Both Germany and the United States boosted retirement benefits in 2025. Only Germany adopted a commission to fix the damage. German lawmakers recently passed a reform package that overrides the sustainability factor—a stabilizer that slows benefit growth in the Statutory Pension Insurance (a payroll tax-financed old-age program like Social Security) as demographics worsen. The new law fixes benefit levels relative to average wages through 2031. Although the sustainability factor resumes after 2031, benefits will remain permanently elevated than under the prior law. Eighteen younger CDU/CSU lawmakers opposed the €200 billion package, arguing the cost through 2040 “cannot be justified to the younger generation.” To secure their support, Chancellor Friedrich Merz pledged to adopt the recommendations of an expert commission in 2026. The 13-member commission includes three Bundestag members, a former government official, and nine experts, tasked with developing reform proposals for Germany’s broader retirement system. The US Congress boosted benefits twice this year—first through the so-called Social Security Fairness Act and then the One Big Beautiful Bill Act (OBBBA)—both of which worsened Social Security’s finances. Unlike in Germany, there was no debate over generational fairness or a commitment to an expert-led commission. Congress should form a fast-track, expert commission to address Social Security’s shortfalls and stabilize the US debt. Seventy-one percent (71 percent) of Americans favor such an approach.

CBO should report federal spending for people age 65 or older. As the US population continues to age, spending for people age 65 and older is consuming a growing share of the federal budget. In 2005, such spending made up 35 percent of federal non-interest outlays, rose to roughly 40 percent by 2018, and was projected to reach 50 percent by 2029, according to the Congressional Budget Office’s (CBO) Budget and Economic Outlook: 2019–2029. That report provided a comprehensive, program-level breakdown of federal spending for older Americans, extending beyond Social Security, Medicare, and Medicaid to include pension and health benefits for retired military and civilian employees of the federal government, veterans’ disability compensation, Supplemental Security Income, SNAP/food stamps, housing assistance, and other programs with significant spending on the elderly. Such detailed accounting was an outlier, with subsequent Long-Term Budget Outlook reports only addressing this issue in the context of Social Security, Medicare, and Medicaid. The COVID-19 pandemic accelerated retirements, potentially shifting both the level and composition of age-related federal spending earlier than projected. Congress should direct CBO to routinely update federal spending for people age 65 or older so lawmakers have a clearer view of how population aging and age-dependent benefits are affecting federal spending, deficits, and debt.

Trump’s “state corporatism” is Republican socialism. Reason’s Eric Boehm says Trump is “on a shopping spree” with “a nearly unlimited supply of someone else’s money,” buying equity stakes in “more than a dozen private companies […] without even an attempt at getting congressional authorization.”Cato’s Scott Lincicome explains that a “direct and permanent financial stake” differs from subsidies “offered broadly, provided at arm’s length, and authorized by law” because it makes government care about a firm’s “ultimate success or failure.” It also invites “repeated, open-ended, non-crisis interventions.” Lincicome warns of “a troubling future across multiple fronts. The problems and distortions associated with state corporatism—cronyism, favoritism, inefficiency, capital misallocation, etc.—will proliferate, often without notice. State champions will double down on their relationship with the government and the short-term advantage it provides. (Some, in fact, have already started.) There’s also a clear risk that more U.S. firms join with the government out of fear or necessity, and that future administrations will use this year’s precedents to implement their own versions of state corporatism—distorting more of the American economy along the way.”

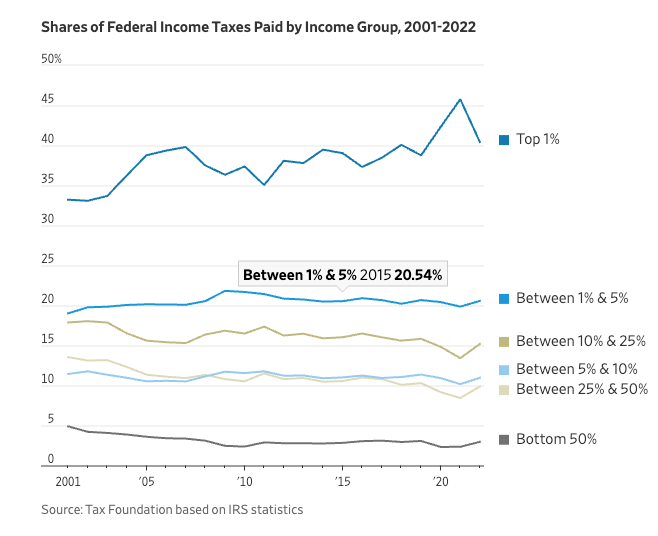

Taxing the rich does not fix the government spending problem. The WSJ pushes back against the common sentiment, now expressed by Mitt Romney, who says, “And on the tax front, it’s time for rich people like me to pay more.” WSJ shares a graph from the Tax Foundation showing the rich already pay a disproportionately large share of total taxes: “As a share of total adjusted gross income reported in 2022, the top 1% earned 22.4%, but they paid 40.4% of total income taxes. They paid in taxes nearly double their share of income. The top 10% earned 49.4% of total AGI but paid 72% of total income taxes.” WSJ points to the real issue: “The U.S. has a federal debt problem, and entitlement reform is essential. It will happen because sooner or later lenders will demand it.” Cato’s Adam Michel explains why taxing the rich cannot be the solution: “Proposals to increase taxes only on high-income Americans are neither a mathematically nor economically feasible mechanism to raise significant amounts of new revenue.” Without spending reforms, “the country is currently headed toward a European-style welfare state that requires significantly higher taxes on all Americans. Funding a European-style welfare state would require a roughly 50 percent tax increase on lower- and middle-income American workers and families.”

Depreciation of the yen should serve as a warning for the US. Brookings’ Robin J. Brooks comments that “the Yen is down to its lowest level in over 20 years, tumbling below the low it made mid-2024 when Japanese interest rates were much lower.” Brooks reveals “the uncomfortable truth: Japan’s longer-term yields have been rising, but – on a risk-adjusted basis – that rise isn’t nearly enough to stabilize the Yen. Another way to say this: markets think risk of a debt crisis is rising sharply. Yen depreciation won’t stop until yields are allowed to rise far more, forcing the government to pursue fiscal consolidation and bring down debt.” As for the situation in the US, Davide Barbuscia reports: “Reuters spoke to more than a dozen executives at banks and asset managers overseeing trillions of dollars in assets who said that beneath the relative calm of bond markets in recent months a battle of wills is playing out between the administration and investors concerned about the persistently high U.S. deficit and debt levels.”