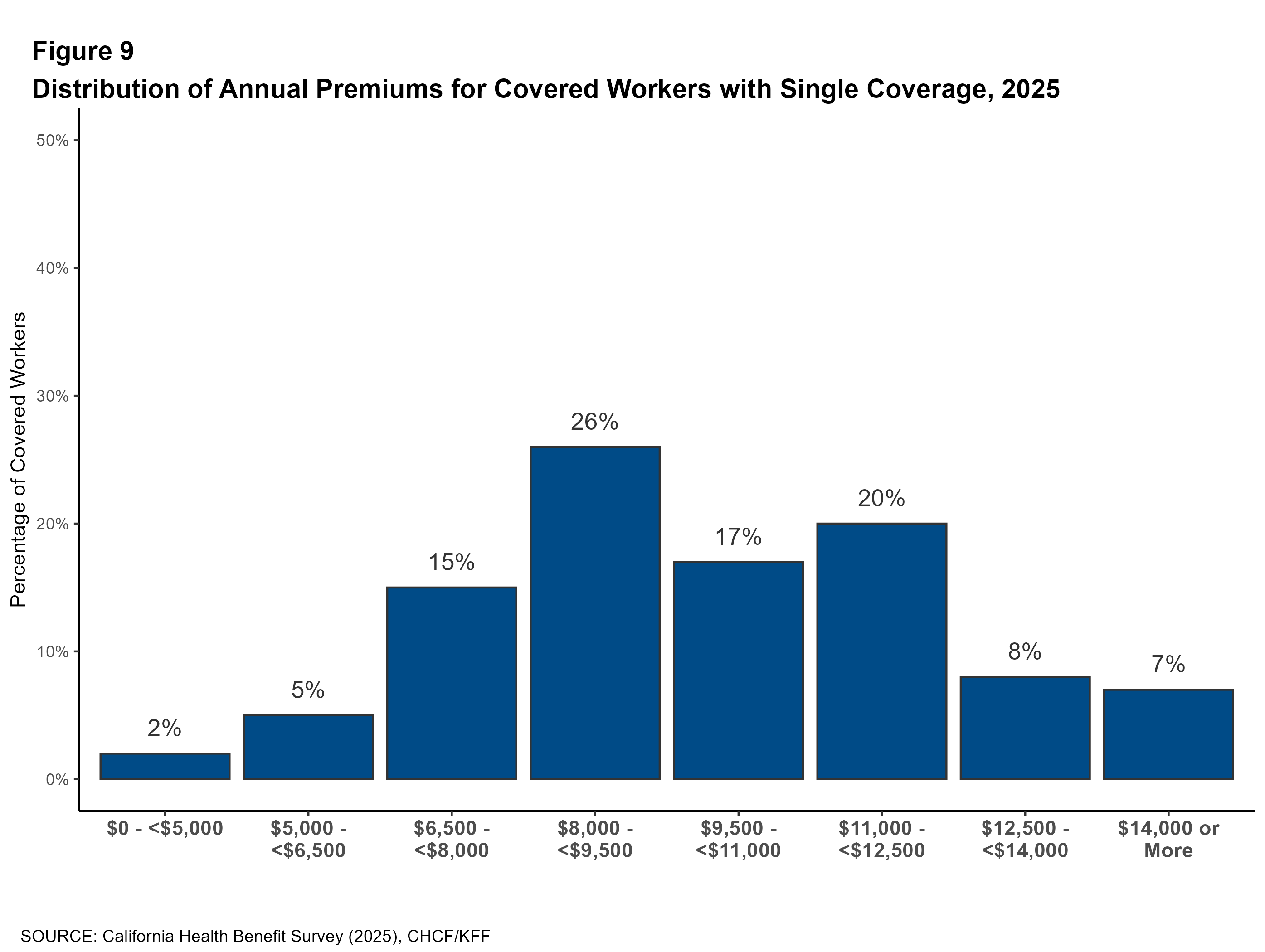

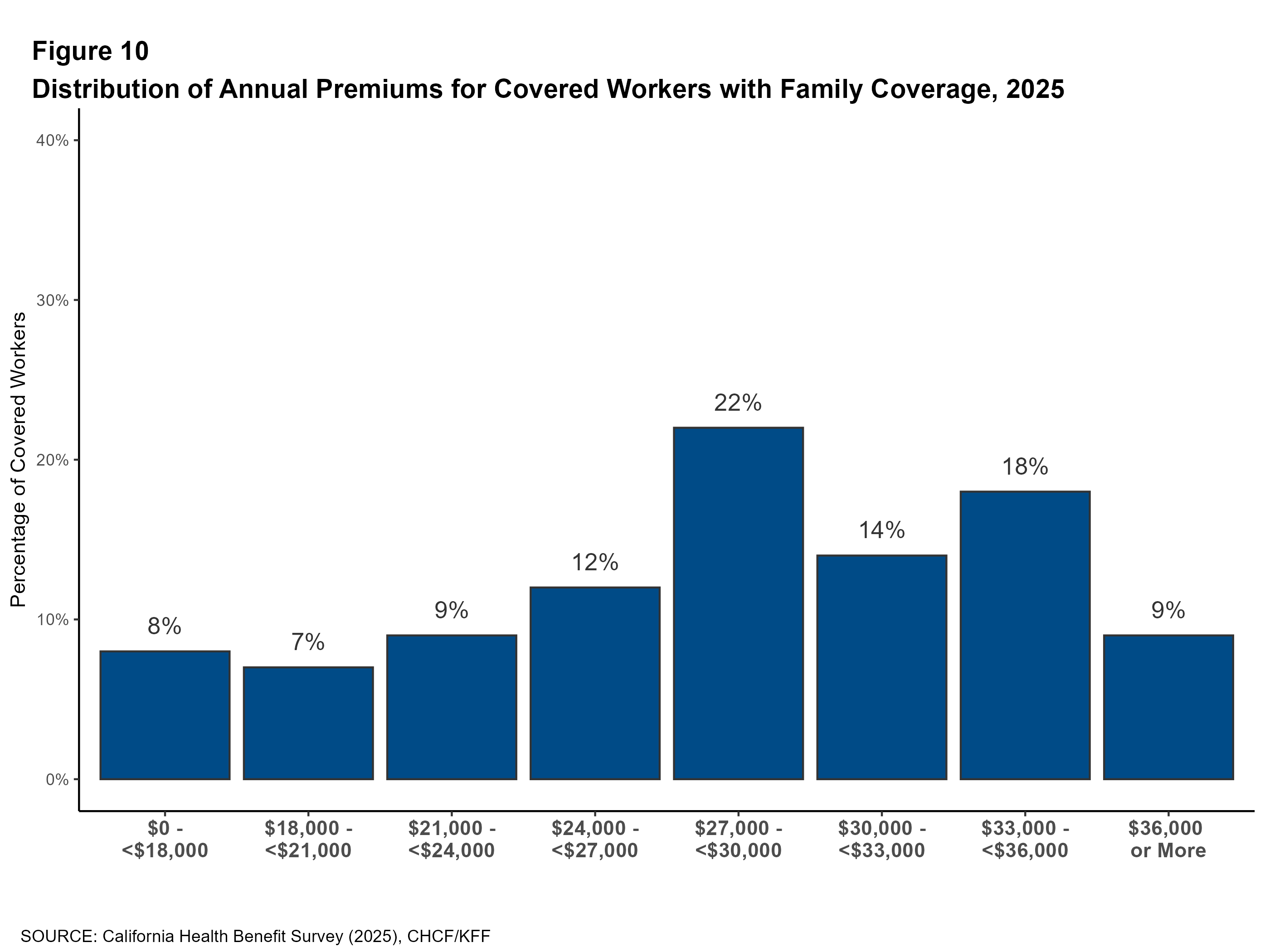

Distribution of Premiums: Premiums for family coverage in California vary considerably. Premiums are set based on a variety of factors, including the cost of providers in the network, the extent of covered benefits, the cost sharing structure, and the number of health services used by enrollees. Among California workers with single coverage, 15% are employed at a firm with an average annual premium of at least $12,500. Fifteen percent of covered workers are in a plan with a family premium of less than $21,000, while 27% are in a plan with a family premium of $33,000 or more.

Worker Contributions to the Premium

For many workers, health insurance is an important component of their total compensation. At the same time, most workers are required to contribute directly to the cost of their health insurance premiums, usually through payroll deductions. The average worker contribution for covered workers in California in 2025 is $1,303 for single coverage and $7,312 for family coverage. On average, covered workers in California contribute a similar amount to the national average to enroll in single or family coverage.

Employers contribute more to the cost of single coverage for covered workers in California than employers do nationally ($8,730 vs. $7,884).

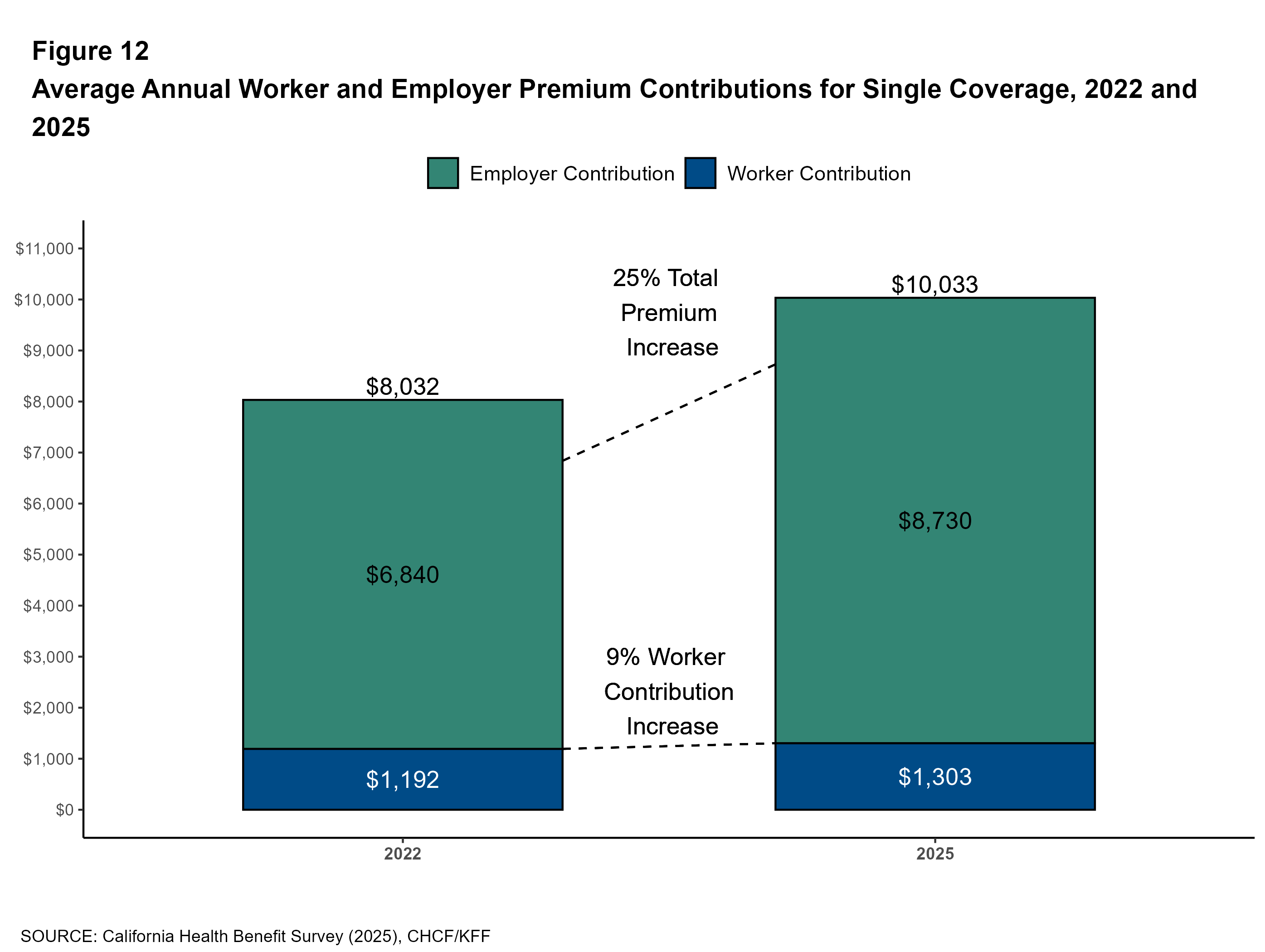

Change Over Time: Compared to 2022, California covered workers contribute a similar amount to enroll in single coverage ($1,192 vs. $1,303) and family coverage ($6,735 vs. $7,312). Since 2022, the average contribution for family coverage in California has increased by about 9%, or roughly 3% per year, but this does not represent a statistically significant change.

Firm Size: In California, the average family coverage premium contribution for covered workers in smaller firms (10 to 199 workers) is much higher than the average for covered workers in larger firms ($9,980 vs. $6,374).

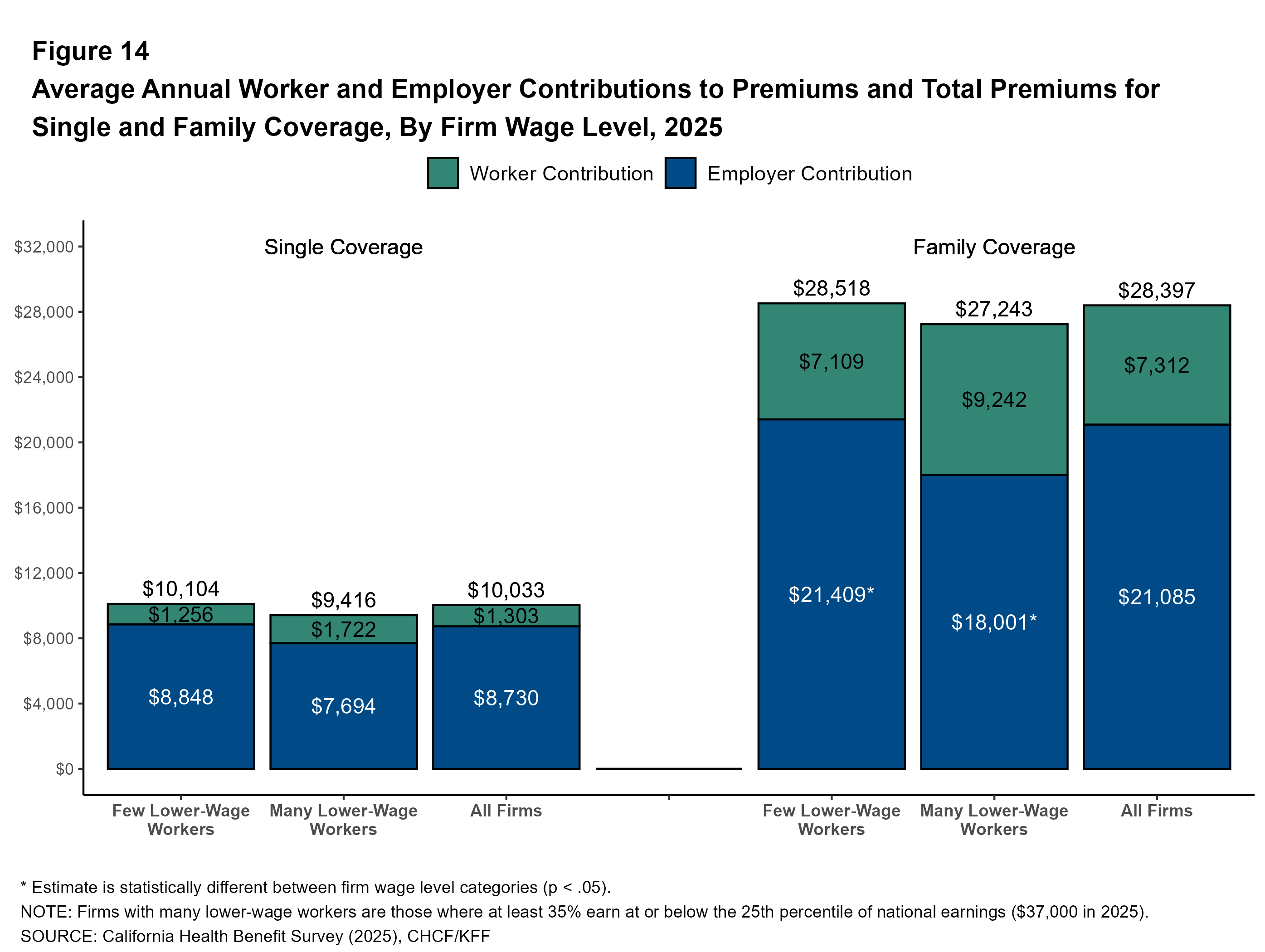

Firm Characteristics: In California, while the average premiums and worker contributions are similar between firms with a large share of lower-wage workers and those with fewer lower-wage workers, the average employer contribution differs. Firms with many lower-wage workers contribute less toward the cost of family coverage ($21,409 vs. $18,001).

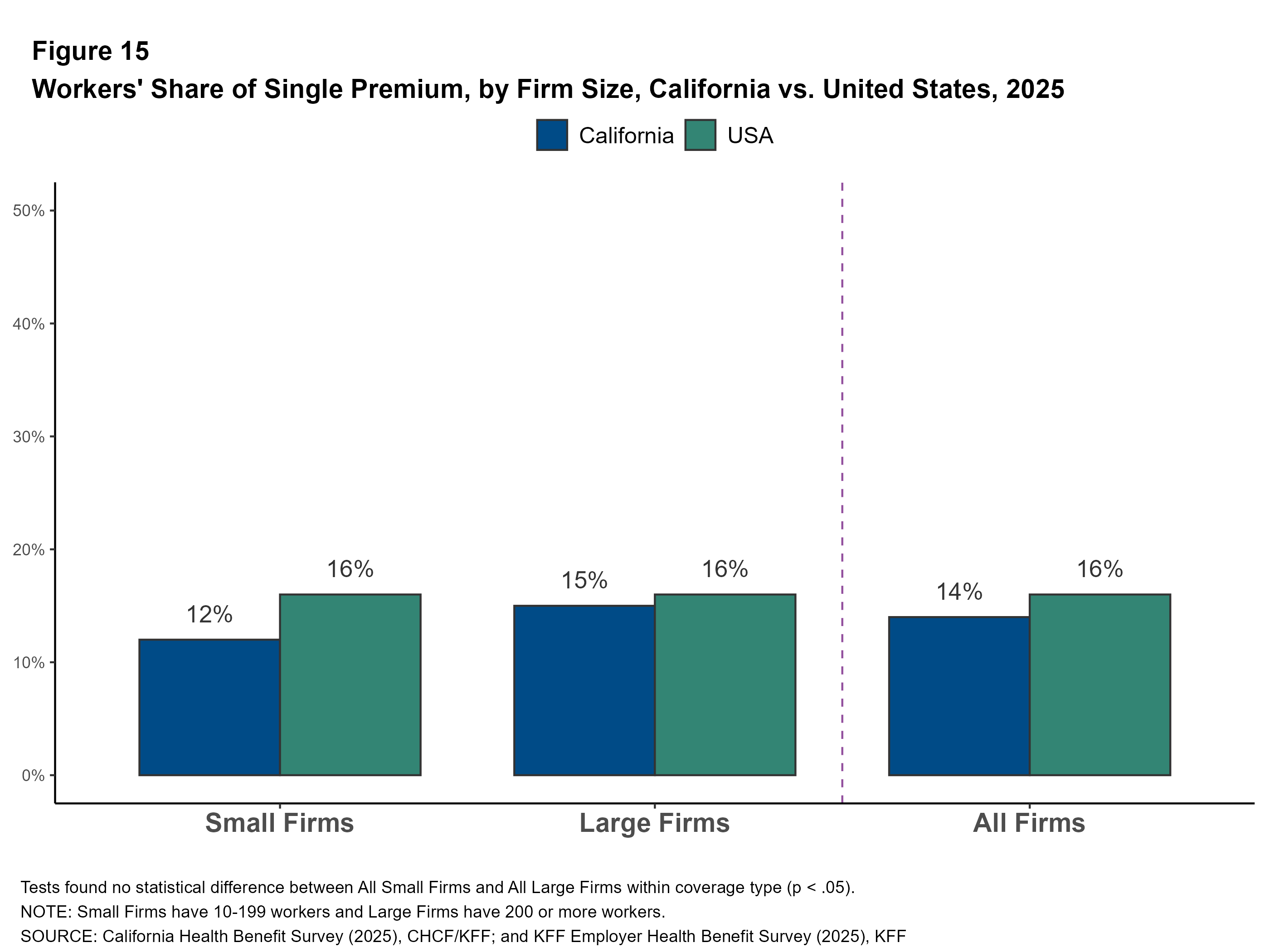

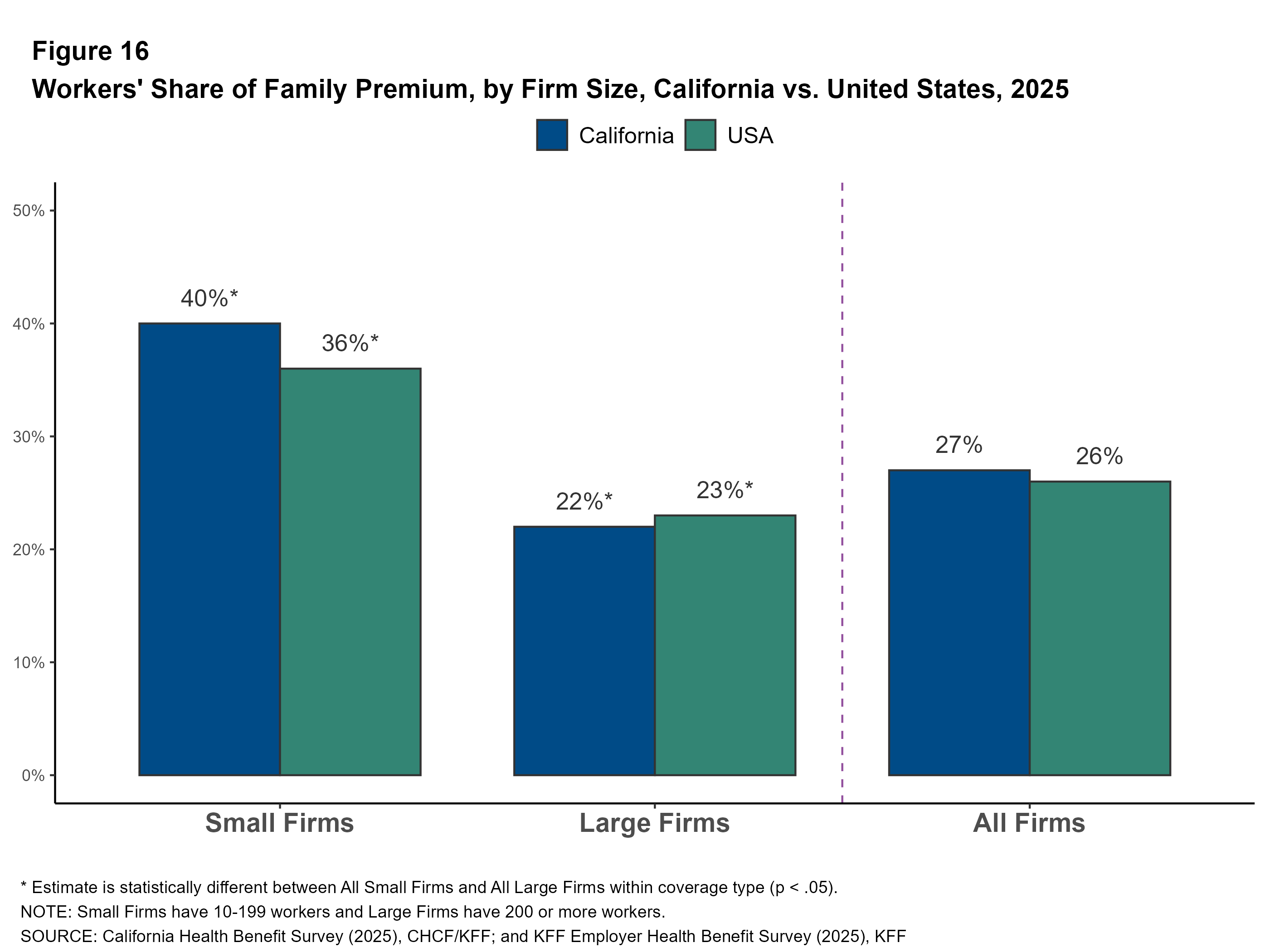

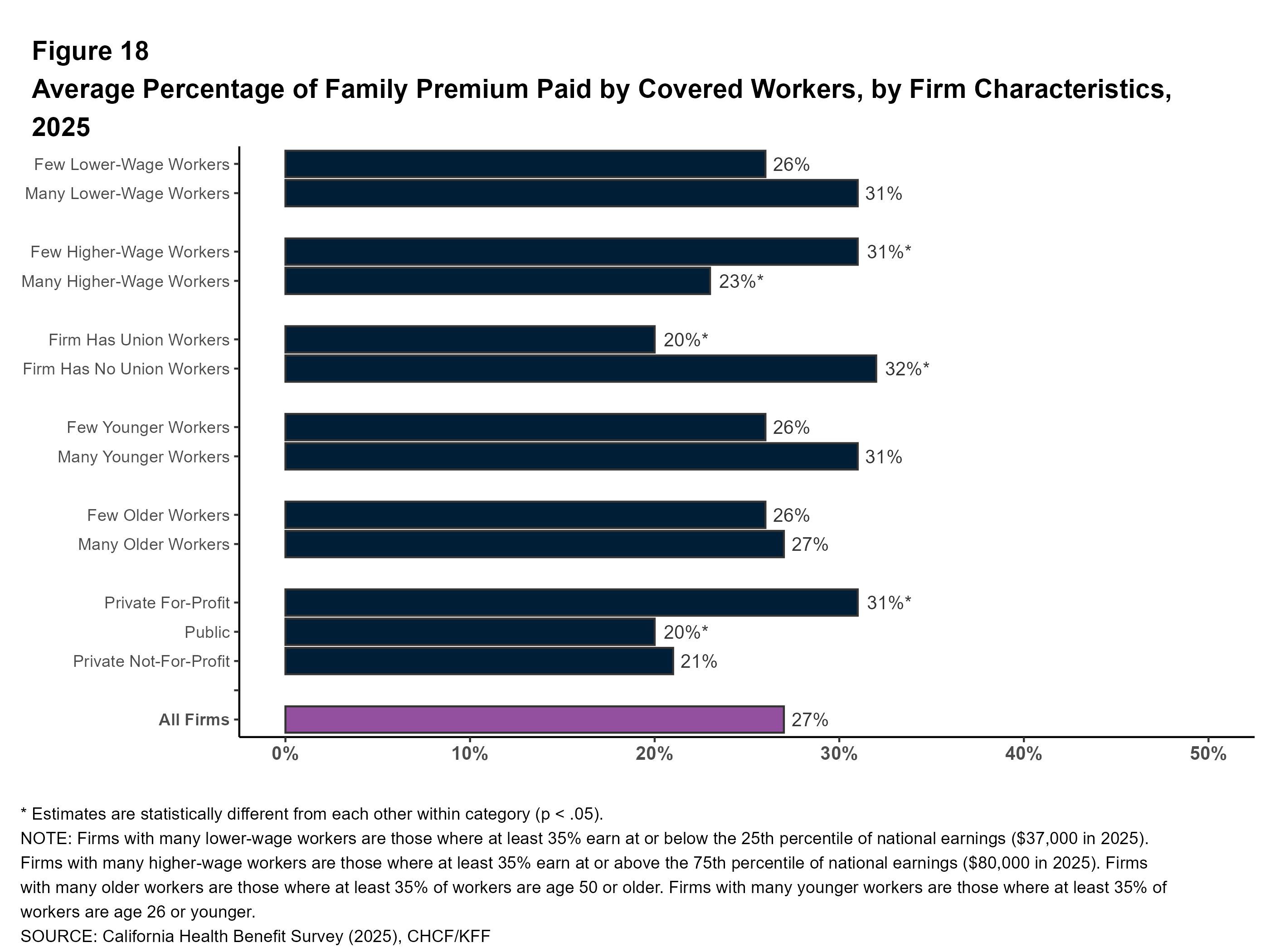

Share of the Premium Paid for by Workers: On average, covered workers in California contribute 14% of the premium for single coverage and 27% of the premium for family coverage, similar to the national averages.

Firm Size: Covered workers in California in small firms contribute a higher percentage of the family premium than those in larger firms, 40% vs. 22%.

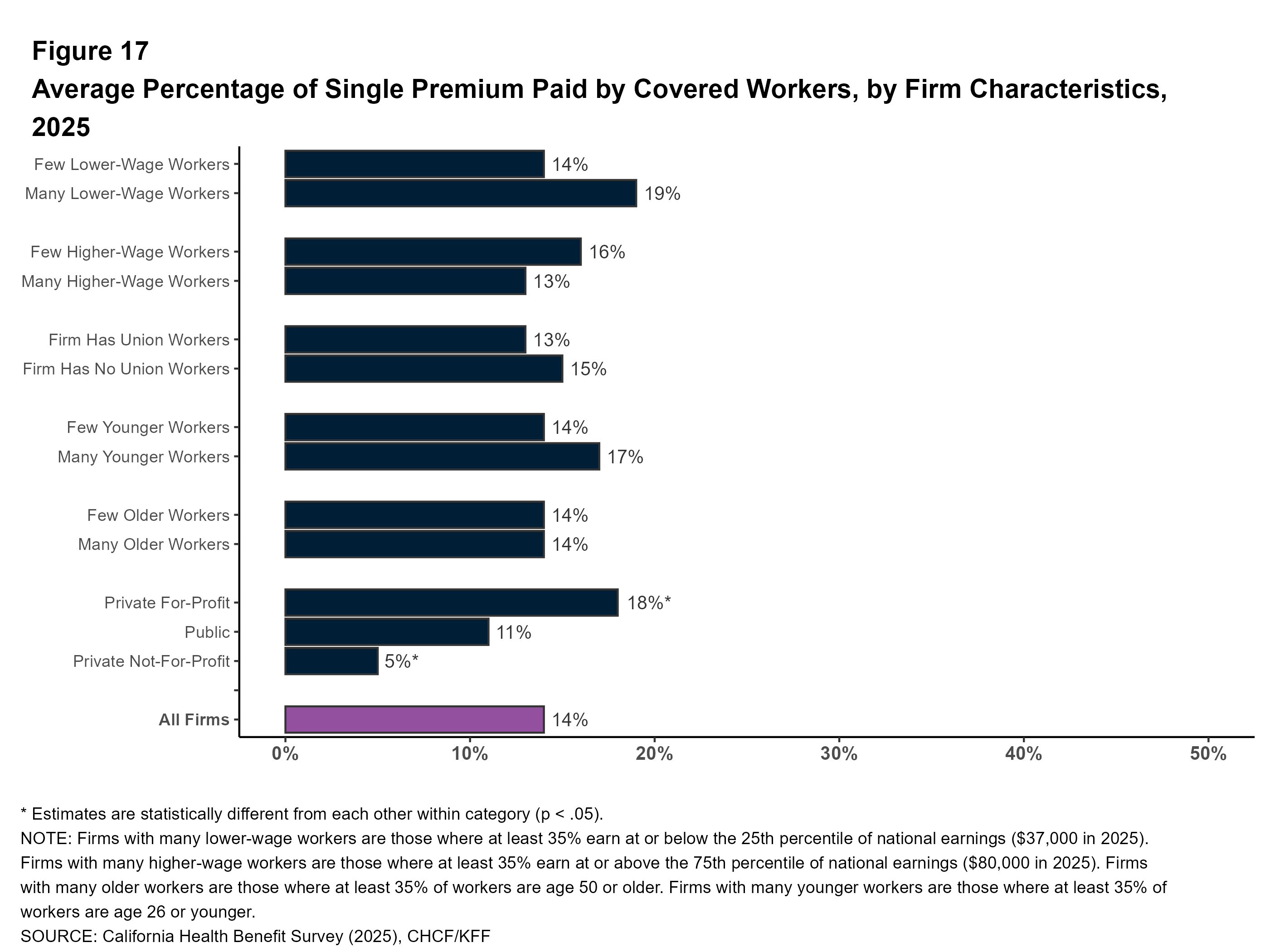

Share of the Premium Paid for by Workers by Firm Characteristics: The average share of the premium paid directly by covered workers differs across types of firms in California.

Covered workers in private, for-profit firms have relatively high average contribution rates for single coverage (18%) and for family coverage (31%) coverage. Covered workers in public firms have relatively low average premium contribution rates for family coverage (20%). Covered workers in private not-for-profit firms have relatively low average premium contribution rates for single coverage (5%).

Covered workers in firms with many higher-wage workers (where at least 35% earn $80,000 or more annually) have a lower average contribution rate for family coverage than those in firms with a smaller share of higher-wage workers (23% vs. 31%).

Covered workers in firms that have at least some union workers have a lower average contribution rate for family coverage than those in firms without any union workers (20% vs. 32%).

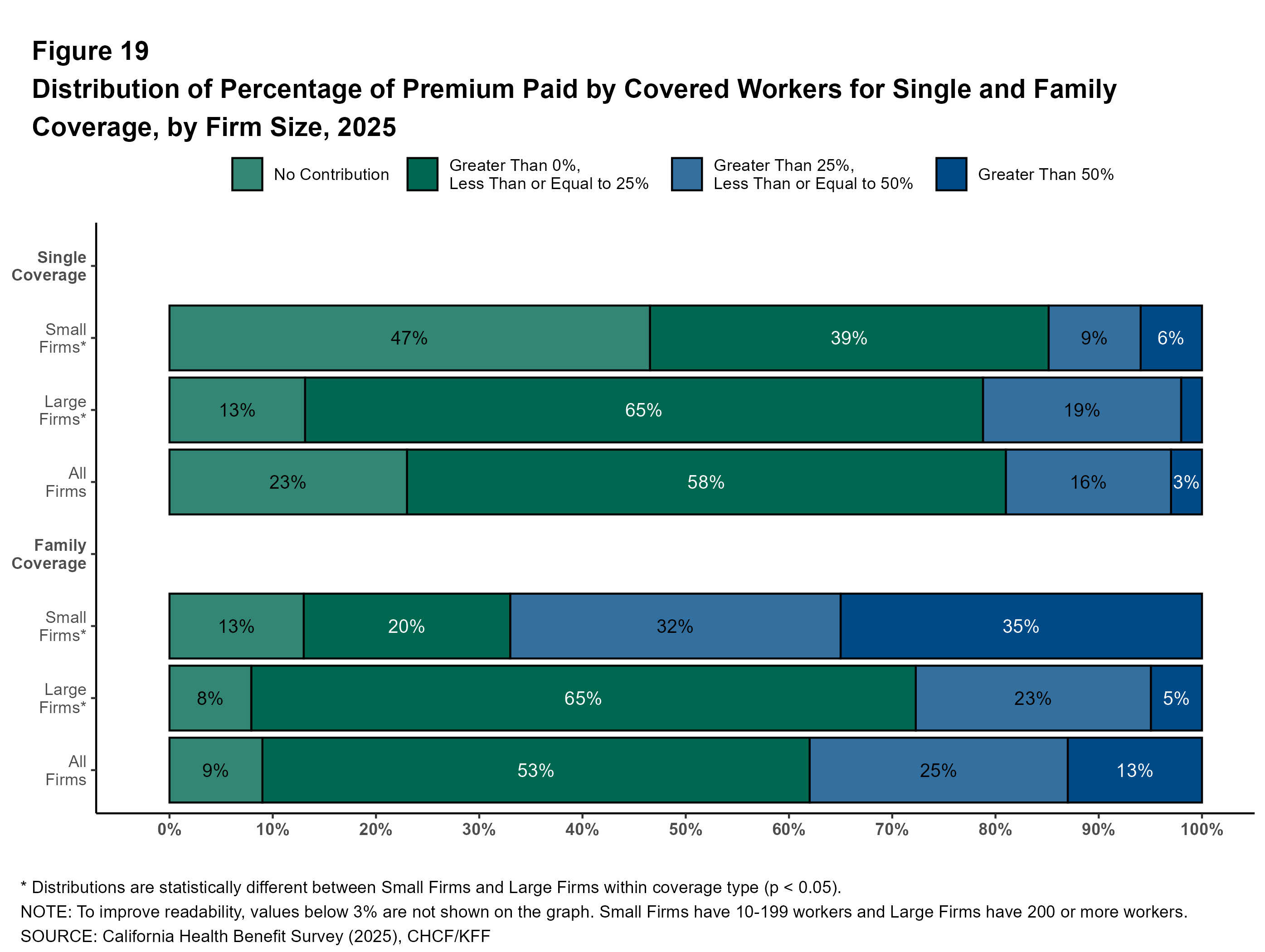

Distribution of Worker Contributions: In California, for single coverage, 47% of covered workers at small firms are enrolled in plans with no premium contribution, compared to only 13% of covered workers at large firms. For family coverage, 35% of covered workers at small firms are enrolled in plans with a worker contribution of more than half the premium, compared to only 5% of covered workers at large firms.

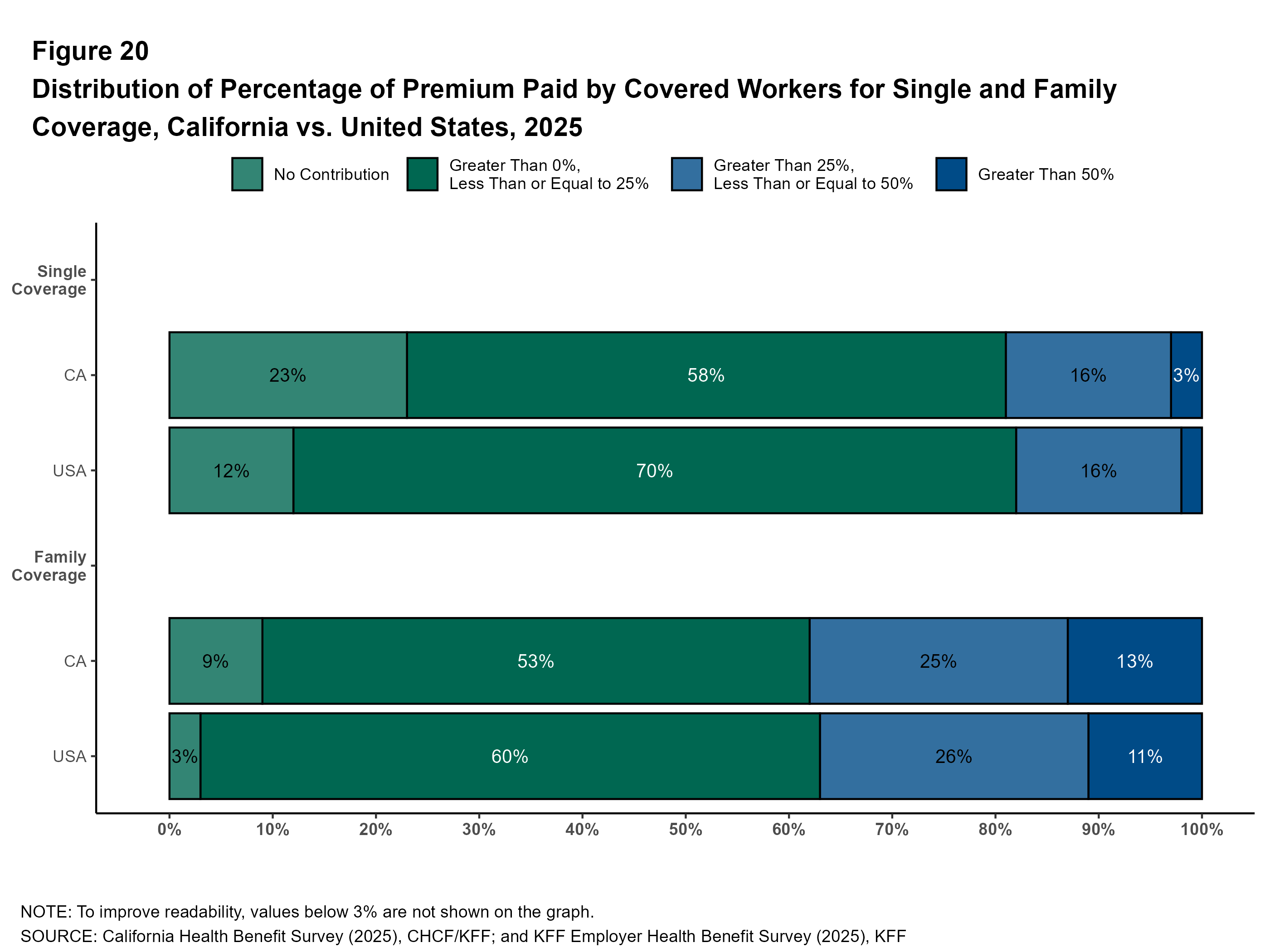

A larger share of covered workers in California are enrolled in a single coverage plan without a premium contribution than covered workers nationally (23% vs. 12%). This pattern also holds among covered workers at small firms (13% vs. 7%).

Another way to illustrate the high cost of family coverage for some workers is to examine the share of workers facing large annual premium contributions. Many workers at small firms encounter substantial costs if they choose to enroll dependents. Among firms offering family coverage, 38% of covered workers in small firms are enrolled in a plan with a premium contribution exceeding $10,000, compared to 12% of covered workers in large firms.