Key Points

Celestica is expecting stronger growth in 2026, fueled by the healthy demand for its connectivity and cloud solutions.

The company develops AI data center infrastructure for hyperscalers and chip designers, suggesting that its rapid growth is sustainable.

Celestica’s improving profitability and earnings growth potential indicate that this AI stock can keep soaring.

Electronics manufacturing services provider Celestica(NYSE: CLS) has been one of the hottest stocks on the market over the past year, soaring an incredible 345% as of this writing.

The company offers design, engineering, and manufacturing services to various sectors through two business segments — connectivity and cloud solutions (CCS) and advanced technology solutions (ATS). And Celestica’s CCS business is benefiting big-time from the tech sector’s heavy investments in artificial intelligence (AI) data center infrastructure.

Will AI create the world’s first trillionaire? Our team just released a report on the one little-known company, called an “Indispensable Monopoly” providing the critical technology Nvidia and Intel both need. Continue »

In fact, the CCS business should ensure that Celestica’s red-hot stock market run continues.

Image source: Getty Images.

Celestica is supporting the aggressive AI data center build-out

Celestica’s CCS business accounted for 80% of its revenue in the first quarter. The segment’s revenue shot up 76% year over year, driving an overall 53% increase in its top line to $4.05 billion. The company clocked stronger-than-expected growth last quarter as it ramped up the production of Ethernet switches for hyperscalers deploying AI data centers.

The company manufactures Ethernet switches for multiple hyperscaler customers. The good news is that these customers continue to tap Celestica to design and develop more AI networking infrastructure. For instance, management noted on the latest earnings call that it secured two new programs in Q1.

One of these new customer wins is for designing and manufacturing Advanced Micro Devices’ (NASDAQ: AMD) Helios rack-scale AI architecture. AMD announced its rack-scale server platform in October last year. This platform integrates its Instinct data center graphics processing units (GPUs), Epyc server processors, and networking hardware.

AMD has chosen Celestica to bring this rack-scale platform to the market. The electronics manufacturing company will “undertake the R&D, design and manufacturing of scale-up networking switches.” Celestica is scheduled to begin supplying the initial units to AMD by the end of the year.

It is worth noting that AMD will start deploying Helios for Meta Platforms’ data centers this year. Those two companies are in a multiyear partnership to deploy 6 gigawatts (GW) of AI data centers. So, Celestica could witness a significant ramp-up in revenue and profitability as it starts the volume production of AMD’s hardware. Importantly, Celestica points out that the pipeline for its networking products remains robust through 2028.

Even better, the company is witnessing healthy margin improvement driven by a better product mix, which explains why its adjusted earnings per share (EPS) increased by 80% year over year to $2.16 per share. Celestica’s guidance suggests its growth rate could improve further. The company raised its full-year revenue guidance from $17 billion to $19 billion, which would be a jump of 53%.

It also increased its adjusted EPS guidance to $10.15 from the earlier estimate of $8.75, driven by expectations of further margin improvements. The updated guidance points to a year-over-year jump of 68% in Celestica’s bottom line.

However, don’t be surprised to see further upward revisions to guidance. Management remarked on the Q1 earnings call that it will update the outlook as the year progresses and also added that it expects significantly higher revenue growth in 2027.

It is easy to see why Celestica remains confident of faster growth in the future. McKinsey estimates that global data center spending could jump to a whopping $7 trillion by 2030. As a result, demand for Celestica’s electronics manufacturing services should continue to improve, potentially driving further upside in the stock price.

Celestica’s earnings growth potential suggests that the stock can move higher

Celestica is trading at 51 times earnings right now, a premium to the Nasdaq-100 index’s earnings multiple of 34. However, the company’s outstanding earnings growth makes it clear why.

Moreover, Celestica is confident it can deliver stronger growth as data center infrastructure spending rises.

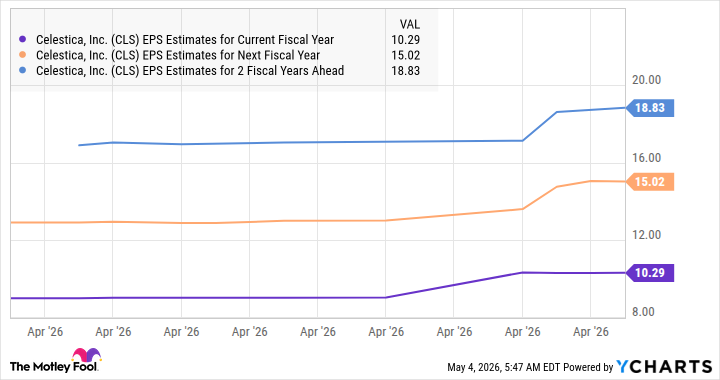

CLS EPS Estimates for Current Fiscal Year data by YCharts.

Analysts’ estimates could rise as the company ramps up its design and manufacturing services for its hyperscaler customers. But if Celestica’s earnings reach just $18.83 per share in 2028 and it only trades at the Nasdaq-100’s average earnings multiple, the stock would be trading at $640. That’s 52% higher than its current price, which means it isn’t too late for investors to buy this high-flying AI stock.

Should you buy stock in Celestica right now?

Before you buy stock in Celestica, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Celestica wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004… if you invested $1,000 at the time of our recommendation, you’d have $473,985!* Or when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $1,204,650!*

Now, it’s worth noting Stock Advisor’s total average return is 950% — a market-crushing outperformance compared to 203% for the S&P 500. Don’t miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

*Stock Advisor returns as of May 6, 2026.

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Advanced Micro Devices, Celestica, and Meta Platforms. The Motley Fool has a disclosure policy.