Executive Summary: The Defining Economic ChallengeCritical Finding

Tanzania’s informal sector has transformed from an economic shock absorber into a structural vulnerability. With 44.9% of GDP and 84% of employment concentrated in informal activities, the country faces mounting fiscal pressures, productivity constraints, and exposure to economic shocks that could trigger crisis-driven formalization without proper preparation.

For decades, Tanzania’s informal economy served as a critical buffer, absorbing surplus labor and sustaining household incomes amid structural economic transitions. Today, this same sector represents one of the nation’s greatest transformation challenges. As nearly 900,000 young people enter the labor market annually—far exceeding formal sector absorption capacity—the question is no longer whether formalization will occur, but whether it will be managed or crisis-driven.

The Transformation Imperative

Tanzania’s economy continues to grow at a robust pace of 5.5-6.0% annually, yet this growth masks deep structural imbalances. Tax revenues remain stuck at 13.3% of GDP, below both the national target of 14.1% and the Sub-Saharan African average of 16.1%. With a growing budget of TZS 57 trillion and persistent deficits around 3.0% of GDP (with risks of widening to 3.5%), the fiscal squeeze is intensifying.

The next 5-10 years are decisive. Without immediate action on skills development, infrastructure investment, simplified taxation, and social protection, Tanzania risks a forced transformation scenario by 2035-2040 that could trigger mass unemployment, social instability, and economic contraction before recovery.

Current State of Tanzania’s Informal EconomyComparative Analysis: Tanzania vs. Global TrendsIndicatorTanzania (2025)Global AverageSSA AverageGap AnalysisInformal Economy % of GDP44.9%11.8%~35-40%+33.1 pp above globalInformal Employment Rate84%~60%~85%Aligned with SSATax-to-GDP Ratio13.3%~18%16.1%-2.8 pp below regionGDP Growth Rate6.0%~3.5%~4%Above regional averageKey Economic Indicators (2013-2025)Metric2013202020242025 (Proj.)TrendInformal Economy % of GDP~55%~48%~45%44.9%↓ Declining slowlyReal GDP (USD billion)~35~6482-85~88↑ Strong growthTax Revenue % of GDP~11%11%12.8%13.3%↑ Gradual increaseInformal Employment %~85%~84%84%84%+→ PersistentBudget Deficit % of GDP~4%~3.5%3.4%3.0%↓ ImprovingCritical Insight: The Labor Market Mismatch

900,000 young Tanzanians enter the labor market annually, yet the formal sector creates only a fraction of the needed jobs. This structural gap forces 84% of workers into informal activities characterized by:

Low and unstable incomesLimited productivity growth potentialNo tax contributions to public servicesMinimal social protection coverageSkills mismatch with modern economy needsDar es Salaam’s Informal Sector ConcentrationIndicatorValueYearSignificanceInformal Sector ContributionTZS 6.2 trillion2019Urban economic driverTax Collection Concentration70%2025Collected in Dar despite 70% GDP outsideFood Import Dependency>50%CurrentSunflower oil and key staplesPrice Shock Timeline24-48 hoursCurrentDisruption to nationwide impactTax Revenue and Fiscal Dynamics: The Growing SqueezeComprehensive Fiscal Overview (2020-2026)Fiscal IndicatorValuePeriodTarget/BenchmarkStatusTax Revenue as % of GDP13.3%2025/26 (Projection)14.1% (Target)⚠️ Below targetHistorical Tax-to-GDP (Baseline)8%Early 1990sPre-reform eraImproved significantlyHistorical Tax-to-GDP11%2020N/ASteady increaseSub-Saharan Africa Average16.1%2023Regional benchmark🔴 -2.8pp gapActual Tax CollectionsTZS 22.38 trillionBy Feb 202599.9% of target✅ On track (+16.6% YoY)Budget SizeTZS 57 trillion2025/26Growing infrastructure needsExpandingBudget Deficit % of GDP3.0%2025/26 (Projection)Below 3.5%⚠️ Risk of wideningPrevious Deficit3.4%2024/25N/AImproving trendDeficit Risk Scenario3.5%PotentialSpending pressure threshold🔴 Critical trigger pointCurrent Account Deficit2.4% of GDPYear ending Sept 2025Narrowed from previous✅ ImprovingThe Fiscal Paradox

70% of tax revenue is collected in Dar es Salaam, yet 70% of GDP is generated outside the city. This geographic mismatch reveals the formalization challenge: economic activity is widespread, but tax compliance is concentrated where enforcement is strongest.

This creates a vicious cycle: limited revenues → constrained infrastructure investment → informal sector remains competitive → tax base stays narrow.

Dar es Salaam Supply Chain Vulnerabilities: A 24-48 Hour Crisis WindowCritical Vulnerability Alert

Dar es Salaam’s food distribution system can experience nationwide price spikes within 24-48 hours of any major disruption. This extreme sensitivity stems from high import dependency, centralized distribution, poor infrastructure, and informal market structures lacking buffer stocks.

Supply Chain Vulnerability FactorsVulnerability FactorCurrent Data/ImpactTimelineRisk LevelFood Import Dependency>50% sunflower oil importedOngoing🔴 CriticalTotal Food/Beverage ImportsUSD 43.5 million2022🟡 HighDistribution CentralizationConcentrated in DarStructural🔴 CriticalInfrastructure GapsPoor roads, electricityOngoing🔴 CriticalPrice Inflation SpeedNationwide ripple in 24-48hrsPer disruption🔴 CriticalRecent Price Increases (Rice)3,000-3,500 TZS/kg2024-2025🟡 HighRecent Price Increases (Beans)4,000 TZS/kg2024-2025🟡 HighFood Inflation Rate5.6%May 2025🟡 HighOverall Import Vulnerability41% fuel/machinery importsStructural🟡 HighGlobal Shock ExposureUS-China trade tensionsExternal risk🟡 HighRegional DisruptionsGrain import bans in regionCurrent🟡 HighCOVID-19 Impact ExampleLockdowns hit informal services2020-2021Historical lessonInformal Sector AmplificationNo buffer stocks/insuranceStructural🔴 CriticalWhy Immediate Action Is Required

Unlike the broader economic transformation which can follow a 15-20 year timeline, food security vulnerabilities require urgent intervention (2025-2027) because:

Single-day disruptions can trigger citywide shortagesInformal distribution networks have zero buffer capacityInfrastructure gaps (roads, storage) amplify every shock5.6% food inflation already straining household budgetsPolitical instability could emerge from food price spikes

Solution: Cannot wait for full economic transformation; requires parallel urgent intervention in agricultural value chains, infrastructure, and strategic buffer stock systems.

Transformation Timeline & Scenarios (2025-2045)Three Transformation Scenarios

1

PHASE 1: Foundation Building (2025-2030)

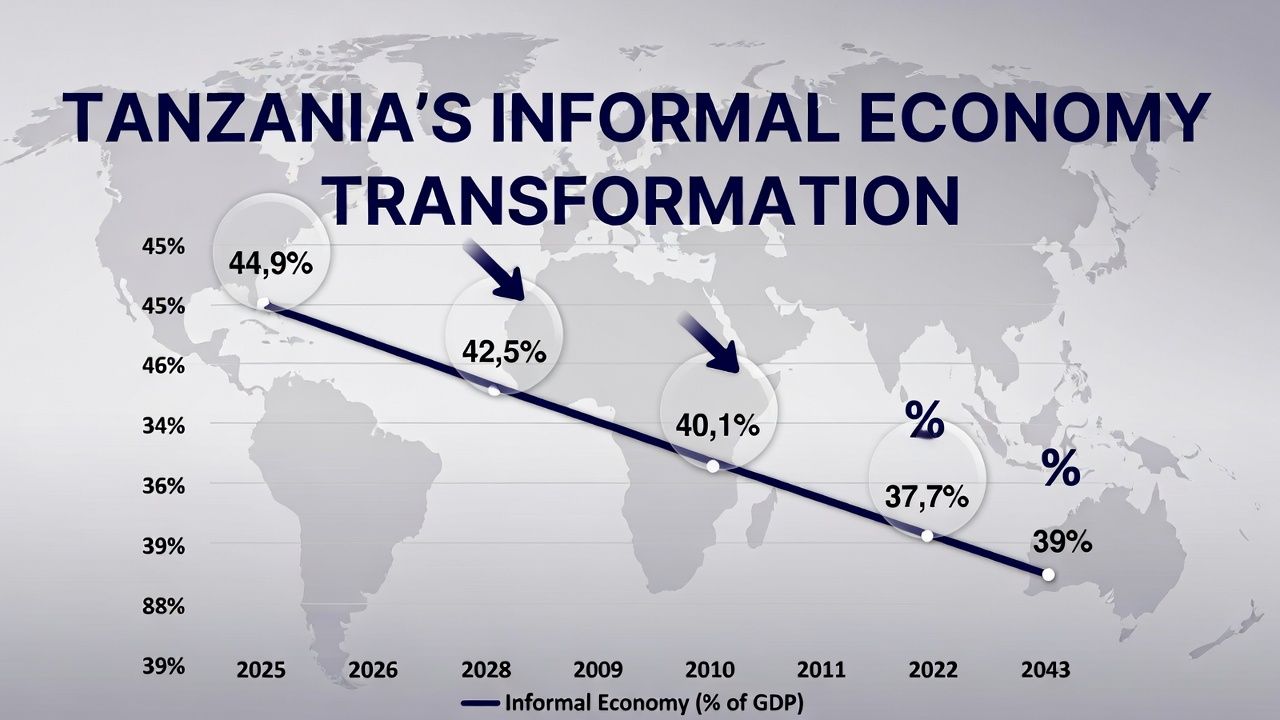

Informal Sector Projection: 44.9% → 42-43% of GDP

GDP Growth: 6.0% sustained annually

Critical Actions Required:

Digital infrastructure deploymentSimplified business registration and taxationMassive skills training programs for 900,000 annual entrantsSocial protection system expansion

Key Risk: 900,000 youth entering annually without adequate formal job opportunities creates social pressure

2

PHASE 2: Acceleration (2030-2040)

Informal Sector Projection: 42% → 39% of GDP

Primary Drivers:

Rising debt service obligationsBudget deficits potentially exceeding 3.5%Infrastructure completion enabling formal competitionDigital economy integration making tax evasion harder

Critical Period Risk: Without preparation in Phase 1, this becomes the “forced transformation” window causing massive job losses and social instability

3

PHASE 3: Maturation (2040-2050)

Optimistic Scenario: 39% → 30-35% of GDP (with aggressive reforms)

Current Path Scenario: 39% → 35-39% of GDP (status quo)

Outcome Determination:

Semi-formalized economy emergesUnlikely to reach global 11.8% without dramatic accelerationQuality of transformation depends entirely on 2025-2030 actionsDetailed Timeline ProjectionsPeriodInformal % of GDPInformal Employment %Key DriversMajor Risks2025 (Current)44.9%84%Status quo persistenceGrowing fiscal pressures203042-43%~82%Minimal shift without reforms900K/year labor surplus accumulates203540-41%~78%Economic pressures mountDebt crisis potential emerges204038-40%~74%Forced formalization likelyMass unemployment if unprepared204339% (baseline projection)69%Slow structural changePersistent dual economy2050 (Optimistic)30-35%~60%Successful managed transitionRegional competitiveness restored2050 (Status Quo)35-39%~65%Minimal policy interventionLocked in low productivity trapForced Transformation Triggers (2035-2040 Window)Trigger EventProjected TimelineMechanismImpact Without PreparationWidening Budget Deficits10-15 yearsDeficit consistently >3.5%, forcing fiscal reformsSudden tax enforcement, business closuresDebt Crisis10-15 yearsExternal debt becomes unsustainableIMF conditionalities force rapid formalizationGlobal Economic ShocksOngoing riskTrade wars, commodity price volatilityInformal sector cannot compete with formal importsYouth Unemployment Explosion5-10 years900,000 annual entrants create massive surplusSocial unrest, political instabilityInfrastructure Completion10-20 yearsRoads, electricity enable formal operationsInformal operators lose competitive advantagesDigital Economy Integration5-10 yearsMobile money, digital taxation systemsTax evasion becomes impossibleThe 2035-2040 Trigger Point

Without preparation begun NOW (2025-2030), forced transformation will cause:

Mass unemployment affecting 84% of current workforce (millions of jobs)Social unrest and political instabilityEconomic contraction of 2-5% before eventual recoveryWidening inequality as formal-sector workers gain while informal workers sufferLost decade of development progressThe Choice Ahead: Managed Transition or Crisis-Driven Shock

Tanzania stands at a critical crossroads. The informal sector that once provided economic stability now threatens to become a source of structural fragility. With 44.9% of GDP and 84% of employment still outside the formal economy, and 900,000 young people entering the labor market each year, the window for managed transformation is narrow.

The data is unequivocal: actions taken between 2025-2030 will determine whether Tanzania achieves a successful 15-20 year transformation or faces a crisis-driven shock by 2035-2040 that could trigger mass unemployment, social instability, and economic contraction.

The path forward requires immediate, coordinated action across multiple fronts: simplified taxation, massive skills development, infrastructure investment, social protection expansion, and strategic food security interventions. The cost of delay will be measured not just in economic terms, but in the lives and livelihoods of millions of Tanzanians.

The question is no longer whether formalization will happen—but whether Tanzania will prepare for it.