If you have ever wondered whether Novartis shares are worth their current price, you are not alone. Many investors are trying to pinpoint whether there is real value up for grabs.

Shares have moved up a solid 5.8% in the last month and are up an impressive 17.5% year-to-date, hinting at shifting sentiment and growth potential.

Rumors of strategic partnerships and ongoing success in the company’s drug pipeline have sparked renewed interest, while regulatory updates have also helped fuel the recent price rally. Investors are keeping a close eye on industry news to get ahead of potential catalysts.

Novartis bags a valuation score of 5 out of 6, which is a strong showing under our checklist approach. Let us dig into the methodology and, more importantly, consider what smarter ways to value a stock might reveal later on.

Find out why Novartis’s 16.1% return over the last year is lagging behind its peers.

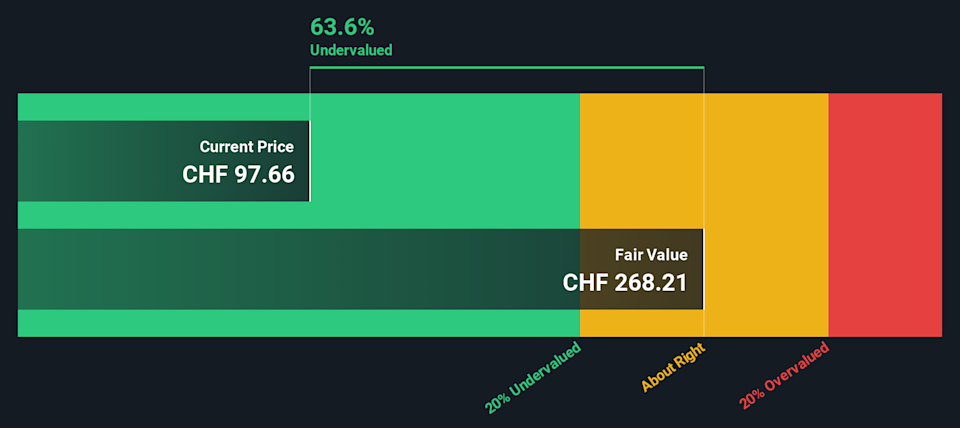

The Discounted Cash Flow (DCF) model estimates what a company is worth today by forecasting how much cash it will generate in the future and then discounting those future cash flows back to their present value. This approach helps investors understand whether a stock may be undervalued or overpriced relative to those projections.

For Novartis, analysts report a current last twelve months Free Cash Flow (FCF) of $18.16 billion. Over the next five years, the company’s FCF is projected to rise year over year, reaching $20.97 billion by 2029. Analyst figures are available for the first several years, with the later forecasts extrapolated from those trends. Extending out to 2035, Simply Wall St projects FCF to approach $24.38 billion.

Based on the DCF model, the estimated intrinsic fair value per share is $280.68. This suggests the stock is trading at a 62.7% discount compared to its fair value, indicating considerable upside if projections hold true. The model uses cash flow projections and conservative growth rates to arrive at this figure, giving investors a clearer view of long-term potential.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Novartis is undervalued by 62.7%. Track this in your watchlist or portfolio, or discover 934 more undervalued stocks based on cash flows.

NOVN Discounted Cash Flow as at Nov 2025

NOVN Discounted Cash Flow as at Nov 2025

For profitable companies like Novartis, the price-to-earnings (PE) ratio is a trusted and widely used valuation metric. The PE ratio measures how much investors are willing to pay for each franc (CHF) of earnings, providing quick insight into market expectations about a company’s growth and risk profile.

Story Continues

A “normal” or “fair” PE ratio for a company depends significantly on future growth potential and the perceived risk in its earnings. Companies with stronger growth or more stable profits typically trade at higher PE multiples, while those facing uncertainty may deserve lower ones. As context, Novartis currently trades at a PE of 17.33x, compared to the pharmaceuticals industry average of 22.93x and a broader peer group average of 81.84x. This suggests Novartis is priced more conservatively by the market than many of its peers.

To go deeper, Simply Wall St calculates a proprietary “Fair Ratio” for each stock, which more accurately gauges value by blending not just earnings, but growth expectations, industry trends, profit margins, overall market capitalization, and company-specific risks. For Novartis, this Fair Ratio is 30.29x. The Fair Ratio is considered far more insightful than basic peer or industry comparisons, because it customizes expectations to the unique profile of Novartis rather than generalizing across companies that may not be directly comparable.

Since Novartis trades at 17.33x compared to a Fair Ratio of 30.29x, the shares appear undervalued on this measure. This means the current price may not fully reflect the company’s quality or future potential.

Result: UNDERVALUED

SWX:NOVN PE Ratio as at Nov 2025

SWX:NOVN PE Ratio as at Nov 2025

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1441 companies where insiders are betting big on explosive growth.

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives. A Narrative, in simple terms, is your personal story about a company. It is how you connect your understanding of Novartis’ business, the numbers you think are likely for its future revenue, profits, and margins, and your idea of fair value, all into one dynamic forecast.

Narratives on Simply Wall St let you document your reasoning and expectations, then see these play out as a fair value calculation, making your investment outlook more transparent, deliberate, and tailored to your own view. As millions of investors use Narratives within the platform’s Community page, you can easily compare your perspective to others, refine your ideas, and make more confident decisions about when to buy or sell by comparing each narrative’s Fair Value to the latest share price.

Best of all, Narratives are kept up-to-date whenever new news or earnings arrive, so your financial story stays relevant. For example, one investor might see Novartis’ growth in emerging markets and new drug launches as reasons to set a fair value at CHF120, while another could be more cautious about generic competition and global pricing pressure, keeping their estimate close to CHF80. By using Narratives, you put your own logic front and center and adjust it as the story changes.

Do you think there’s more to the story for Novartis? Head over to our Community to see what others are saying!

SWX:NOVN Community Fair Values as at Nov 2025

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include NOVN.SW.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com