In this report:

-

October 10 Market Dislocation Highlights Risk Dynamics in Crypto Lending

-

Plasma’s Rapid Launch Reinforces DeFi Lending Stability

-

Paypal and Spark Partner to Expand PYUSD Liquidity Through DeFi

-

Morpho Expands the Institutional Backbone of On-Chain Lending

Market Update

Crypto markets rallied steadily through September, supported by softer U.S. macro data, renewed ETF inflows, and growing expectations for the Federal Reserve’s rate cut. The Fed delivered the anticipated 25 bps reduction on September 18, lowering the policy range to 4.00–4.25% and hinting that more cuts may follow later in the year. The move improved liquidity conditions, easing cash borrowing costs across both fiat and stablecoin markets, and set a constructive tone for digital assets.

In September, Bitcoin (BTC) climbed from roughly $109,000 to $117,000, while Ethereum (ETH) advanced from $4,300 to $4,600 before retracing to around $4,000 by month-end. Solana (SOL) outperformed, gaining over 10% to reach the mid-$240s amid strong ecosystem inflows, though it later eased back to the $200 range. Volatility compressed into the FOMC meeting as traders positioned for potential easing, underpinned by stable liquidity across derivatives and spot markets.

In derivatives, the CME front-month basis captured steady institutional demand for leverage. The BTC basis traded between 6–9% annualized, peaking near 9% in late September before retracing, while ETH’s basis followed a similar range of 6–10%. SOL’s basis remained elevated between 12–20%, consistent with its higher beta and active on-chain lending dynamics. Rising basis levels signaled renewed appetite for leveraged exposure, with front-month futures trading above spot as capital rotated into basis-arbitrage trades. This rotation temporarily lifted short-term funding rates, as liquidity providers redirected capital from external lending toward futures hedging and carry capture.

Despite the firm basis, overall leverage remained contained. BTC perpetual funding averaged 6–10% APR, with ETH around 8%, levels that indicate a balanced and disciplined derivatives market rather than speculative excess. Combined with cheaper cash borrowing costs following the Fed cut, the funding backdrop supported stable crypto credit conditions through month-end.

By late September, both basis and funding normalized alongside lower volatility, leaving the market in a healthy position heading into October. That stability proved short-lived, however, as early-October macro shocks and a record liquidation cascade quickly reset market conditions.

Key Trends:

001

October 10 Market Dislocation Highlights Risk Dynamics in Crypto Lending

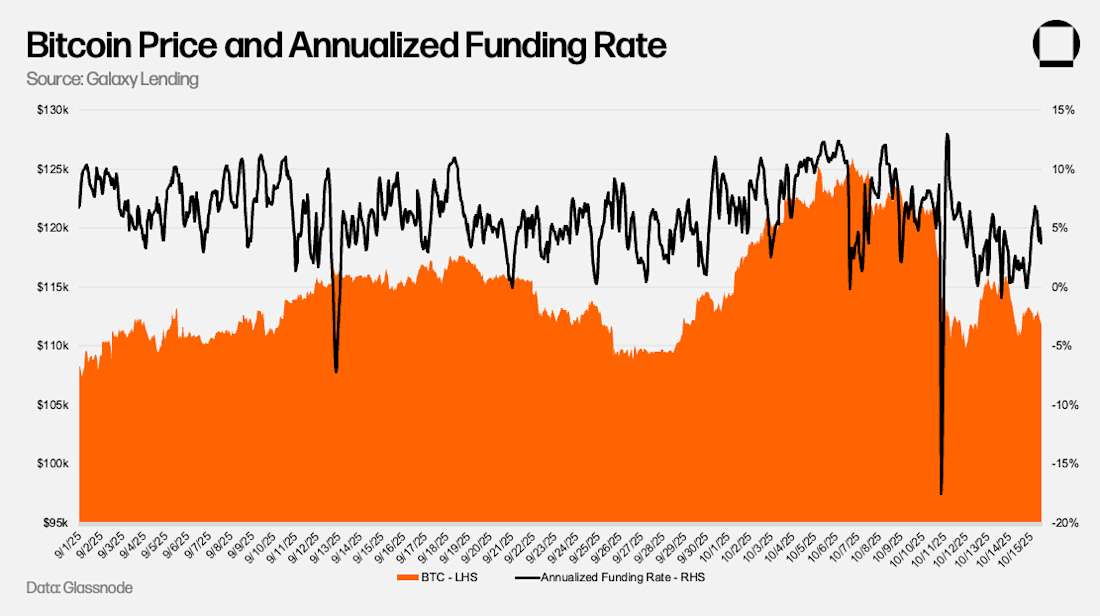

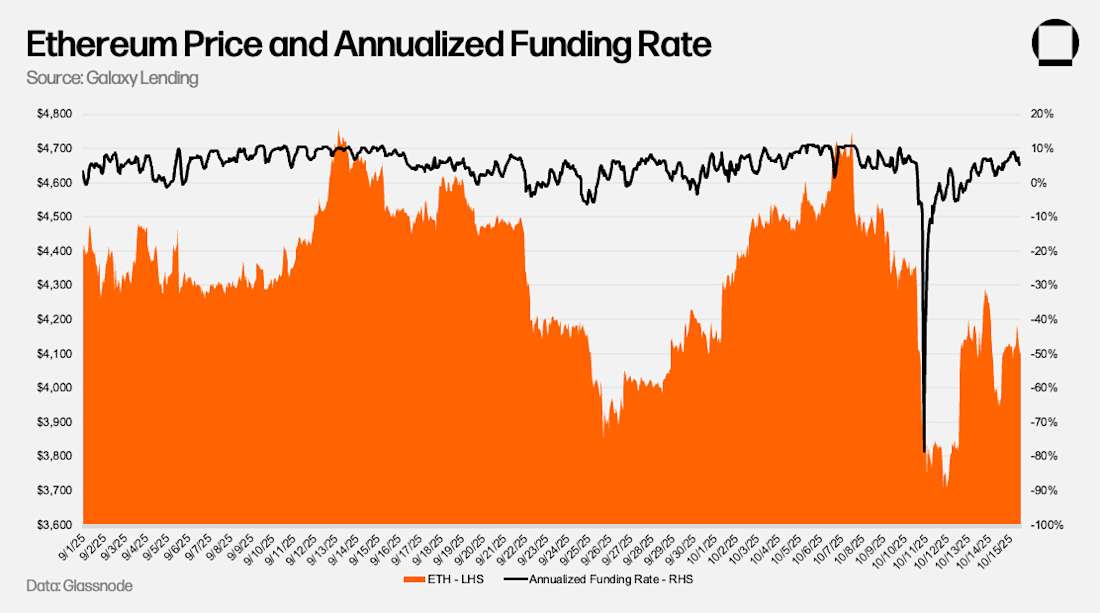

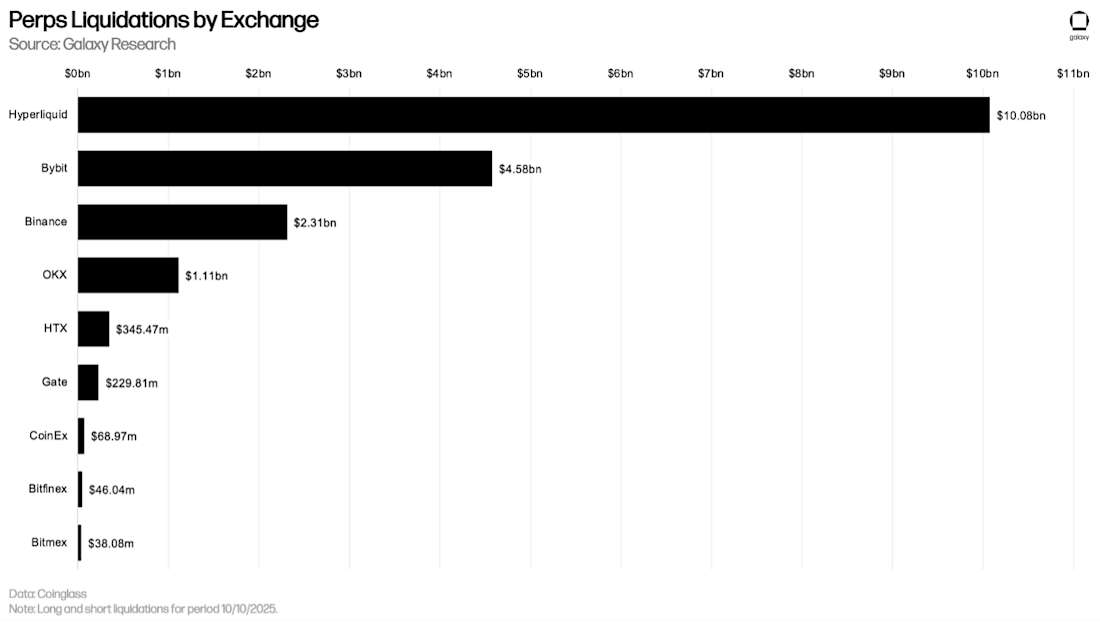

On Friday night, October 10 (EST), the crypto market endured its largest liquidation event in history, with estimated forced unwinds ranging between $20 billion and $40 billion in notional positions — surpassing even the May 2021 crash, when roughly $10 billion was liquidated. The trigger came after President Trump’s announcement of potential 100% tariffs on Chinese imports, which sent risk assets tumbling globally. As traditional markets closed, liquidity in crypto thinned sharply, and aggressive selling cascaded across exchanges.

Bitcoin briefly fell to around $101,000 before recovering toward $113,000 as the weekend progressed. Across major venues, exchange market makers faced collateral constraints, where unmet margin calls and thin order books accelerated the liquidation cycle. The result was significant price dislocation, with some altcoins dropping 30–70%, while yield-generating assets such as USDe, bnSOL, and wBETH temporarily depegged as collateral was liquidated into shallow markets. All three assets were quickly arbitraged back to near parity once liquidity normalized. In the aftermath, Binance announced roughly $283 million in compensation to affected users, underscoring both the scale of the event and the exchange’s role in restoring market confidence.

Centralized lenders were relatively well positioned, managing through the accelerated market crash with limited disruption. The market recovered quickly, validating the strength of risk frameworks and collateral management practices across CeFi desks.

DeFi and exchange-based leverage experienced their own set of challenges. Many participants rely on these venues for their efficiency and automation, but their auto-liquidation and auto-deleverage mechanisms can amplify the speed of market moves during sharp drawdowns. These systems serve a vital role in protecting protocol solvency, yet they inherently react to price volatility in real time.

In summary, the event demonstrated how different risk frameworks across the industry operate under stress. Automated protocols provide transparency and mechanical risk control, while CeFi lenders complement the ecosystem by managing credit exposures and collateral positions with human oversight and flexibility. Both play important roles in supporting a more resilient and liquid crypto lending market.

002

Plasma’s Rapid Launch Reinforces DeFi Lending Stability

Plasma’s launch in September was one of the most significant liquidity events of the year in the crypto space, drawing approximately $6 billion in deposits within ten days and reaching a peak of more than $8 billion on Aave. The surge in inflows reflected sustained demand for stablecoin-driven markets and demonstrated how quickly capital can mobilize toward new protocols that integrate seamlessly with established lending infrastructure.

During the launch period, Galaxy actively participated in Aave’s liquidation processes on Plasma, providing liquidity during deleveraging events and supporting orderly collateral management across the platform.

003

Paypal and Spark Partner to Expand PYUSD Liquidity Through DeFi

In September, PayPal announced a partnership with Spark aimed at deploying up to $1 billion of PYUSD liquidity into DeFi lending protocols, following an initial wave of deposits that reached roughly $100–$135 million within days of launch. The initiative came during a period of record stablecoin activity, with global supply expanding by about $30 billion to $263 billion and daily volumes exceeding $100 billion.

Spark, known for its large-scale on-chain credit facilities, previously supported Coinbase’s institutional lending operations through its Spark Liquidity layer. Spark’s ecosystem links lending markets, liquidity layers, and decentralized exchanges into a single infrastructure — allowing stablecoins to achieve scale and utility across DeFi markets at institutional depth.

For PayPal, this move extends PYUSD’s reach beyond payments and into capital markets functionality — using DeFi infrastructure to deepen liquidity, establish yield channels, and enhance the stablecoin’s utility. Spark’s prior institutional lending work gave the partnership immediate credibility, showing that regulated fintechs can deploy significant liquidity on-chain without abandoning compliance standards.

004

Morpho Expands the Institutional Backbone of On-Chain Lending

In September, Morpho gained further traction with key partnerships that broadened its institutional presence. Crypto.com announced plans to integrate Morpho for its on-chain lending and stablecoin yield products, while Société Générale’s SG-Forge adopted Morpho and Uniswap to enable lending and borrowing using its MiCA-compliant stablecoins, EURCV and USDCV.

These developments reflect the continued adoption of DeFi lending infrastructure by institutional players. By enabling regulated entities to lend and borrow on-chain with transparent collateral management and defined rate structures, Morpho is contributing to the gradual normalization of institutional activity within DeFi credit markets. For the broader lending landscape, this steady participation reinforces that institutional capital remains an important and growing component of on-chain liquidity and credit formation.

Notable News:

Subscribe to receive this commentary and more directly to your inbox!

This document, and the information contained herein, has been provided to you by Galaxy Digital Holdings LP and its affiliates (“Galaxy”) solely for informational purposes. Galaxy provides comprehensive financial products and services to institutions, corporates, and qualified individuals (typically Eligible Contract Participants and accredited investors) within the digital asset ecosystem. This document may not be reproduced or redistributed in whole or in part, in any format, without the express written approval of Galaxy. Neither the information, nor any opinion contained in this document, constitutes an offer to buy or sell, or a solicitation of an offer to buy or sell, any advisory services, securities, futures, options or other financial instruments or to participate in any advisory services or trading strategy. Nothing contained in this document constitutes investment, legal or tax advice. You should make your own investigations and evaluations of the information herein. Any decisions based on information contained in this document are the sole responsibility of the reader. Certain statements in this document reflect Galaxy’s views, estimates, opinions or predictions (which may be based on proprietary models and assumptions, including, in particular, Galaxy’s views on the current and future market for certain digital assets), and there is no guarantee that these views, estimates, opinions or predictions are currently accurate or that they will be ultimately realized. To the extent these assumptions or models are not correct or circumstances change, the actual performance may vary substantially from, and be less than, the estimates included herein. None of Galaxy nor any of its affiliates, shareholders, partners, members, directors, officers, management, employees or representatives makes any representation or warranty, express or implied, as to the accuracy or completeness of any of the information or any other information (whether communicated in written or oral form) transmitted or made available to you. Each of the aforementioned parties expressly disclaims any and all liability relating to or resulting from the use of this information. Certain information contained herein (including financial information) has been obtained from published and non-published sources. Such information has not been independently verified by Galaxy and Galaxy does not assume responsibility for the accuracy of such information. Affiliates of Galaxy’s own investments in some of the digital assets and protocols discussed in this document. Except where otherwise indicated, the information in this document is based on matters as they exist as of the date of preparation and not as of any future date, and will not be updated or otherwise revised to reflect information that subsequently becomes available, or circumstances existing or changes occurring after the date hereof. The foregoing does not constitute a “research report” as defined by FINRA Rule 2241 or a “debt research report” as defined by FINRA Rule 2242 and was not prepared by GalaxyDigital Partners LLC. Similarly, the forgoing does not constitute a “research report”, as defined under CFTC Regulation 23.605(a)(9), and may only be considered a solicitation for entering into a derivatives transaction for purposes of CFTC Regulation 23.605. It is not intended to constitute a solicitation for any other purposes under CFTC or NFA rules, and it should not be relied on as a form of recommendation to trade under CFTC regulations. Any statement, express or implied, contained within these materials is subject, in all cases, to the actual terms of an agreement entered into with Galaxy Digital on a principal basis. The Information is being provided solely for informational purposes about Galaxy Digital and may not be used or relied on for any purpose (including, without limitation, as legal, tax or investment advice) without the express written approval of Galaxy Digital. The Information is not an offer to buy or sell, nor is it a solicitation of an offer to buy or sell, any investment banking services, securities, futures, options, commodities or other financial instruments or to participate in any investment banking services or trading strategy. Any decision to make an investment or enter into a transaction should be made after conducting such investigations as the investor deems necessary and consulting the investor’s own investment, legal, accounting and tax advisors in order to make an independent determination of the suitability and consequences of an investment. Additional information about the Company and its products and services can be found at Galaxy Digital’s website at galaxy.com. For all inquiries, please email [email protected]. ©Copyright Galaxy Digital Holdings LP 2025. All rights reserved.