AMETEK (AME) has just released its 2025 Sustainability Report, detailing concrete steps forward on emissions reduction, operational efficiency, and sustainability initiatives. The company reports a 33% drop in greenhouse gas intensity, which is well ahead of its 2035 target.

See our latest analysis for AMETEK.

While AMETEK’s leadership on sustainability has made headlines, the stock itself has been quietly resilient, clocking a 1-year total shareholder return of -0.54%. It also boasts impressive long-term momentum with a 39.5% total return over the past three years and 68.2% over five years. The latest 5.45% share price gain in the past month hints that momentum could be returning, especially as efficiency gains and emissions progress get noticed.

If AMETEK’s progress has you watching for the next standout, now’s a smart time to broaden your scope and discover fast growing stocks with high insider ownership

With shares currently trading near all-time highs and still at a 13% discount to analysts’ targets, the real question is whether the market is overlooking AMETEK’s upside or if future growth is already fully priced in.

Most Popular Narrative: 11.3% Undervalued

AMETEK’s most widely followed narrative assigns a fair value of $219.94 per share, suggesting notable upside from the last close at $195.02. The stage is set for a debate on what exactly is fueling this optimism, especially given recent operational tailwinds and a resilient share price.

Adoption of digital reality, automation, and advanced metrology solutions is accelerating across key end markets such as aerospace, defense, and architecture. This has been recently reinforced by the FARO Technologies acquisition, which expands AMETEK’s addressable market and supports both revenue and margin growth through higher value, software-enabled recurring revenue streams. Growing global focus on sustainability and energy efficiency, alongside regulatory requirements across sectors, is driving long-term demand for high-precision analytical and monitoring instrumentation, favoring AMETEK’s portfolio and supporting steady revenue and market share gains.

Curious what underpins that bullish target? One key assumption in this narrative is a bold leap in recurring revenues and profitability. Want to see what projections shape this valuation and how AMETEK’s momentum stacks up against Wall Street’s expectations? Dive into the full narrative for the numbers and the tension you won’t want to miss.

Result: Fair Value of $219.94 (UNDERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, persistent weakness in key end markets or challenges integrating recent acquisitions could significantly undermine the positive outlook analysts have outlined for AMETEK.

Find out about the key risks to this AMETEK narrative.

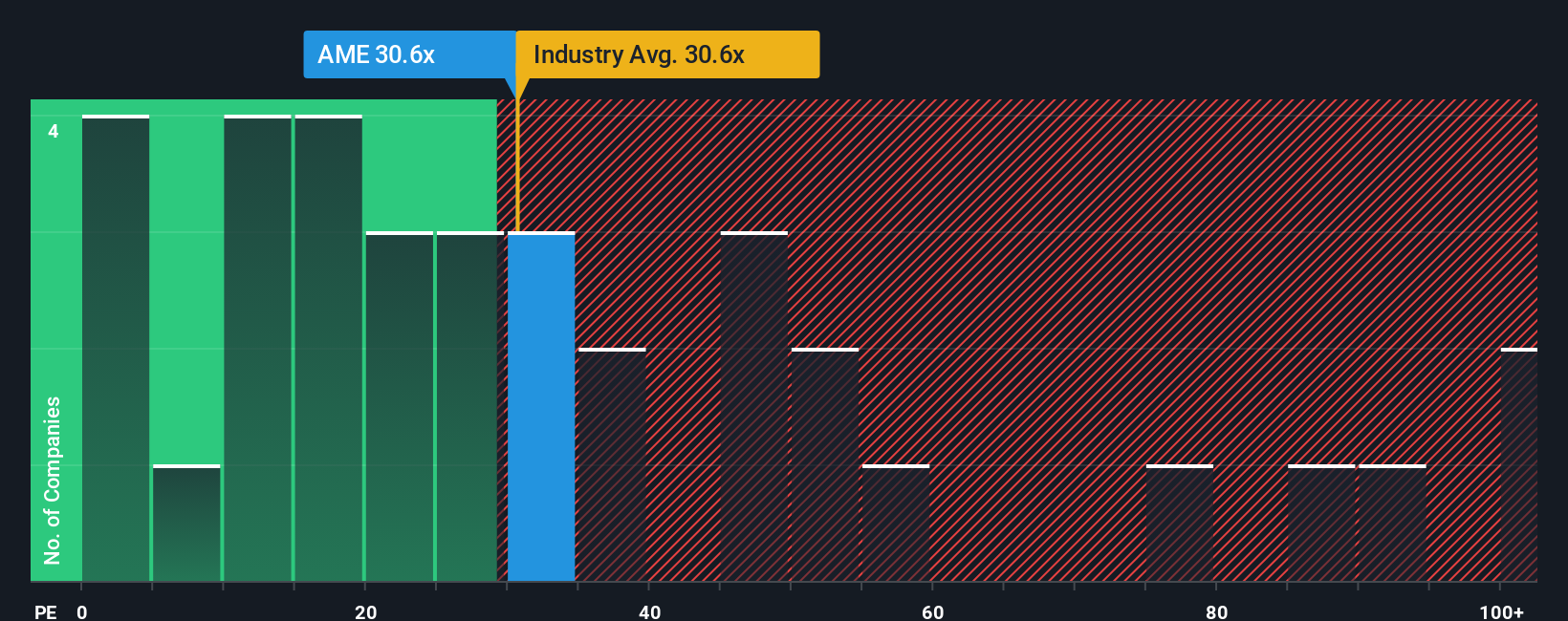

Another View: Multiples Tell a Cautious Story

Taking a look at the company’s price-to-earnings ratio, AMETEK is trading at 30.6x, which is above both the US Electrical industry average of 28x and its own fair ratio of 25.1x. This suggests that in today’s market, AMETEK might be priced for more growth than what it could realistically deliver if market sentiment turns. Could there be more valuation risk here than the 11% discount to fair value implies?

See what the numbers say about this price — find out in our valuation breakdown.

NYSE:AME PE Ratio as at Nov 2025 Build Your Own AMETEK Narrative

NYSE:AME PE Ratio as at Nov 2025 Build Your Own AMETEK Narrative

If the numbers or narratives here don’t quite fit your perspective, you can dig into the data and build your own view in just minutes. Do it your way

A great starting point for your AMETEK research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Smart investors seize the best opportunities early. Don’t hold back when the next winning idea might come from a space you haven’t checked yet. Plug into more potential now:

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com